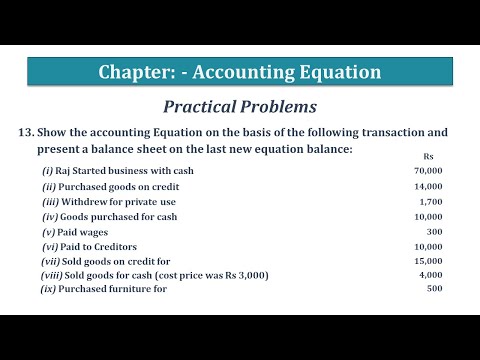

Question No 13 Chapter No 5

13 Show the accounting Equation on the basis of the following transaction and present a balance sheet on the last new equation balance:

(i) Raj Started business with cash 70,000

(ii) Purchased goods on credit 14,000

(iii) Withdrew for private use 1,700

(iv) Goods purchased for cash 10,000

(v) Paid wages 300

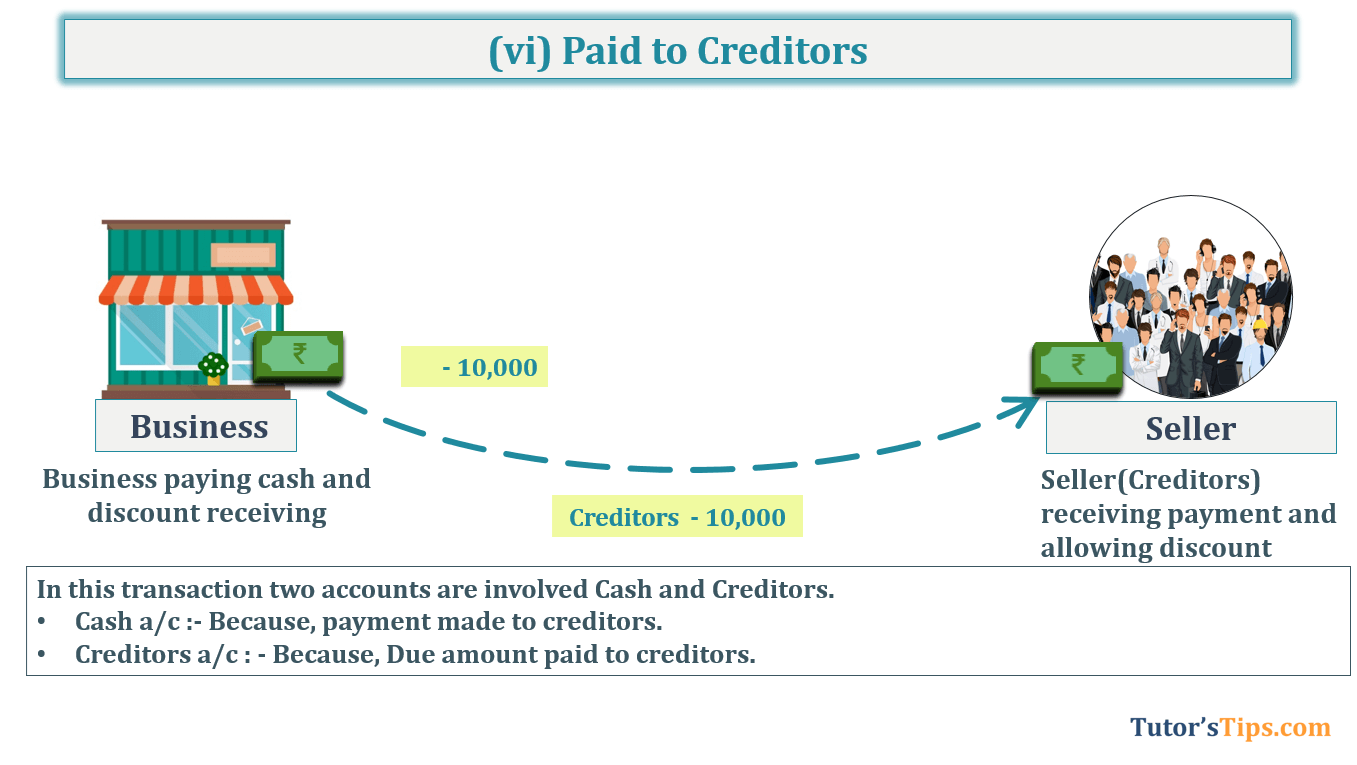

(vi) Paid to Creditors 10,000

(vii) Sold goods on credit for 15,000

(viii) Sold goods for cash (cost price was Rs 3,000) 4,000

(ix) Purchased furniture for 500

Solution of Question No 13 Chapter No 5: –

Subscribe our Youtube Channel

| S. No. | Particulars | Assets |

Liabilities |

Capital | |||

| +Cash | +Stock | +Debtors | +Fur. |

+Creditors | |||

| (i) | Raj Started business with cash 70,000 |

+70,000 |

+70,000 |

||||

| 70,000 | +70,000 | ||||||

| (ii) | Purchased goods on credit 14,000 | +14,000 | +14,000 | ||||

| 70,000 | +14,000 | 14,000 | +70,000 | ||||

| (iii) | Withdrew for private use 1,700 |

-1,700 |

-1,700 |

||||

| 68,300 | 14,000 | 14,000 | +68,300 | ||||

| (iv) | Goods purchased for cash 10,000 | -10,000 | +10,000 | ||||

| 58,300 | +24,000 | 14,000 | +68,300 | ||||

| (v) | Paid wages 300 | -300 | -300 | ||||

| 58,000 | +24,000 | 14,000 | +68,000 | ||||

| (vi) | Paid to Creditors 10,000 | -10,000 | -10,000 | ||||

| 48,000 | +24,000 | 4,000 | +68,000 | ||||

| (vii) | Sold goods on credit for 15,000 | -15,000 | +15,000 | ||||

| 48,000 | +9,000 | +15,000 | 4,000 | +68,000 | |||

| (viii) | Sold goods for cash (cost price was Rs 3,000) 4,000 | +4,000 | -3,000 | +1,000 | |||

| 52,000 | +6,000 | +15,000 | 4,000 | +69,000 | |||

| (ix) | Purchased furniture for 500 | -500 | +500 | ||||

| Total | 51,500 | +6,000 | +15,000 | +500 | 4,000 | +69,000 | |

Answer: –

Assets: – Cash 51,500 + + Stock 6,000 + Debtors 15,000 + Furniture 500 = 73,000/-

Liabilities: – Creditors 4,000 = 4,000/-

Capital = 69,000/-

Liabilities +Capital

4,000 + 69,000 = 73,000/-

Explanation of All Transactions with images: –

This is not a part of the solution, So you don’t have to write it in the exam. So why we explained if it is not needed. Because This explanation will help you to understand all transactions with logic so don’t need to remember all the transactions but just understand and remember the logic use behind it.

Transaction No. 1

As we discuss in the previous topic, A owner and a business both have a separate identity in the eye of law. So, the business will be treated as an Artificial Person and anything invested by the owner into the business will be treated as capital.

So, In this transaction, as shown in the above image owner investing her cash into the business, this will be treated as capital of the business. The business receiving an asset i.e. cash.

Transaction No. 2

