Question No 29 Chapter No 18

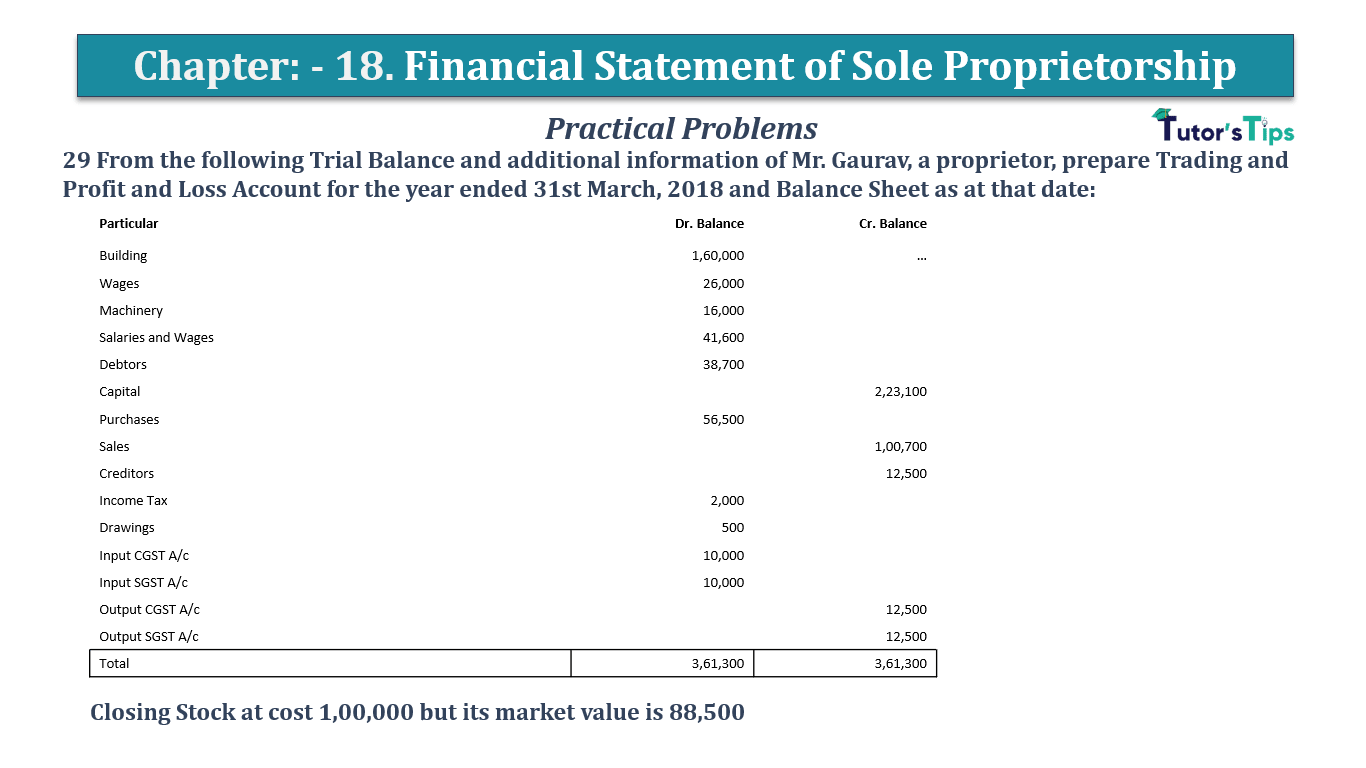

29 From the following Trial Balance and additional information of Mr. Gaurav, a proprietor, prepare Trading and Profit and Loss Account for the year ended 31st March, 2018 and Balance Sheet as at that date:

| Particular | Dr. Balance | Cr. Balance |

| Building | 1,60,000 | … |

| Wages | 26,000 | |

| Machinery | 16,000 | |

| Salaries and Wages | 41,600 | |

| Debtors | 38,700 | |

| Capital | 2,23,100 | |

| Purchases | 56,500 | |

| Sales | 1,00,700 | |

| Creditors | 12,500 | |

| Income Tax | 2,000 | |

| Drawings | 500 | |

| Input CGST A/c | 10,000 | |

| Input SGST A/c | 10,000 | |

| Output CGST A/c | 12,500 | |

| Output SGST A/c | 12,500 | |

| Total | 3,61,300 | 3,61,300 |

Closing Stock at cost 1,00,000 but its market value is 88,500

The solution of Question No 29 Chapter No 18:-

| Trading Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Purchases | 56,500 | By Sales | 1,00,700 | ||

| To Wages | 26,000 | By Closing Stock | 88,500 | ||

| To Gross Profit | 1,06,700 | ||||

| 1,89,200 | 1,89,200 | ||||

| Profit and Loss Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Salaries and Wages | 25,000 | By Gross Profit | 1,06,700 | ||

| To Net Profit | 65,100 | ||||

| 1,06,700 | 1,06,700 | ||||

| Balance Sheet |

|||||

| Particular |

Amount | Particular |

Amount | ||

| Capital | 2,23,100 | Building | 1,60,000 | ||

| Add: Net Profit | 65,100 | Machinery | 16,000 | ||

| Less: Drawings | 500 | Closing Stock | 88,500 | ||

| Less: Income Tax | 2, 000 | 2,85,700 | Sundry Debtor | 38,700 | |

| Creditors | 12,500 | ||||

| GST Payable | 5,000 | ||||

| 3,03,200 | 3,03,200 | ||||

Working Notes:

1 GST Set off First: Output CGST-Input CGST= 12,500-10,000=2,500

Second: Output SGST-Input SGST= 12,500-10,000=2,500

GST Payable=Output CGST+Output SGST=2,500+2,500=5,000

2 Closing Stock has been taken at its Market Price i. e. Rs88, 500

and not on its Cost. This is because, as per the Principle of Conservatism, Closing Stock is taken at Cost or Market Price whichever is less.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

-

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping