Question No 30 Chapter No 16 – Unimax Class 11

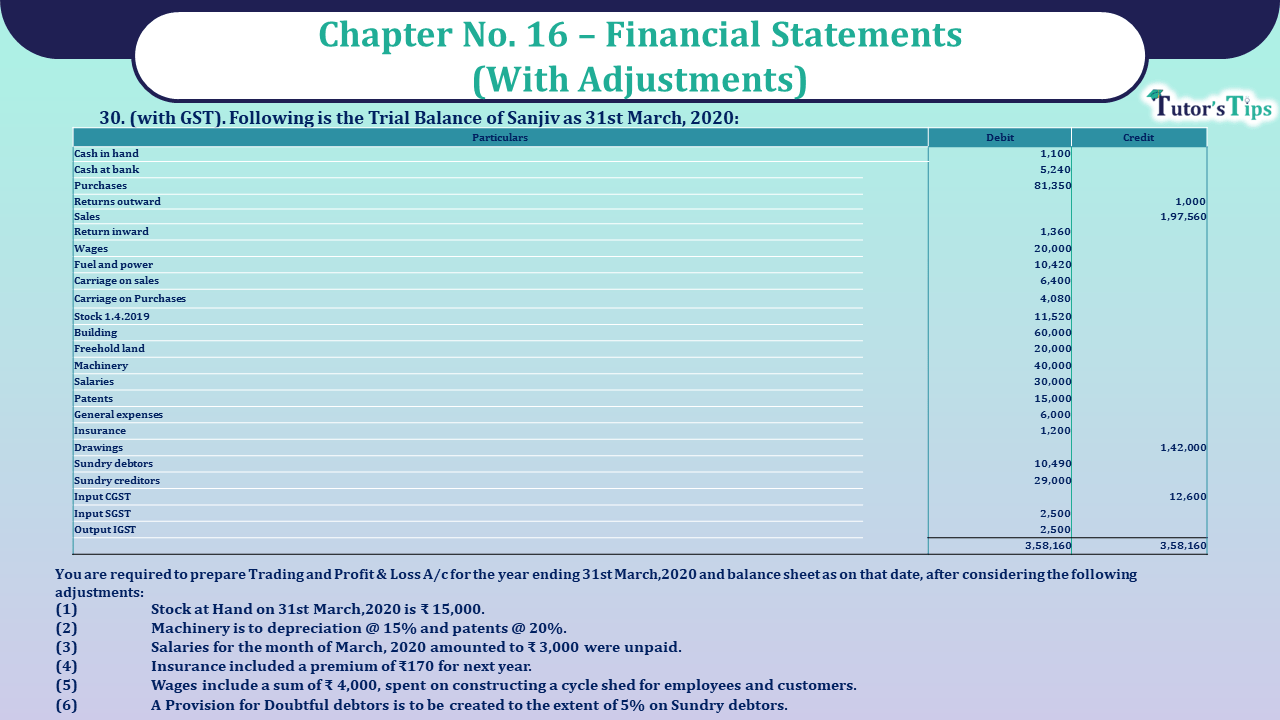

(with GST). Following is the Trial Balance of Sanjiv as 31st March, 2020:

| Particulars | Debit | Credit |

| Cash in hand | 1,100 | |

| Cash at bank | 5,240 | |

| Purchases | 81,350 | |

| Returns outward | 1,000 | |

| Sales | 1,97,560 | |

| Return inward | 1,360 | |

| Wages | 20,000 | |

| Fuel and power | 10,420 | |

| Carriage on sales | 6,400 | |

| Carriage on Purchases | 4,080 | |

| Stock 1.4.2019 | 11,520 | |

| Building | 60,000 | |

| Freehold land | 20,000 | |

| Machinery | 40,000 | |

| Salaries | 30,000 | |

| Patents | 15,000 | |

| General expenses | 6,000 | |

| Insurance | 1,200 | |

| Drawings | 1,42,000 | |

| Sundry debtors | 10,490 | |

| Sundry creditors | 29,000 | |

| Input CGST | 12,600 | |

| Input SGST | 2,500 | |

| Output IGST | 2,500 | |

| 3,58,160 | 3,58,160 |

You are required to prepare Trading and Profit & Loss A/c for the year ending 31st March,2020 and balance sheet as on that date, after considering the following adjustments:

(1) Stock at Hand on 31st March,2020 is ₹ 15,000.