In this transaction, as shown in the above image two accounts are involved Stock (Purchase) and Creditor

- Stock:- Because business receiving goods.

- Creditor: – Because Businesses bought goods on credit, they did not pay anything. But it has to pay in the future. so that’s why Seller becomes our creditor.

Transaction No. 3

In this transaction, as shown in the above image three accounts are involved i.e. one is cash and another is capital.

- Cash a/c: – payment is made in cash.

- Capital a/c:- cash withdrawal by the owner

Transaction No. 4

In this transaction, as shown in the above image two accounts are involved i.e. Stock(Purchase) and Cash:

- Stock a/c (Purchase):- Because business receiving goods.

- Cash a/c: – Because business paying due amount in cash.

Transaction No. 5

In this transaction, as shown in the above image two accounts are involved i.e. cash and capital

- Cash A/c: – Because business cash goes out of the business.

- Capital a/c:- because business gets services from its workers and paid them for it. So these is expenses for the business. “ All expenses and losses are deducted from the amount of capital.

Transaction No. 6

In this transaction, as shown in the above image two accounts are involved i.e. Cash and Creditors.

- Cash a/c:- Because payment made to creditors.

- Creditors a/c: – Because, Due amount paid to creditors.

Transaction No. 7

In this transaction, as shown in the above image two accounts are involved i.e. Stock(Sale) and Debtors:

- Stock a/c (Sale):- Because of business giving(selling) its goods.

- Debtors (Sohan): – Because the Business sold goods on credit, the Customer did not pay anything. That’s why he has to pay in the future to us, so that’s why Shyam becomes our Debtors.

Note: The cost of goods sold is not given So, we treat it as no profit and no loss.

Transaction No. 8

In this transaction, as shown in the above image two accounts are involved i.e. Stock(Sale), Cash and Capital(Profit):

- Stock a/c (Sale):- Because of business giving(selling) its goods.

- Cash: – Because Business received cash from the customer.

- Capital(Profit): Because the owner has right on all profit of the business so the amount of the profit will be added in the capital a/c. (Profit = sale price – cost price) 4,000-3,000 = 1,000(Profit)

Transaction No. 9

In this transaction, as shown in the above image two accounts are involved i.e. Furniture and Cash:

- Furniture a/c (Purchase):- Because business receiving Furniture.

- Cash a/c: – Because the business transaction is not clear about the payment so it assumed that it is paid in cash.

Thanks Please share with your friends

Comment if you have any question.

T.S. Grewal’s Double Entry Book Keeping (Class +1) – Solution

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

Check out T.S. Grewal’s +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping