Question No 9 Chapter No 10

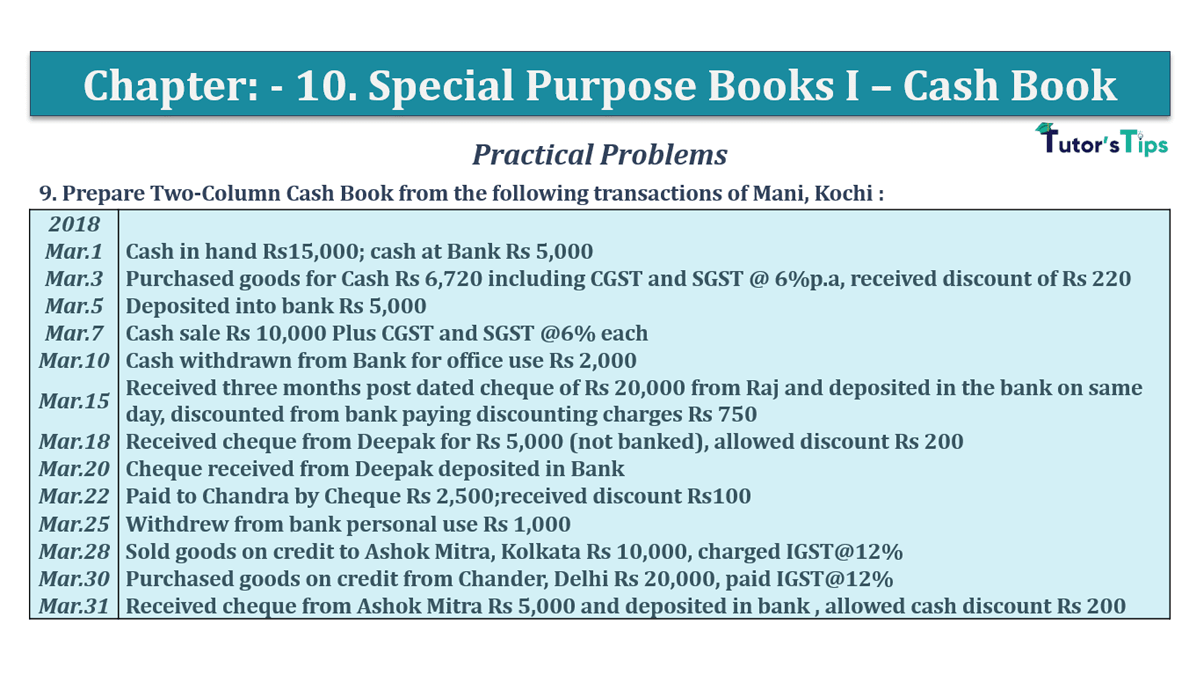

Prepare Two-Column Cash Book from the following transactions of Mani, Kochi :

| 2018 | |

| Mar.1 | Cash in hand Rs15,000; cash at Bank Rs 5,000 |

| Mar.3 | Purchased goods for Cash Rs 6,720 including CGST and SGST @ 6%p.a, received a discount of Rs 220 |

| Mar.5 | Deposited into bank Rs 5,000 |

| Mar.7 | Cash sale Rs 10,000 Plus CGST and SGST @6% each |

| Mar.10 | Cash is withdrawn from bank for office use Rs 2,000 |

| Mar.15 | Received three months post-dated cheque of Rs 20,000 from Raj and deposited in the bank on the same day, discounted from bank paying discounting charges Rs 750 |

| Mar.18 | Received cheque from Deepak for Rs 5,000 (not banked), allowed discount Rs 200 |

| Mar.20 | Cheque received from Deepak deposited in Bank |

| Mar.22 | Paid to Chandra by Cheque Rs 2,500; received discount Rs100 |

| Mar.25 | Withdrew from bank personal use Rs 1,000 |

| Mar.28 | Sold goods on credit to Ashok Mitra, Kolkata Rs 10,000, charged IGST@12% |

| Mar.30 | Purchased goods on credit from Chander, Delhi Rs 20,000, paid IGST@12% |

| Mar.31 | Received cheque from Ashok Mitra Rs 5,000 and deposited in the bank, allowed cash discount Rs 200 |

The solution of Question No 9 Chapter No 10: –

In the Books of Mani, Kochi

| Dr. | Cash Book | Cr. | |||||||

| Date | Particulars |

L.F. | Cash | Bank | Date | Particulars |

L.F. | Cash | Bank |

| Mar. 2018 | Mar. 2018 | ||||||||

| 1 | To Bal. B/d | 15,000 | 5,000 | 3 | To purchase A/c* | 5,780 | |||

| 5 | To Cash A/c | C | 5,000 | 3 | By Input CGST A/c | 360 | |||

| 7 | To Sale A/c* | 10,000 | 3 | By Input SGST A/c | 360 | ||||

| 7 | To Output CGST A/c | 600 | 5 | By Bank A/c | C | 5,000 | |||

| 7 | To Output SGST A/c | 600 | 10 | By Cash A/c | C | 2,000 | |||

| 10 | To Bank A/c | C | 2,000 | 22 | By Chandra A/c | 2,500 | |||

| 15 | To Raj A/c | 19,250 | 25 | By Drawing A/c | 1,000 | ||||

| 20 | To cheque in hand A/c | 5,000 | |||||||

| 31 | To Ashok Mitra A/c | 5,000 | 31 | By Balance C/d | 16,700 | 33,750 | |||

| 28,200 | 39,250 | 28,200 | 39,250 | ||||||

All transactions which are highlighted with (*) are explained as following as follows: –

*Mar.3 Purchased goods for Cash Rs 6,720 including CGST and SGST @ 6%p.a, received a discount of Rs 220

In this transaction, we will calculate the amount of CGST and SGST @ 6% each with help of following formula because the total amount is given. It means it includes the amount of CGST & SGST.

| Total Amount X Rate(CGST or SGST) |

| 100 + Rate of CGST + Rate of SGST |

| 6,720 X 6 |

| 100 + 6 + 6 |

| 40,320 |

| 112 |

Amount of GST =Rs. 360/- each

and subtract the amount of discount received of Rs. 220/-. So, total payable will be

= Total Invoice amount – CGST – SGCST – Cash Discount

= 6720-360-360-220

= 5,780/–

*Mar.30 Cash sale Rs 10,000 Plus CGST and SGST @6% each

The calculation of Amount of CGST and SGST @ 6% each

10,000 * 6% = 600/- each.

To understand more about cash book please check out following links: –

Cash Book | Types of Cash Book | Subsidiary Books

Single Column Cash Book | Explained with Example

Double Column Cash Book | Explained with Example

Triple Column Cash Book | Explained with Example

Petty Cash Book | Example | Subsidiary Books

Thanks Please share with your friends

Comment if you have any question.

Also, Check out previous Chapters: –

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping