Question No 42 Chapter No 16 – Unimax Class 11

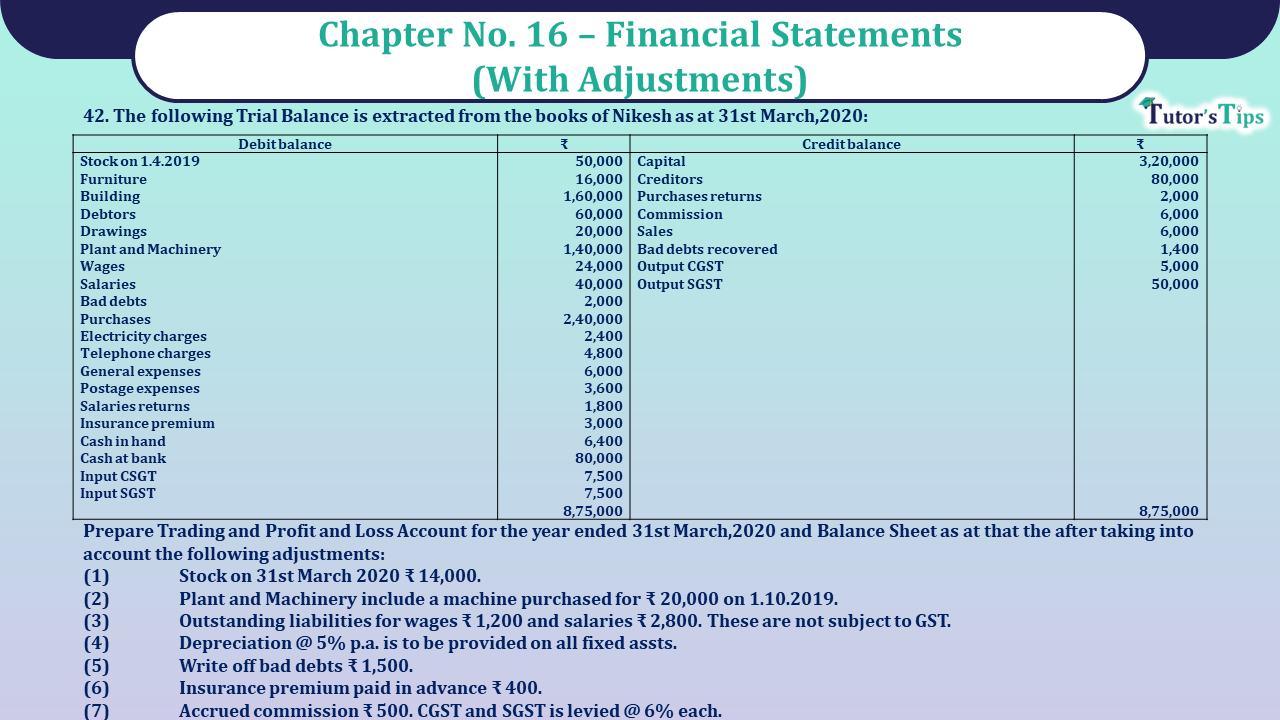

The following Trial Balance is extracted from the books of Nikesh as at 31st March,2020:

Trial balance

| Debit balance | ₹ | Credit balance | ₹ |

| Stock on 1.4.2019 | 50,000 | Capital | 3,20,000 |

| Furniture | 16,000 | Creditors | 80,000 |

| Building | 1,60,000 | Purchases returns | 2,000 |

| Debtors | 60,000 | Commission | 6,000 |

| Drawings | 20,000 | Sale | 4,55,600 |

| Plant and Machinery | 1,40,000 | Bad debts recovered | 1,400 |

| Wages | 24,000 | Output CGST | 5,000 |

| Salaries | 40,000 | Output SGST | 5,000 |

| Bad debts | 2,000 | ||

| Purchases | 2,40,000 | ||

| Electricity charges | 2,4000 | ||

| Telephone charges | 4,800 | ||

| General expenses | 6,000 | ||

| Postage expenses | 3,600 | ||

| Salaries returns | 1,800 | ||

| Insurance premium | 3,000 | ||

| Cash in hand | 6,400 | ||

| Cash at bank | 80,000 | ||

| Input CSGT | 7,500 | ||

| Input SGST | 7,500 | ||

| 8,75,000 | 8,75,000 |

Prepare Trading and Profit and Loss Account for the year ended 31st March,2020 and Balance Sheet as at that the after taking into account the following adjustments:

(1) Stock on 31st March 2020 ₹ 14,000.

