Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Today, we are covering the slightly easier and less conceptual topic of the trial balance. It is just a posting of balances from the ledger into it. We will learn the meaning of a trial balance, its advantages, and methods, and to understand it in many better ways, we will solve an example with all the methods. After reading this article, you can prepare and check the trial balance of any business.

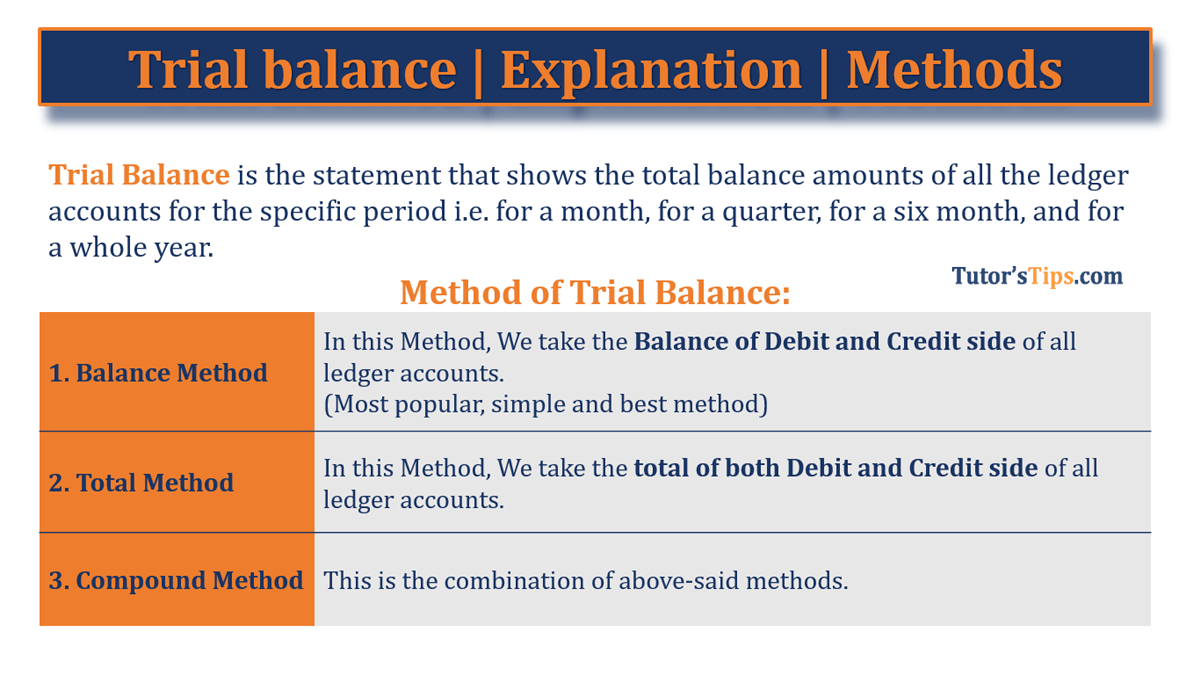

It shows the total closing balanced amounts of all the ledger accounts for the specific period, i.e. for a month, for a quarter, for six months, and for a whole year. It is the end of the accounting process. In the double-entry accounting system, there is always the same amount of Credit corresponding to every Debit. So, the Total trial balance is equal; if not, then there is an error in the posting of the transactions.

In a manual system of accounting:-

An accountant needs to prepare the trial balance. He matched the Debit balance amounts with the credit balance amounts. If they agree, it means that it has no error of omission, commission, etc. We will discuss the meaning of all these errors in a separate upcoming article.

Note: -

Nowadays, in the computerised system of accounting:-

An accountant doesn't need to prepare a trial balance because it will be prepared automatically by the accounting software (Like Tally, SAP, ZOHO, Marg, etc.). An accountant just has to post all business transactions in the subsidiary books of accounting, i.e. Cash Book, Purchase Book, Sales Book, Purchase Return Book, Sales Return Book, and last is Journal Proper.

The following advantages are common in both systems: -

The following are the three methods of Trial Balance: -

| 1. Balance Method | In this Method, We take the Balance of the Debit and Credit sides of all ledger accounts.(Most popular, simple and best method) |

| 2. Total Method | In this Method, We take the total of both the Debit and Credit sides of all ledger accounts. |

| 3. Compound Method | This is a combination of the above-said methods. |

We are taking a single example, and then we will prepare a trial balance with all the above-said three methods: -

Prepare a trial balance of A&B co. as on 30/04/18 with all three methods.

| Date | Transaction | Amount |

|---|---|---|

| Cash | 20,000 | |

| Bank | 100,000 | |

| Land and Building | 2,000,000 | |

| Furniture and fixture | 230,000 | |

| Office Equipment | 150,000 | |

| 05/04/2018 | Purchase goods from M/s Ram and Sons. | 250,000 |

| 05/04/2018 | Paid Freight by cash | 5,000 |

| 07/04/2018 | Paid for Stationery Items | 2,000 |

| 09/04/2018 | Sold goods to Mr. Parvesh Kumar | 85,000 |

| 12/04/2018 | Paid to M/s Ram and Sons by cheque | 150,000 |

| 15/04/2018 | Purchase goods from M/s Ram and Sons. | 200,000 |

| 15/04/2018 | Paid Freight by cash | 3,000 |

| 18/04/2018 | Sold goods to Miss. Deepika and payment received by cheque | 125,000 |

| 21/04/2018 | Payment received from Mr. Parvesh Kumar by cheque | 85,000 |

| 25/04/2018 | Sold goods to M/s A&B Co. | 135,000 |

| 28/04/2018 | Sold Goods to M/s X&Y Co. | 150,000 |

"Download Example in PDF format"

First of all, we have to post all the above transactions in the journal.

"Download all Journal entries in PDF Format"

And after that, we have to post all journal entries in the ledger accounts. It's also attached.

"Download all Ledger accounts in PDF format"

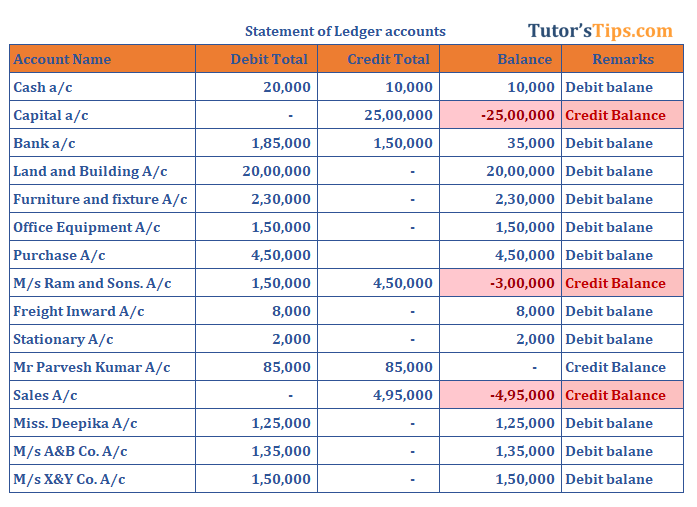

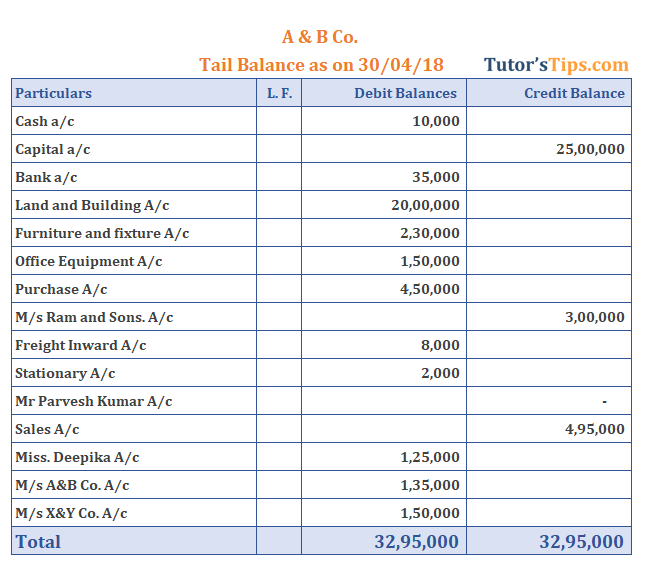

After taking the above steps, we got a statement of ledger accounts, including the total of the debit side, the total of the credit side and balances shown as follows: -

Now we will prepare Trial Balances with all three methods: -

In the balance method, we have to post all the Debit balances shown in the column of "Balances" in the above statement of ledger accounts in the trial balance column named "Debit Balances" and the credit balance in the column named "Credit Balances".

"Important Note: - Trial balance always has equal total in both the column named debit Balance and credit balance."

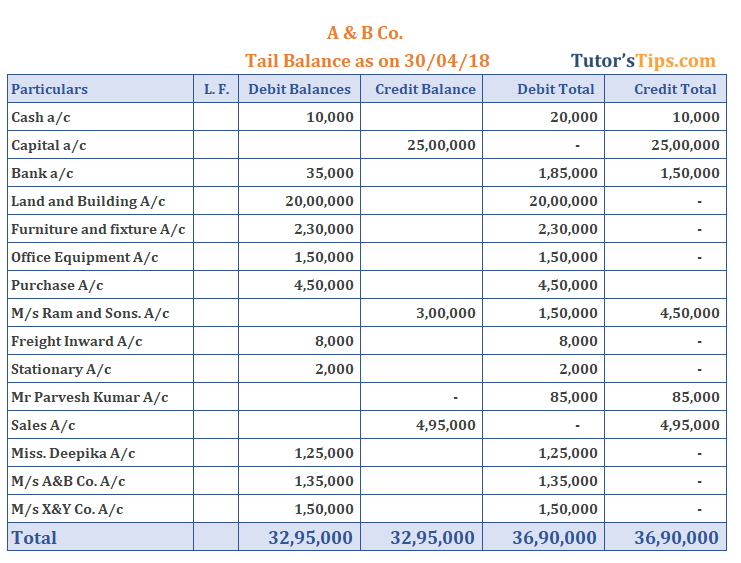

In the Total method, we have to post all the total amounts of the debit side of all ledger accounts shown in the column of "Debit Total" in the above statement of ledger accounts in the trial balance column named "Debit Total" and the credit total in the column named "Credit Total".

Trial Balance - Solved with Total Method

The Compound method is the mixture of both the above-explained methods, or we can say that shows both methods on a single sheet. As shown below: -

Trial Balance - Solved with Compound Method

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Today, we are covering the slightly easier and less conceptual topic of the trial balance. It is just a posting of balances from the ledger into it. We will…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

29 September 2020

22 August 2022

25 August 2022

30 August 2022

13 November 2022

8 January 2023

27 September 2025