Question No 35 Chapter No 17

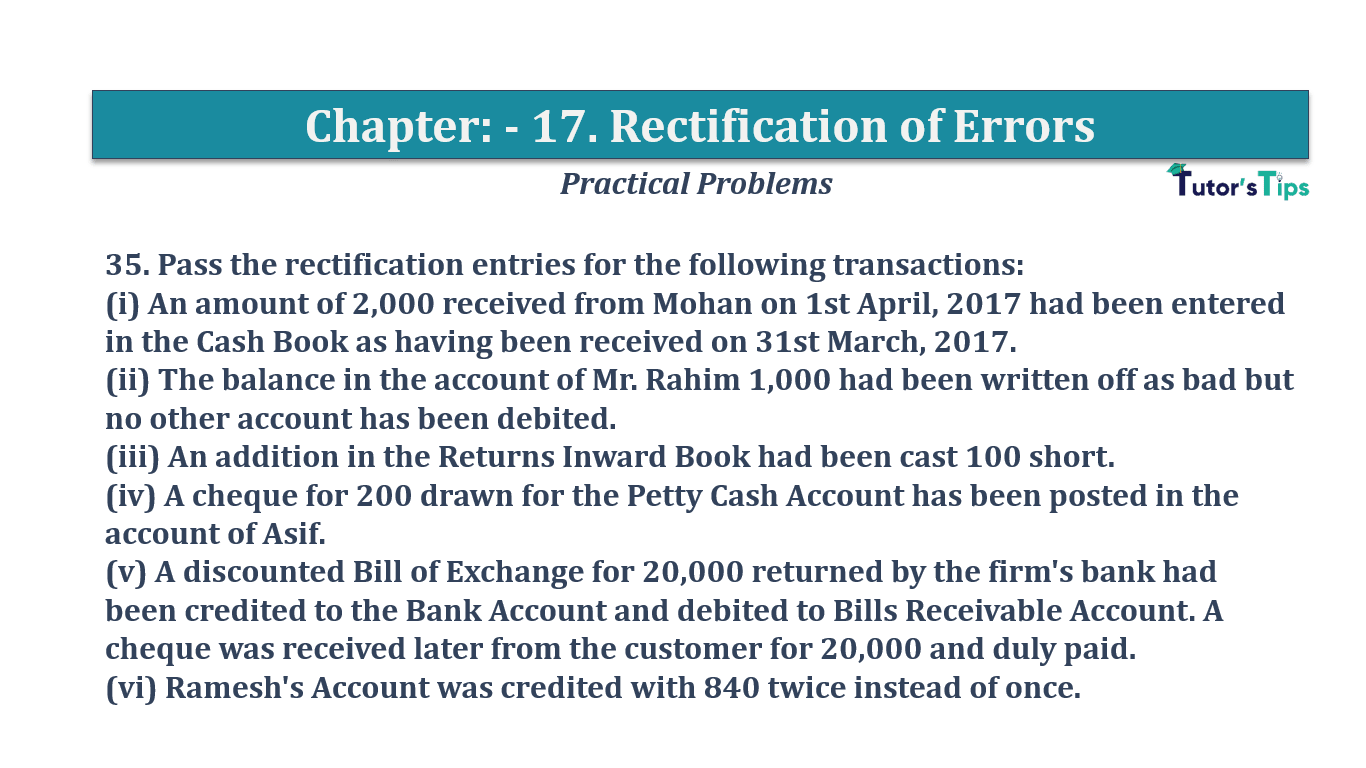

35. Pass the rectification entries for the following transactions:

(i) An amount of 2,000 received from Mohan on 1st April, 2017 had been entered in the Cash Book as having been received on 31st March, 2017.

(ii) The balance in the account of Mr. Rahim 1,000 had been written off as bad but no other account has been debited.

(iii) An addition in the Returns Inward Book had been cast 100 short.

(iv) A cheque for 200 drawn for the Petty Cash Account has been posted in the account of Asif.

(v) A discounted Bill of Exchange for 20,000 returned by the firm’s bank had been credited to the Bank Account and debited to Bills Receivable Account. A cheque was received later from the customer for 20,000 and duly paid. (vi) Ramesh’s Account was credited with 840 twice instead of once.

The solution of Question No 35 Chapter No 16:-

| Date | Particulars |

L.F. | Debit | Credit | |

| i | Mohan | Dr. | 2,000 | ||

| To Cash A/c | 2,000 | ||||

| (Being Cash received from Mohan on April 01,2017 but was wrongly passed on March 31, 2017) | |||||

| Note: On April 01,2017 in Cash Book Mohan’s Account is debited) | |||||

| ii | Bad Debts A/c | Dr. | 1,000 | ||

| To Suspense A/c | 1,000 | ||||

| (Being Bad Debt of Rahim was not posted to Bad Debts Account, now rectified) | |||||

| iii | Return Inwards A/c | Dr. | 100 | ||

| To Suspense A/c | 100 | ||||

| (Being Return Inwards Book was undercast, now rectified) | |||||

| iv | Petty Cash A/c | Dr. | 200 | ||

| To Asif | 200 | ||||

| (Being Cheque Drawn for Petty Cash was wrongly debited to Asif’s Account, now rectified) | |||||

| v | Customer’s A/c | Dr. | 20,000 | ||

| To Bills Receivable A/c | 20,000 | ||||

| (Being A discounted bill dishonored wrongly debited to Bills Receivable A/c, now rectified) | |||||

| vi | Ramesh | Dr. | 840 | ||

| To Suspense A/c | 840 | ||||

| (Being Ramesh’s Account was Credited twice, now rectified | |||||

Error Rectification in accounting – Explanation with examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

-

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping