Today we are covering the slightly easy and less conceptual topic of trial balance. It is just a posting of balances from the ledger in to it. We will learn the meaning of trial balance, Advantages, methods and to understand it in much better ways we will solve one example with all methods of it. After reading this article you can prepare and check out the trial balance of any business.

What is Trial Balance:

It shows the total closing balanced amounts of all the ledger accounts for the specific period i.e. for a month, for a quarter, for six months, and for a whole year. it is the end of the accounting process. In the double-entry accounting system, there is always the same amount of Credit corresponding to every Debit. so, the Total trial balance always is equal if not then there is an error in the posting of the transactions.

In a manual system of accounting:-

An accountant needs to prepare the trial balance. He matched the Debit balance amounts with Credit balance amounts. If they agree it means that it has no error of omission, commission and etc. we will discuss the meaning of all these errors in a separate upcoming article.

Note: –

- Debit balance amounts mean that amounts which are listed in a column with the heading “Debit balances”.

- Credit balance amounts mean that amounts which are listed in a column with the heading “Credit balances”.

- We will explain the topic of errors in next upcoming articles.

Nowadays, in the computerized system of accounting:-

An accountant doesn’t need to prepare a trial balance Because it will be prepared automatically by the accounting software (Like Tally, SAP, ZOHO, Marg, etc.). An accountant just has to post all business transactions in the subsidiary books of accounting i.e. Cash Book, Purchase Book, Sales Book, Purchase Return Book, Sales Return Book and last is Journal Proper.

Advantages of a Trial Balance

In the manual system:

- With the help of it, we will ensure that all the amount of Debit has the corresponding amount of Credit.

- It helps to identify the error of omission, commission and etc.

- It proves the arithmetical accuracy of the accounting work done by the bookkeeper.

The following advantages are common in both the system: –

In the computerized system

- It is also very useful for auditors, they will get the general ledger account balances prior to their proposed adjustments, and after their proposed adjustments.

- The trial balance helps the accountant to prepare and finalize the financial statement for the year because it is the list of all debit and credit balances of leader accounts.

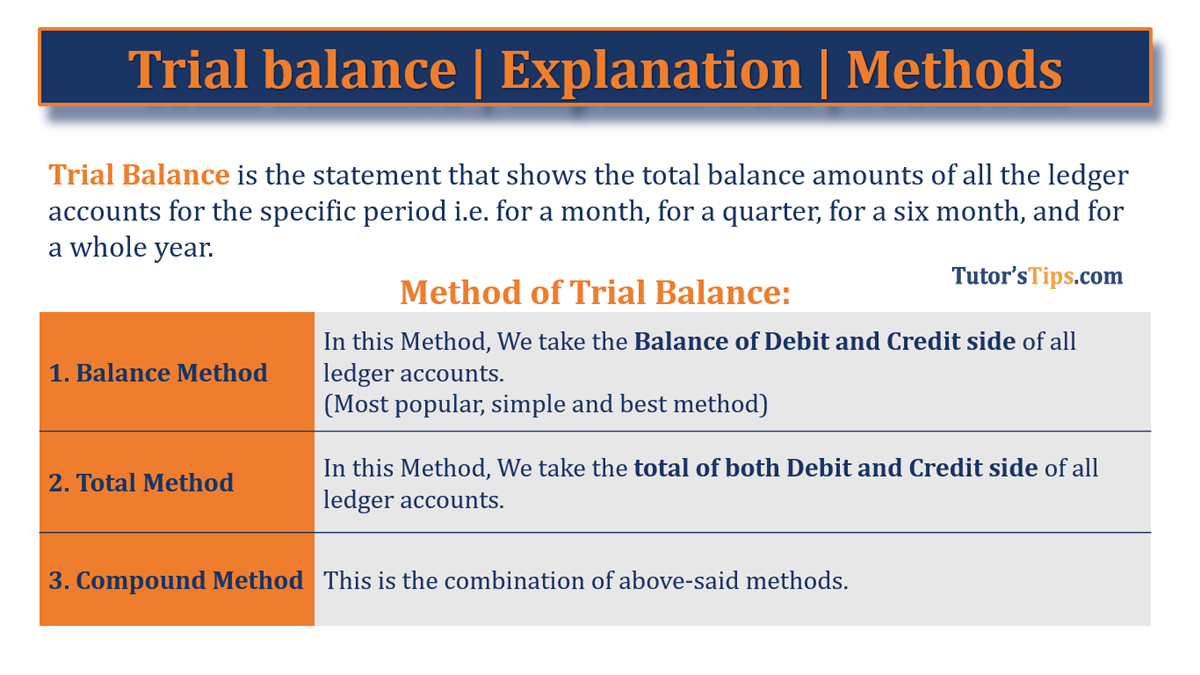

Method of Trial Balance:

The following are the three methods of Trial Balance: –

| 1. Balance Method | In this Method, We take the Balance of the Debit and Credit sides of all ledger accounts.(Most popular, simple and best method) |

| 2. Total Method | In this Method, We take the total of both the Debit and Credit sides of all ledger accounts. |

| 3. Compound Method | This is a combination of the above-said methods. |

The examples of all methods of the Trial Balance: –

We are taking a single example and then we will prepare a trial balance with all the above-said three methods: –