(2) Machinery is to depreciation @ 15% and patents @ 20%.

(3) Salaries for the month of March, 2020 amounted to ₹ 3,000 were unpaid.

(4) Insurance included a premium of ₹170 for next year.

(5) Wages include a sum of ₹ 4,000, spent on constructing a cycle shed for employees and customers.

(6) A Provision for Doubtful debtors is to be created to the extent of 5% on Sundry debtors.

The solution of Question No 30 Chapter No 16 – UNIMAX Class 11

| Trading and Profit & Loss A/c of Sanjiv For the year ended 31st March, 2020 |

|||||

| Particulars |

Amount | Particulars |

Amount | ||

| To Opening stock | 11,520 | By sales | 1,97,560 | ||

| To purchases | 81,350 | Less: Returns inwards | 1,360 | 1,96,200 | |

| Less: Returns outwards | 1,000 | 80,350 | By Closing stock | 15,000 | |

| To Wages | 20,000 | ||||

| Less: Wages spent on cycle shed | 4,000 | 16,000 | |||

| To Fuel and power | 10.420 | ||||

| To Carriage on purchases | 4,080 | ||||

| To Gross Profit | 88,830 | ||||

| (transferred to P & L A/c) | |||||

| 2,11,200 | 2,11,200 | ||||

| To Carriage on sales | 6,400 | By Gross Profit b/d | 88,830 | ||

| To salaries | 30,000 | ||||

| Add: outstanding salaries | 3,000 | 33,000 | |||

| To General expenses | |||||

| To Insurance | 1,200 | ||||

| Less: Prepaid | 170 | 1,030 | |||

| To depreciation on | |||||

| Machinery @ 15% | 6,000 | ||||

| Patents @ 20% | 3,000 | 9,000 | |||

| To Provision for Doubtful debts | 1,450 | ||||

| To Net Profit | |||||

| (Transferred to capital) | 31,950 | ||||

| 88,830 | 88,830 | ||||

Balance Sheet of Sanjiv As on 31st Dec., 2020 |

|||||

| Liabilities | Amount | Assets | Amount | ||

| Capital | 1,42,000 | Building | 60,000 | ||

| Add: Net Profit | 31,950 | Add: wages spend on cycle shed | 4,000 | 64,000 | |

| 1,73,950 | Freehold land | 20,000 | |||

| Less: Drawings | 10,490 | 1,63,460 | Machinery | 40,000 | |

| Creditors | 12,600 | Less: Depreciation | 6,000 | 34,000 | |

| Outstanding salaries | 3,000 | Patents | 15,000 | ||

| Less: Depreciation | 3,000 | 12,000 | |||

| Debtors | 29,000 | ||||

| Less Provision for doubtful debts | 1,450 | 27,550 | |||

| Prepaid insurance | 170 | ||||

| Closing stock | 15,000 | ||||

| Cash in hand | 1,100 | ||||

| Cash at bank | 5,240 | ||||

| 1,79,060 | 1,79,060 | ||||

note:

1. Wages paid for constructing a cycle shed being capital expenditure should be debited to the building account.

2. Input CGST (₹ 2,500) and Input SGST (₹ 2,500 are set off against Output IGST (₹ 5,000).

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

Question No 30 Chapter No 16 – Unimax Class 11

(with GST). Following is the Trial Balance of Sanjiv as 31st March, 2020:

| Particulars | Debit | Credit |

| Cash in hand | 1,100 | |

| Cash at bank | 5,240 | |

| Purchases | 81,350 | |

| Returns outward | 1,000 | |

| Sales | 1,97,560 | |

| Return inward | 1,360 | |

| Wages | 20,000 | |

| Fuel and power | 10,420 | |

| Carriage on sales | 6,400 | |

| Carriage on Purchases | 4,080 | |

| Stock 1.4.2019 | 11,520 | |

| Building | 60,000 | |

| Freehold land | 20,000 | |

| Machinery | 40,000 | |

| Salaries | 30,000 | |

| Patents | 15,000 | |

| General expenses | 6,000 | |

| Insurance | 1,200 | |

| Drawings | 1,42,000 | |

| Sundry debtors | 10,490 | |

| Sundry creditors | 29,000 | |

| Input CGST | 12,600 | |

| Input SGST | 2,500 | |

| Output IGST | 2,500 | |

| 3,58,160 | 3,58,160 |

You are required to prepare Trading and Profit & Loss A/c for the year ending 31st March,2020 and balance sheet as on that date, after considering the following adjustments:

(1) Stock at Hand on 31st March,2020 is ₹ 15,000.

(2) Machinery is to depreciation @ 15% and patents @ 20%.

(3) Salaries for the month of March, 2020 amounted to ₹ 3,000 were unpaid.

(4) Insurance included a premium of ₹170 for next year.

(5) Wages include a sum of ₹ 4,000, spent on constructing a cycle shed for employees and customers.

(6) A Provision for Doubtful debtors is to be created to the extent of 5% on Sundry debtors.

The solution of Question No 30 Chapter No 16 – UNIMAX Class 11

| Trading and Profit & Loss A/c of Sanjiv For the year ended 31st March, 2020 |

|||||

| Particulars |

Amount | Particulars |

Amount | ||

| To Opening stock | 11,520 | By sales | 1,97,560 | ||

| To purchases | 81,350 | Less: Returns inwards | 1,360 | 1,96,200 | |

| Less: Returns outwards | 1,000 | 80,350 | By Closing stock | 15,000 | |

| To Wages | 20,000 | ||||

| Less: Wages spent on cycle shed | 4,000 | 16,000 | |||

| To Fuel and power | 10.420 | ||||

| To Carriage on purchases | 4,080 | ||||

| To Gross Profit | 88,830 | ||||

| (transferred to P & L A/c) | |||||

| 2,11,200 | 2,11,200 | ||||

| To Carriage on sales | 6,400 | By Gross Profit b/d | 88,830 | ||

| To salaries | 30,000 | ||||

| Add: outstanding salaries | 3,000 | 33,000 | |||

| To General expenses | |||||

| To Insurance | 1,200 | ||||

| Less: Prepaid | 170 | 1,030 | |||

| To depreciation on | |||||

| Machinery @ 15% | 6,000 | ||||

| Patents @ 20% | 3,000 | 9,000 | |||

| To Provision for Doubtful debts | 1,450 | ||||

| To Net Profit | |||||

| (Transferred to capital) | 31,950 | ||||

| 88,830 | 88,830 | ||||

Balance Sheet of Sanjiv As on 31st Dec., 2020 |

|||||

| Liabilities | Amount | Assets | Amount | ||

| Capital | 1,42,000 | Building | 60,000 | ||

| Add: Net Profit | 31,950 | Add: wages spend on cycle shed | 4,000 | 64,000 | |

| 1,73,950 | Freehold land | 20,000 | |||

| Less: Drawings | 10,490 | 1,63,460 | Machinery | 40,000 | |

| Creditors | 12,600 | Less: Depreciation | 6,000 | 34,000 | |

| Outstanding salaries | 3,000 | Patents | 15,000 | ||

| Less: Depreciation | 3,000 | 12,000 | |||

| Debtors | 29,000 | ||||

| Less Provision for doubtful debts | 1,450 | 27,550 | |||

| Prepaid insurance | 170 | ||||

| Closing stock | 15,000 | ||||

| Cash in hand | 1,100 | ||||

| Cash at bank | 5,240 | ||||

| 1,79,060 | 1,79,060 | ||||

note:

1. Wages paid for constructing a cycle shed being capital expenditure should be debited to the building account.

2. Input CGST (₹ 2,500) and Input SGST (₹ 2,500 are set off against Output IGST (₹ 5,000).

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication