Question No 78 Chapter 1 – UNIMAX Class 12 Part 2 – 2021

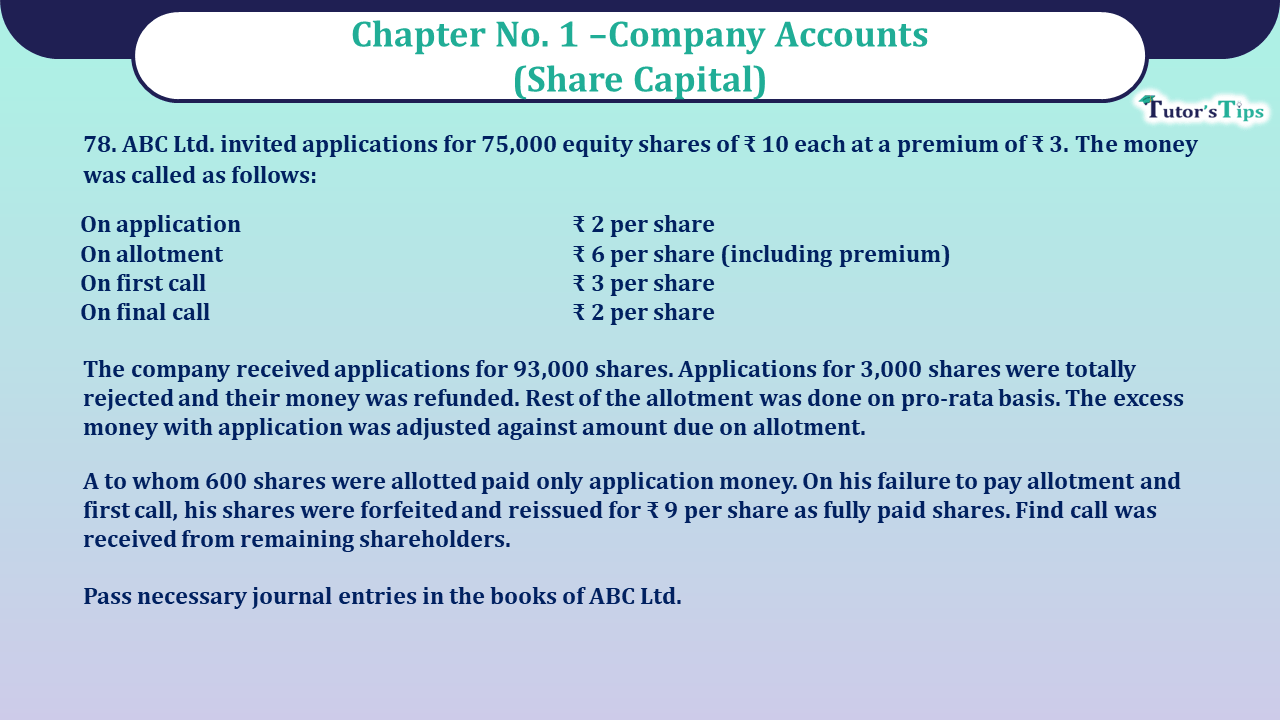

ABC Ltd. invited applications for 75,000 equity shares of ₹ 10 each at a premium of ₹ 3. The money was called as follows:

| On application | ₹ 2 per share |

| On allotment | ₹ 6 per share |

| On first | ₹ 3 per share |

| On final call | ₹ 2 per share |

The company received applications for 93,000 shares. Applications for 3,000 shares were totally rejected and their money was refunded. Rest of the allotment was done on pro-rata basis. The excess money with application was adjusted against amount due on allotment.

A to whom 600 shares were allotted paid only application money. On his failure to pay allotment and first call, his shares were forfeited and reissued for ₹ 9 per share as fully paid shares. Find call was received from remaining shareholders.

Pass necessary journal entries in the books of ABC Ltd.