Advertisement-X

Example 1: –

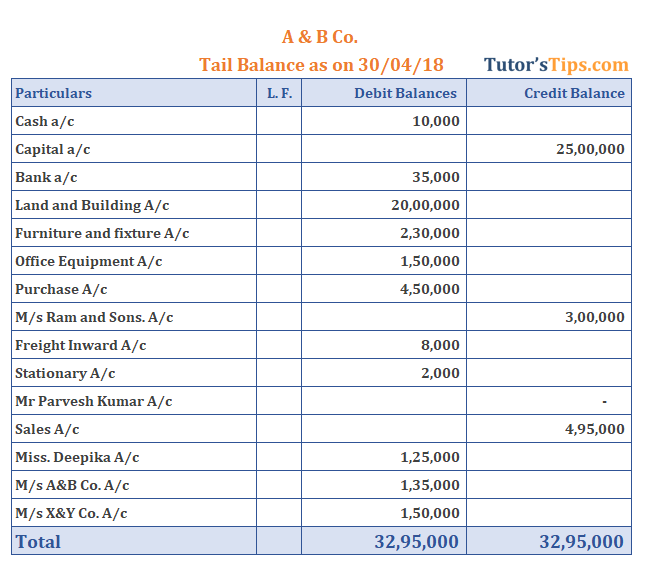

Prepare a trial balance of A&B co. as on 30/04/18 with all three methods.

| Date | Transaction | Amount |

| Cash | 20,000 | |

| Bank | 100,000 | |

| Land and Building | 2,000,000 | |

| Furniture and fixture | 230,000 | |

| Office Equipment | 150,000 | |

| 05/04/2018 | Purchase goods from M/s Ram and Sons. | 250,000 |

| 05/04/2018 | Paid Freight by cash | 5,000 |

| 07/04/2018 | Paid for Stationery Items | 2,000 |

| 09/04/2018 | Sold goods to Mr. Parvesh Kumar | 85,000 |

| 12/04/2018 | Paid to M/s Ram and Sons by cheque | 150,000 |

| 15/04/2018 | Purchase goods from M/s Ram and Sons. | 200,000 |

| 15/04/2018 | Paid Freight by cash | 3,000 |

| 18/04/2018 | Sold goods to Miss. Deepika and payment received by cheque | 125,000 |

| 21/04/2018 | Payment received from Mr. Parvesh Kumar by cheque | 85,000 |

| 25/04/2018 | Sold goods to M/s A&B Co. | 135,000 |

| 28/04/2018 | Sold Goods to M/s X&Y Co. | 150,000 |

“Download Example in PDF format”

Solutions: –

First of all, we have to post all these above transactions in the journal.

- I have posted all the transactions in the journal but attached the file in PDF format because of the increase in the length of an article.

“Download all Journal entries in PDF Format”

and after that, we have to post all journal entries in the ledger accounts. It’s also attached.

“Download all Ledger accounts in PDF format”

after taking the above steps we got a statement of ledger accounts including the total of the debit side, the total of the credit side and balances shown as the following: –

Now we will prepare Trial Balances with all three methods: –

1. Balance Method: –

In the balance method, we have to post all the Debit balances shown in the column of “Balances” in the above statement of ledger accounts in the trial balance column named “Debit Balances” and the credit balance in the column named “Credit balances”.

“Important Note: – Trial balance always has equal total in both the column named debit Balance and credit balances.”

Advertisement-X

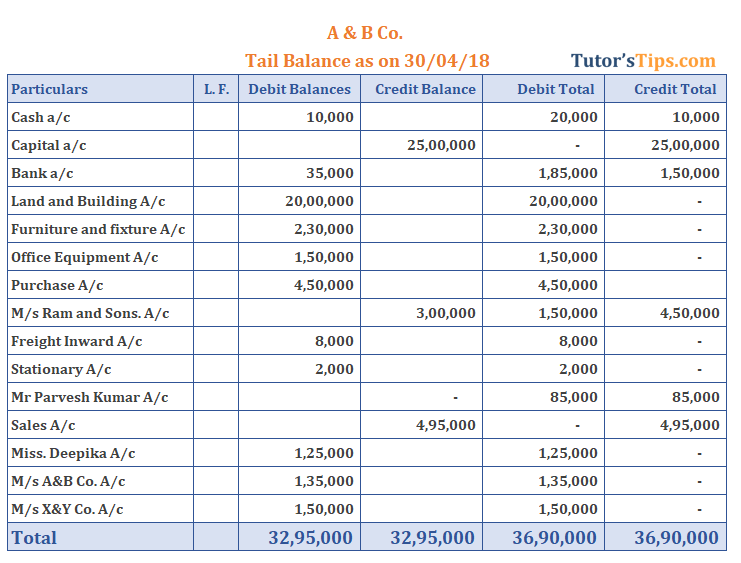

2. Total Method: –

In the Total method, we have to post all the total amount of Debit side of all ledger accounts shown in the column of “Debit Total” in the above statement of ledger accounts in the trial balance column named “Debit Total” and the credit total in the column named “Credit Total”.

Trial Balance – Solved with Total Method

3. Compound Method: –

The Compound method is the mixture of both the above-explained method or we can say that show both methods on a single sheet. As shown below: –

Trial Balance – Solved with Compound Method

Thanks for reading the topic of Trial Balance, please comment your feedback on whatever you want. If you have any questions please ask us by commenting.

Please Share and spread it.