(2) Plant and Machinery include a machine purchased for ₹ 20,000 on 1.10.2019.

(3) Outstanding liabilities for wages ₹ 1,200 and salaries ₹ 2,800. These are not subject to GST.

(4) Depreciation @ 5% p.a. is to be provided on all fixed assts.

(5) Write off bad debts ₹ 1,500.

(6) Insurance premium paid in advance ₹ 400.

(7) Accrued commission ₹ 500. CGST and SGST is levied @ 6% each.

The solution of Question No 42 Chapter No 16 – UNIMAX Class 11

Trading and Profit & Loss A/c of Nikesh

For the year ended 31st March, 2020

| Particulars | Amount | Particulars | Amount | ||

| To Opening stock | 50,0,00 | By sales | 4,55,600 | ||

| To purchases | 2,40,000 | Less: Returns | 1,800 | 4,53,800 | |

| Less: Returns | 2,000 | 2,38,000 | By Closing stock | 14,000 | |

| Wages | 24,000 | ||||

| Add: O/s Wages | 1,200 | 25,200 | |||

| To Gross Profit | 1,5,600 | ||||

| (transferred to P & L A/c) | |||||

| 4,67,800 | 4,67,800 | ||||

| To Salaries | 40,000 | By Gross Profit b/d | 1,54,600 | ||

| Add: Outstanding Salaries | 2,800 | 42,800 | By Commission | 6,000 | |

| To Bad debts | 2,000 | Add: Accrued Commission | 500 | 6,500 | |

| Add: Further bad debts | 1,500 | 3,500 | By bad debs Recovered | 1,400 | |

| To Electricity charges | 2,400 | ||||

| To Telephone charges | 4,800 | ||||

| To General expenses | 6,000 | ||||

| To Postage expenses | 3,600 | ||||

| To Insurance premium | 3,000 | ||||

| Less: Prepaid insurance | 400 | 2,600 | |||

| To Dep. Machinery & Plant | 6,500 | ||||

| To Dep. On Furniture | 800 | ||||

| To Dep. On Building | 8,000 | 15,300 | |||

| To Net Profit (Transferred to capital) |

81,500 | ||||

| 1,62,500 | 1,62,500 | ||||

Balance Sheet of Nikesh

AS 0n 31st March, 2020

| Liabilities | Amount | Assets | Amount | ||

| Current Liabilities | Current Assets | ||||

| Creditors | 80,000 | Cash in hand | 6,400 | ||

| Wages outstanding | 1,200 | Cash at bank | 80,000 | ||

| Salaries outstanding | 40,000 | Insurance prepaid | 400 | ||

| Capital | Accrued Commission | 560 | |||

| Opening Balance | 3,20,000 | Debtors | 60,000 | ||

| Add: Net Profit | 81,500 | Less: Bad debts | 1,500 | 58,500 | |

| 4,01,500 | Closing stock | 14,00 | |||

| Less: Drawings | 20,000 | 3,81,500 | Input CGST (7,500-5,000-30*) | 2,470 | |

| Input SGST (7,500-5,000-30*) | 2,470 | ||||

| Fixed Assets | |||||

| Plant and Machinery | 1,40,000 | ||||

| Less: Depreciation | 6,500 | 1,33,500 | |||

| Furniture | 16,000 | ||||

| Less: Depreciation | 800 | 15,200 | |||

| Building | 1,60,000 | ||||

| Less: Depreciation | 8,000 | 1,52,000 | |||

| 4,65,500 | 4,65,500 | ||||

Output CSGT on accrued commission= 6% of ₹ 500= ₹ 30;

Out put SGST on accrued commission= 6% of ₹ 500= ₹ 30.

Note: Input CGST and SGST is set off against output CGST. Similarly, input SGST is set off against output SGST.

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication