Question No 14 Chapter No 15 – Unimax Class 11

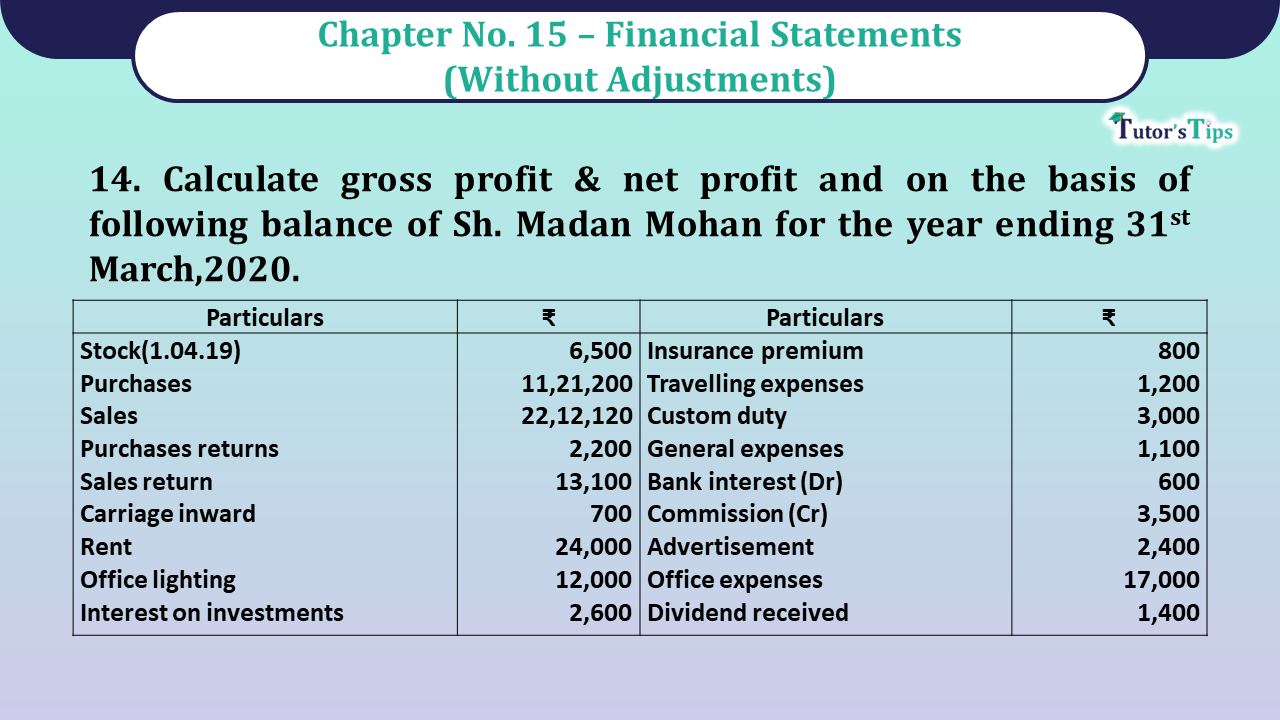

Calculate gross profit & net profit and on the basis of following balance of Sh. Madan Mohan for the year ending 31st March,2020

| Particular | ₹ | Particular | ₹ |

| Stock(1.04.19) | 6,500 | Insurance premium | 800 |

| Purchases | 11,21,200 | Travelling expenses | 1,200 |

| Sales | 22,12,120 | Custom duty | 3,000 |

| Purchases returns | 2,200 | General expenses | 1,100 |

| Sales return | 13,100 | Bank interest (D r) | 600 |

| Carriage inward | 700 | Commission (Cr) | 3,500 |

| Rent | 24,000 | Advertisement | 2,400 |

| Office lighting | 12,000 | Office expenses | 17,000 |

| Interest on investments | 2,600 | Dividend received | 1,400 |

Closing stock was valued at ₹22,00.

The solution of Question No 14 Chapter No 15 – UNIMAX Class 11

We know that: Gross profit = Net Sales – Coat of goods sold

Net profit =

Cost of goods sold = opening stock + Net purchases + Direct expense – closing stock

| Trading A/c, Profit & Loss A/c of MADAN MOHAN for the year ended 31st March, 2020 | |||||

| Particular |

Amount | Particular |

Amount | ||

| To Opening stock | 6,500 | By Sales | 2212,120 | ||

| To Purchases | 11,21,200 | Less return | 13,100 | 21,99,020 | |

| Less returns | 2,200 | 11,19,000 | By Closing stock | 22,000 | |

| To Customer duty | 3,000 | ||||

| To Carriage inwards | 7,000 | ||||

| To Gross profit c/d (and transferred to P&L a/c) |

10,91,820 | ||||

| 22,21,020 | 22,21,020 | ||||

| To Rent | 24,000 | By Gross profit b/d | 10,91,820 | ||

| To Office lighting | 12,000 | By Commission | 3,500 | ||

| To Travelling expenses | 1,200 | By Dividend received | 1,400 | ||

| To General expenses | 1,100 | By Interest on investments | 2,600 | ||

| To Bank interest | 600 | ||||

| To Advertisement | 2,400 | ||||

| To Office expenses | 17,000 | ||||

| To Insurance premium | 800 | ||||

| To Net profit (and transferred to capital) |

10,40,220 | ||||

| 10,99,320 | 10,99,320 | ||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Also, Check out the solved question of all Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST): An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Computers and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software: Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication