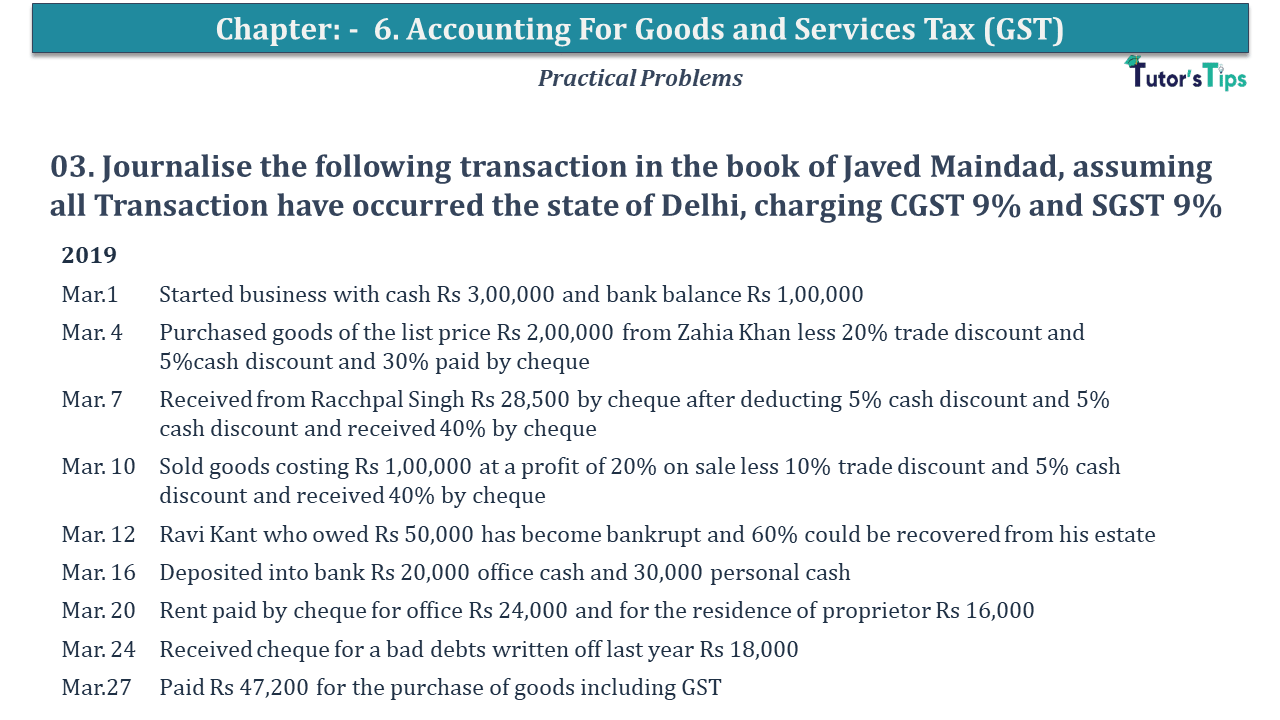

Question No 04 Chapter No 6

04. Journalise the following transaction in the book of Javed Miandad, assuming all Transaction has occurred the state of J&K, charging CGST 9% and SGST 9%

| 2019 | |

| Mar.1 | Started business with cash Rs 3,00,000 and bank balance Rs 1,00,000 |

| Mar. 4 | Purchased goods of the list price Rs 2,00,000 from Zahia Khan less 20% trade discount and 5%cash discount and 30% paid by cheque |

| Mar. 7 | Received from Racchpal Singh Rs 28,500 by cheque after deducting 5% cash discount and 5% cash discount and received 40% by cheque |

| Mar. 10 | Sold goods costing Rs 1,00,000 at a profit of 20% on sale less 10% trade discount and 5% cash discount and received 40% by cheque |

| Mar. 12 | Ravi Kant who owed Rs 50,000 has become bankrupt and 60% could be recovered from his estate |

| Mar. 16 | Deposited into bank Rs 20,000 office cash and 30,000 personal cash |

| Mar. 20 | Rent paid by cheque for office Rs 24,000 and for the residence of proprietor Rs 16,000 |

| Mar. 24 | Received cheque for a bad debt written off last year Rs 18,000 |

| Mar.27 | Paid Rs 47,200 for the purchase of goods including GST |

The solution of Question No 04 Chapter No 6: –

| In the Books of Javed Miandad | |||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2019 | |||||

| Mar. 1 | Cash A/c | Dr. | 3,00,000 | ||

| Bank A/c | Dr. | 1,00,000 | |||

| To Mamta A/c | 4,00,000 | ||||

| (Being started business with cash and bank balance. ) | |||||

| Mar. 4 | Purchases A/c | Dr. | 1,60,000 | ||

| Input CGST A/c | Dr. | 14,400 | |||

| Input SGST A/c | Dr. | 14,400 | |||

| To Bank A/c | 53,808 | ||||

| To Zahir Khan A/c | 1,32,160 | ||||

| To Discount Received A/c | 2,832 | ||||

| (Being goods bought from Zahir Khan less 20% trade Discount and cash discount of 5% plus 9% CGST and SGST. ) | |||||

| Mar. 7 | Bank A/c | Dr. | 28,500 | ||

| Discount allowed A/c | Dr. | 1,500 | |||

| To Racchpal A/c | 30,000 | ||||

| (Being cheque received from Racchpal Singh after deducting 55 Cash discount. ) | |||||

| Mar. 10 | Bank A/c | Dr. | 50,445 | ||

| Creditor A/c | Dr. | 79,650 | |||

| Discount Allowed A/c | Dr. | 2,655 | |||

| To Sale A/c | 1,12,500 | ||||

| To Output CGST A/c | 10,125 | ||||

| To Output SGST A/c | 10,125 | ||||

| (Being goods sold to creditor less 10% trade discount and 5% cash Discount and 40% received by cheque plus 9% CGST and SGST) | |||||

| Mar. 12 | Bank A/c | Dr. | 30,000 | ||

| Bad debts A/c | Dr. | 20,000 | |||

| To Kavi Kant A/c | 50,000 | ||||

| (Being Ravi become bankrupt only 60% cloud be recovered. ) | |||||

| Mar. 16 | Bank A/c | Dr. | 50,000 | ||

| To Cash A/c | 20,000 | ||||

| To Capital A/c | 30,000 | ||||

| (Being cash deposited into bank by the office and by proprietor ) | |||||

| Mar. 20 | Rent A/c | Dr. | 20,000 | ||

| Input CGST A/c | Dr. | 1,800 | |||

| Input SGST A/c | Dr. | 1,800 | |||

| To Bank A/c | 23,600 | ||||

| (Being rent paid by cheque plus 9% CGST and SGST. ) | |||||

| Mar. 20 | Drawing A/c | Dr. | 16,000 | ||

| To Bank A/c | 16,000 | ||||

| (Being rent to proprietor house paid ) | |||||

| Mar. 24 | Bank A/c | Dr. | 18,000 | ||

| To Bad debts recovered A/c | 18,000 | ||||

| (Being bad debts recovered. ) | |||||

| Mar. 27 | Purchases A/c | Dr. | 40,000 | ||

| Input CGST A/c | Dr. | 3,600 | |||

| Input SGST A/c | Dr. | 3,600 | |||

| To Cash A/c | 47,600 | ||||

| (Being purchased goods including 9% CGST and SGST. ) | |||||

What is Accounting Equation | Example

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)