The solution of Question 78 Chapter 1 of +2 Part-2: –

Journal

| Date | Particulars |

L.F. | Debit | Credit | |

| Bank A/c | Dr. | 1,86,000 | |||

| To Equity share application A/c | 1,86,000 | ||||

| (Being application money received on 93000 shares @ ₹ 2 each) | |||||

| Equity shares application A/c | Dr. | 1,86,000 | |||

| To Equity shares capital A/c | 1,50,000 | ||||

| To Equity share allotment A/c | 30,000 | ||||

| To Bank A/c | 6,000 | ||||

| (Being application money transferred to share capital a/c and share allotment & balance amount on 3000 shares refunded) | |||||

| Equity share allotment A/c | Dr. | 4,50,000 | |||

| To Equity shares capital A/c | 2,25,000 | ||||

| To Securities premium reserve A/c | 2,25,000 | ||||

| (Being allotment money due on 75,000 share @ ₹ 6 per share including 3 premium) | |||||

| Bank A/c | Dr. | 4,16,640 | |||

| To Equity share allotment A/c | 4,16,640 | ||||

| (Being received on allotment money) | |||||

| Equity share 1st call A/c | Dr. | 2,25,000 | |||

| To Equity shares capital A/c | 2,25,000 | ||||

| (Being first call money due on 75,000 shares @ ₹ 3 per shares) | |||||

| Bank A/c | Dr. | 2,23,200 | |||

| To Equity shares 1st call A/c | 2,23,200 | ||||

| (Being first call money received on 74400 shares @ ₹ 3 per share) | |||||

| Equity share capital A/c | Dr. | 4800 | |||

| Securities premium A/c | Dr. | 1800 | |||

| To Equity share allotment A/c | 3360 | ||||

| To Equity first call A/c | 1800 | ||||

| To Share forfeited A/c | 1440 | ||||

| (Being 600 shares of shareholder A forfeited due to non-payment of allotment and first call money) | |||||

| Equity share second & final call A/c | Dr. | 1,48,800 | |||

| To Equity shares capital A/c | 1,48,800 | ||||

| (Being second & final call money due on 74400 shares @ ₹ 2 per share) | |||||

| Bank A/c | Dr. | 1,48,800 | |||

| To Equity share second call A/c | 1,48,800 | ||||

| (Being second & final call money received on74400 shares @ ₹ 2 per share) | |||||

| Bank A/c | Dr. | 5400 | |||

| Share forfeited A/c | Dr. | 600 | |||

| To Equity share capital A/c | 6000 | ||||

| (Being 600 forfeited shares reissued @ ₹ 9 per share as fully paid up) | |||||

| Share forfeited A/c | Dr. | 840 | |||

| To capital reserve A/c | 840 | ||||

| (Being profit on 600 forfeited transferred to capital reserve A/c) | |||||

Working Note:

| Shares applied | Shares allotted | |

| Lot 1 | 90,000 | 75,000 |

| Lot 2 | 3,000 | Nil |

| 93,000 | 75,000 |

1 Table showing adjustment of excess amount received on application.

| Lot 1 | Lot 2 | total | |

| No. of shares applied | 90,000 | 3,000 | 93,000 |

| Less: no. of shares allotted | 7500 | Nil | 75,000 |

| Over subscription | 15,000 | 3000 | 18,000 |

| ₹ | ₹ | ₹ | |

| Excess amount received on application | 30,000 | 6,000 | 36,000 |

| Less: amount adjusted on allotment | 30,000 | Nil | 30,000 |

| Refunded to be made | Nil | 6000 | 6000 |

2 Net Amount received on allotment

| No. of share allotted to Mr. A shareholder =600 share | |

| No. of shares applied by Mr. A shareholder = 600*9000/75000 | 720share |

| ₹ | |

| Application money received 720 shares = 720*2 | 1440 |

| Less: actual application amount on 600 shares = 600*2 | 1200 |

| 240 | |

| ₹ | |

| Allotment amount due Mr. It on 600 shares 600*6 | 3600 |

| Less: Excess application money adjusted | 240 |

| Amount not paid by Mr. A | 3360 |

| Total amount due on allotment 75000*6 | 4,50,000 |

| Less: application money already adjusted | 30,000 |

| 420000 | |

| Less: amount not paid by Mr. A | 3360 |

| Net amount received on allotment | 416640 |

4 Calculation of amount to be transferred to Capital Reserve

| ₹ | ||

| Amount forfeited on 600 shares held by A | 1440 | |

| Less: Discount on allowed on reissued shares | 600 | |

| Balance credited to capital reserve a/c | 840 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

Share Capital: Meaning, Types, and Classes

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication