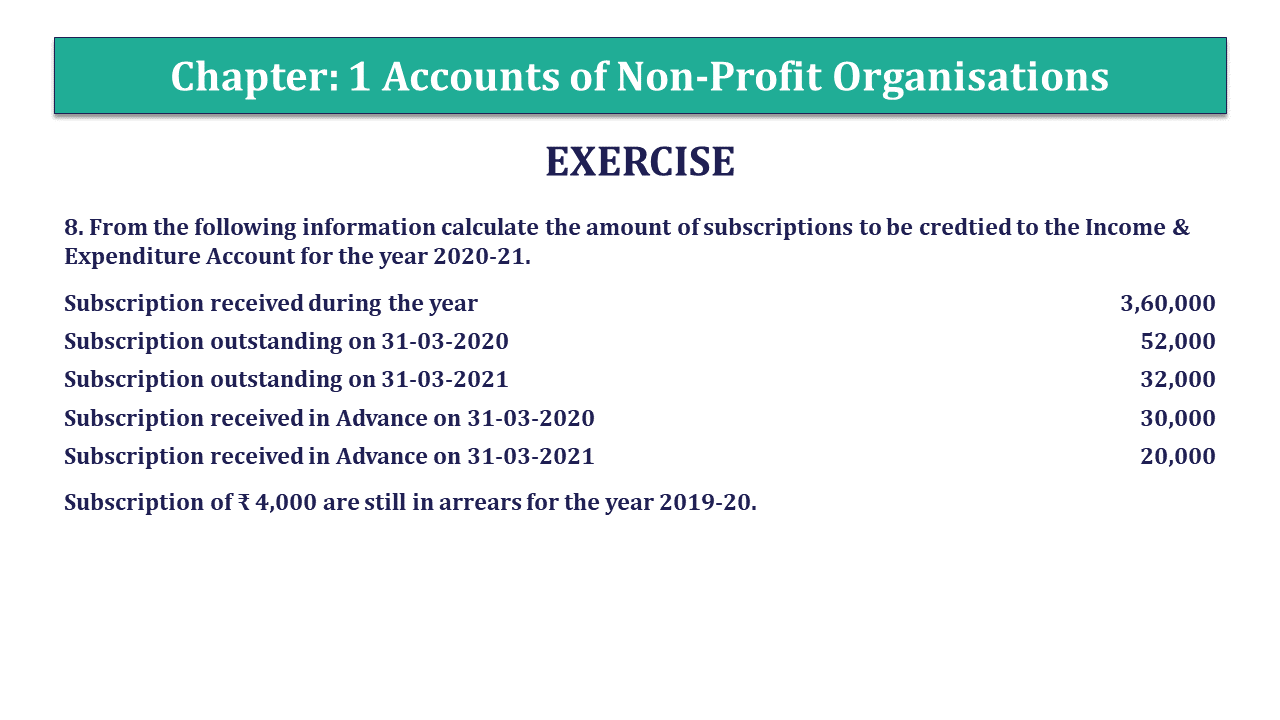

Question 8 Chapter 1 – Unimax Class 12 Part 1

8. From the following information calculate the amount of subscriptions to be credited to the Income & Expenditure Account for the year 2020-21.

| Subscription received during the year | 3,60,000 |

| Subscription outstanding on 31-03-2020 | 52,000 |

| Subscription outstanding on 31-03-2021 | 32,000 |

| Subscription received in Advance on 31-03-2020 | 30,000 |

| Subscription received in Advance on 31-03-2021 | 20,000 |

Subscription of ₹ 4,000 are still in arrears for the year 2019-20.

The solution of Question 8 Chapter 1 – Unimax Class 12 Part 1:

| Particulars | Amount | |

| Subscription received during the year | 3,60,000 | |

| Add: – Subscription outstanding on 31-03-2021 | 32,000 | |

| Add: – Subscription received in Advance on 31-03-2020 | 30,000 | 62,000 |

| 4,22,000 | ||

| Less: – Subscription received in Advance on 31-03-2021 | 20,000 | |

| Less: – Subscription outstanding on 31-03-2020 | 52,000 | 72,000 |

| Amt. of stationery to be posted in income and Expenditure A/c | 3,50,000 | |

It is all about Question 8 Chapter 1 of Class 12 unimax, If you have any problem please comment below.

Read out the full article to know the meaning of Not for Profit Organisations

Not-for-Profit Organisations – Meaning and Overview

Also, Check out the same article in Hindi from the following link

Not-for-Profit Organisations – Meaning and Overview

Also, Check out the solved question of all Chapters: –

Accountancy – Unimax Class 12 Part 1 – 2021 – Solution.

Chapter No. 1 – Accounts of Non-Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Basic Concepts)

Chapter No. 3 – Partnership Accounts – II (Goodwill)

Chapter No. 4 – Partnership Accounts – III (Change in Profit Sharing Ratio among Existing Partners)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

Chapter No. 1 – Accounting Not for Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Introduction)

Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement