Question No 38 Chapter No 5

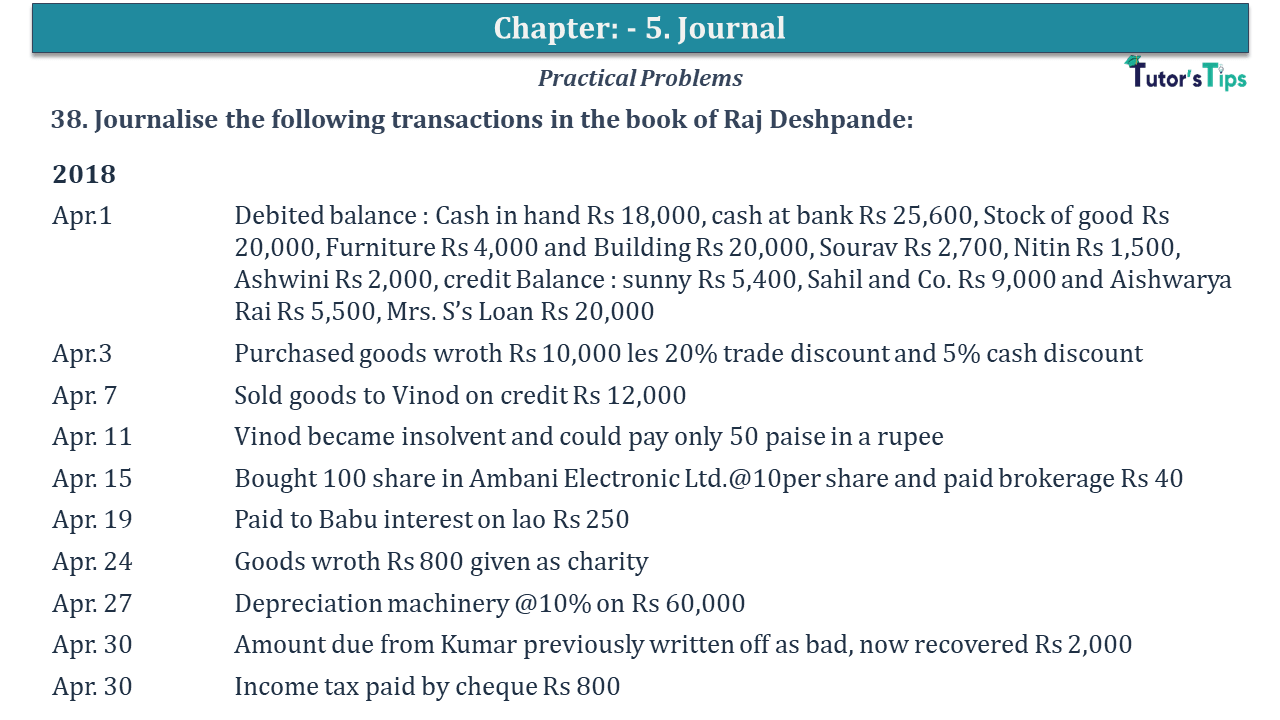

38. Journalise the following transactions in the book of Raj Deshpande:

| 2018 | |

| Apr.1 | Debited balance : Cash in hand Rs 18,000, cash at bank Rs 25,600, Stock of good Rs 20,000, Furniture Rs 4,000 and Building Rs 20,000, Sourav Rs 2,700, Nitin Rs 1,500, Ashwini Rs 2,000, credit Balance : sunny Rs 5,400, Sahil and Co. Rs 9,000 and Aishwarya Rai Rs 5,500, Mrs S’s Loan Rs 20,000 |

| Apr.3 | Purchased goods worth Rs 10,000 less 20% trade discount and 5% cash discount |

| Apr. 7 | Sold goods to Vinod on credit Rs 12,000 |

| Apr. 11 | Vinod became insolvent and could pay only 50 paise in a rupee |

| Apr. 15 | Bought 100 shares in Ambani Electronic Ltd.@10per share and paid brokerage Rs 40 |

| Apr. 19 | Paid to Babu interest on Laon Rs 250 |

| Apr. 24 | Goods worth Rs 800 given as charity |

| Apr. 27 | Depreciation machinery @10% on Rs 60,000 |

| Apr. 30 | Amount due from Kumar previously written off as bad, now recovered Rs 2,000 |

| Apr. 30 | Income tax paid by cheque Rs 800 |

The solution of Question No 38 Chapter No 5: –

| In the Books of Raj Deshpande | |||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2018 | |||||

| Apr. 1 | Cash A/c | Dr. | 18,000 | ||

| Bank A/c | Dr. | 25,600 | |||

| Stock A/c | Dr. | 20,000 | |||

| Furniture A/c | Dr. | 4,000 | |||

| Building A/c | Dr. | 20,000 | |||

| Sourav A/c | Dr. | 2,700 | |||

| Nitin A/c | Dr. | 1,500 | |||

| Ashwani A/c | Dr. | 2,000 | |||

| To Sunny A/c | 5,400 | ||||

| To Sahil and co. A/c | 9,000 | ||||

| To Ashwarya pillani A/c | 5,500 | ||||

| ToMrs S’s Loan A/c | 20,000 | ||||

|

To loan A/c To capital A/c |

53,900 | ||||

| (Being opening entry passed with assets and liabilities ) | |||||

| Apr. 3 | Purchases A/c | Dr. | 8,000 | ||

| To Cash A/c | 7,600 | ||||

| To Discount A/c | 400 | ||||

| (Being purchases goods from Kamal Chaudhary) | |||||

| Apr. 7 | Vinod A/c | Dr. | 12,000 | ||

| To Sale A/c | 12,000 | ||||

| (Being sold on credit ) | |||||

| Apr. 11 | Cash A/c | Dr. | 3,500 | ||

| Bad debts A/c | Dr, | 3,500 | |||

| To Vinod A/c | 7,000 | ||||

| (Being Receipts of 50% of the amount due & remaining treated as bad) | |||||

| Apr. 15 | Investment A/c | Dr. | 12,000 | ||

| To Cash A/c | 12,000 | ||||

| (Being purchased 800 share @ Rs10 each & brokerage paid ) | |||||

| Apr. 19 | Interest on loan A/c | Dr. | 250 | ||

| To CashA/c | 250 | ||||

| (Being interest on the loan paid in cash ) | |||||

| Apr. 24 | Charity A/c | Dr. | 800 | ||

| To Purchases A/c | 800 | ||||

| (Being goods distributed as a charity ) | |||||

| Apr. 27 | Depreciation A/c | Dr. | 6,000 | ||

| To Machinery A/c | 6,000 | ||||

| (Being Depreciation @10%on Machinery provided ) | |||||

| Apr. 30 | Cash A/c | Dr. | 4,400 | ||

| To Bad Debts Recovered A/c | 4,400 | ||||

| (Being Bad debts recovered from Kumar) | |||||

| Apr. 30 | Drawing A/c | Dr. | 800 | ||

| To Bank A/c | 800 | ||||

| (Being Income tax paid by cheque ) | |||||

How to make Journal Entries in Accounting – Explanation

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)