Question No 8 Chapter No 10

With Goods and Services Tax (GST)

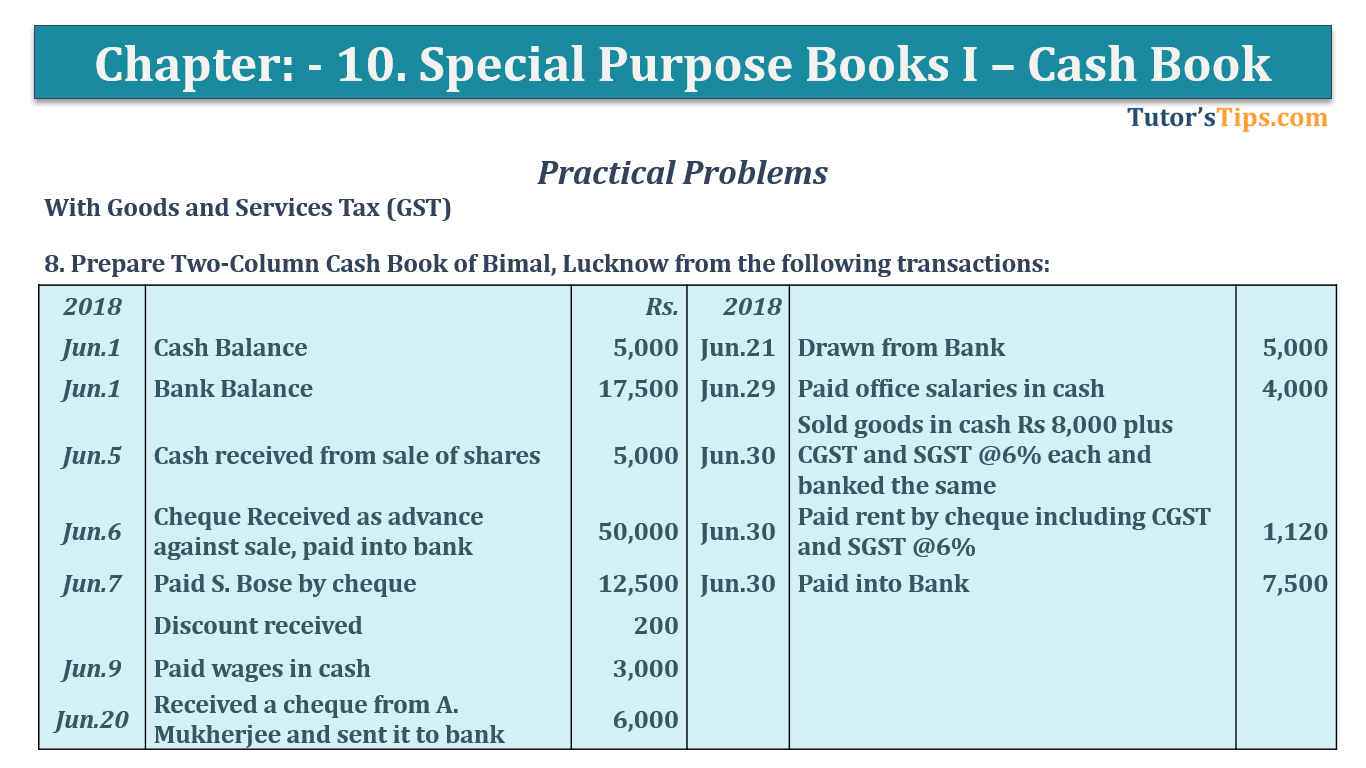

Prepare Two-Column Cash Book of Bimal, Lucknow from the following transactions:

| 2018 | Rs. | 2018 | Rs. | ||

| Jun.1 | Cash Balance | 5,000 | Jun.21 | Drawn from Bank | 5,000 |

| Jun.1 | Bank Balance | 17,500 | Jun.29 | Paid office salaries in cash | 4,000 |

| Jun.5 | Cash received from the sale of shares | 5,000 | Jun.30 | Sold goods in cash Rs 8,000 plus CGST and SGST @6% each and banked the same | |

| Jun.6 | Cheque Received as an advance against the sale, paid into a bank | 50,000 | Jun.30 | Paid rent by cheque including CGST and SGST @6% | 1,120 |

| Jun.7 | Paid S. Bose by cheque | 12,500 | Jun.30 | Paid into Bank | 7,500 |

| Discount received | 200 | ||||

| Jun.9 | Paid wages in cash | 3,000 | |||

| Jun.20 | Received a cheque from A. Mukherjee and sent it to bank | 6,000 |

The solution of Question No 8 Chapter No 10: –

In the Books of Mr Bimal, Lucknow

| Dr. | Cash Book | Cr. | |||||||

| Date | Particulars |

L.F. | Cash | Bank | Date | Particulars |

L.F. | Cash | Bank |

| Jun. 2018 | Jun. 2018 | ||||||||

| 1 | To Bal. B/d | 5,000 | 17,500 | 7 | To S. Bose A/c | 12,500 | |||

| 5 | To Investment A/c* | 5,000 | 9 | By Wages A/c | 3,000 | ||||

| 6 | To Adv. From Customer A/c* | 50,000 | 21 | By Cash A/c | C | 5,000 | |||

| 20 | To A. Mukherjee A/c | 6,000 | 29 | By Salaries A/c | 4,000 | ||||

| 21 | To Bank A/c | C | 5,000 | 30 | By Rent A/c* | 1,000 | |||

| 30 | To Sales A/c* | 8,000 | 30 | By Input CGST A/c | 60 | ||||

| 30 | To Output CGST A/c | 480 | 30 | By Input SGST A/c | 60 | ||||

| 30 | To Output SGST A/c | 480 | 30 | By Bank A/c | C | 7,500 | |||

| 21 | To Cash A/c | C | 7,500 | 30 | By Balance C/d | 500 | 71,340 | ||

| 15,000 | 89,960 | 15,000 | 89,960 | ||||||

All transactions which are highlighted with (*) are explained as following as follows: –

*Jun.5 Cash received from sale of shares

Share is our assets which is named as Investment, So that’s why we had used the account Investment while posting the transaction into cash book.

*Jun.6 Cheque Received as an advance against the sale, paid into a bank

Cheque received as an advance against sale but the name of the person or firm is not given. So, that’s why we have the account of Advance from the customer while posting the transaction into the cash book.

But in real-world, nothing will happen with you like this, Because the name of the customer will be written on the cheque.

*Jun.30 Sold goods in cash Rs 8,000 plus CGST and SGST @6% each and banked the same

The calculation of Amount of CGST and SGST @ 6% each

8,000 * 6% = 480/- each

*Jun.30 Sold goods in cash Rs 8,000 plus CGST and SGST @6% each and banked the same

In this transaction, we will calculate the amount of CGST and SGST @ 6% each with help of following formula because the total amount is given. It means it includes the amount of CGST & SGST.

| Total Amount X Rate(CGST or SGST) |

| 100 + Rate of CGST + Rate of SGST |

| 1,120 X 6 |

| 100 + 6 + 6 |

| 6,720 |

| 112 |

Amount of GST =Rs. 60/- each

To understand more about cash book please check out following links: –

Cash Book | Types of Cash Book | Subsidiary Books

Single Column Cash Book | Explained with Example

Double Column Cash Book | Explained with Example

Triple Column Cash Book | Explained with Example

Petty Cash Book | Example | Subsidiary Books

Thanks Please share with your friends

Comment if you have any question.

Also, Check out previous Chapters: –

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping