Question No 29 Chapter No 18

Bad debts and provision

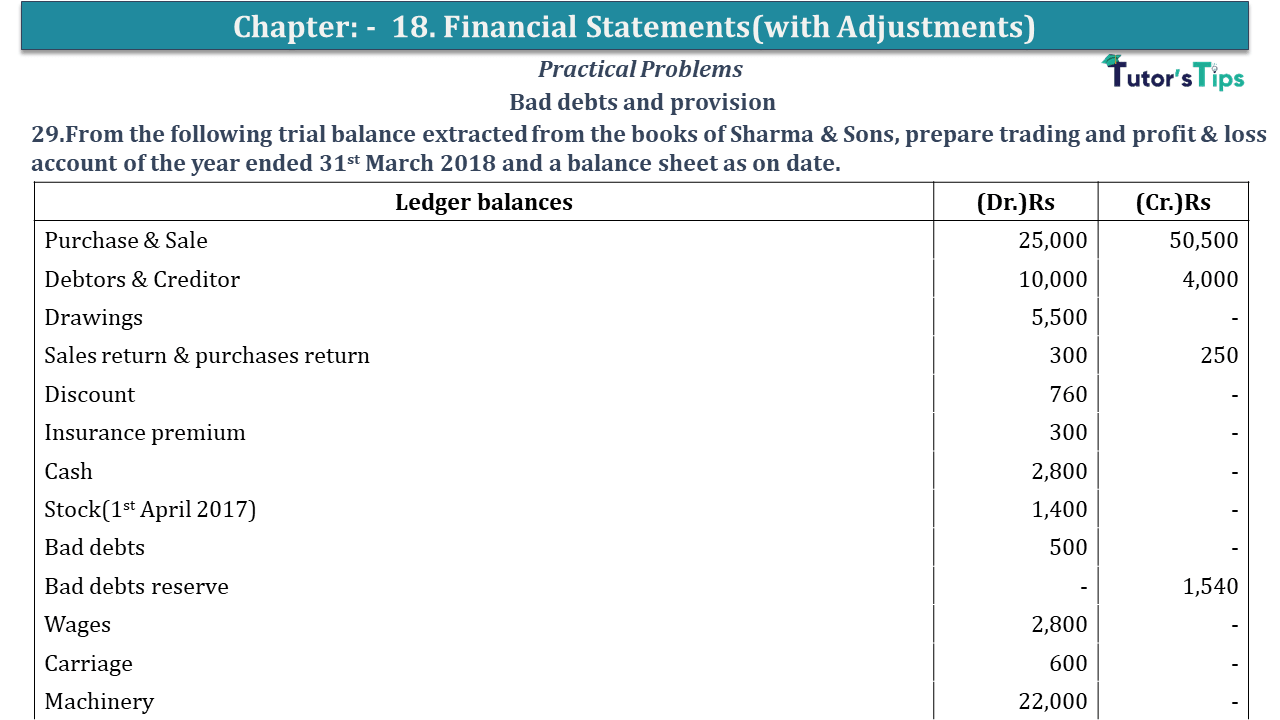

29.From the following trial balance extracted from the books of Sharma & Sons, prepare trading and profit & loss account of the year ended 31st March 2018 and a balance sheet as on date.

| Ledger balances | (Dr.)Rs | (Cr.)Rs |

| Purchase & Sale | 25,000 | 50,500 |

| Debtors & Creditor | 10,000 | 4,000 |

| Drawings | 5,500 | – |

| Sales return & purchases return | 300 | 250 |

| Discount | 760 | – |

| Insurance premium | 300 | – |

| Cash | 2,800 | – |

| Stock(1st April 2017) | 1,400 | – |

| Bad debts | 500 | – |

| Bad debts reserve | – | 1,540 |

| Wages | 2,800 | – |

| Carriage | 600 | – |

| Machinery | 22,000 | – |

| Furniture | 4,000 | – |

| Salaries | 3,000 | – |

| Bank charges | 500 | – |

| Bill receivable & bills payable | 5,500 | 5,000 |

| Trade expenses | 1,330 | – |

| Capital account | – | 29,000 |

| Building | 4,000 | – |

| 90,290 | 90,290 |

Adjustments:

- Depreciation building @5% and Machinery@10%

- Trade expenses of Rs 220 and wages of Rs 200 have not yet been paid

- Allow interest on capital at 10% p.a.

- Make provision for doubtful debts at 12%

- Stock on 31st March 2018 was Rs 10,000

- Prepaid insurance premium is Rs 50.

The solution of Question No 29 Chapter No 18:-

| Trading A/c |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Opening Stock A/c | 1,400 | By Sale A/c | 50,500 | ||

| To Purchases A/c | 25,000 | Less: Return | 300 | 50,200 | |

| Less: return | 250 | 24,750 | By Closing Stock | 10,000 | |

| To Wages A/c | 2,800 | ||||

| Add: outstanding wages | 200 | 3,000 | |||

| To Carriage A/c | 600 | ||||

| To Gross Profit A/c | 30,450 | ||||

| 60,200 | 60,200 | ||||

| Profit/Loss A/c |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Discount A/c | 760 | By Gross Profit A/c | 30,450 | ||

| By Insurance A/c | 300 | ||||

| Less: prepaid | 50 | 250 | |||

| By Trade Exp. A/c | 1,330 | ||||

| Add: outstanding | 220 | 1,550 | |||

| To Dep. On building | 160 | ||||

| To Dep. On Machinery | 200 | ||||

| To Provision for doubtful debts | |||||

| Bad debts | 500 | ||||

| Add: new provision | 1,200 | ||||

| Less: old Provision | 1,540 | 160 | |||

| To Interest on capital | 2,000 | ||||

| To Salaries | 3,000 | ||||

| To Bank changes | 500 | ||||

| To Net profit A/c | 18,930 | ||||

| 30,450 | 30,450 | ||||

| Balance Sheet | |||||

| Labilities |

Amount | Assets |

Amount | ||

| Capital A/c | 29,000 | Debtors | 10,000 | ||

| Add: Net Profit | 18,930 | Less: Provision for doubtful debts | 1,200 | 8,800 | |

| Add: Interest on capital | 2,900 | Cash in hand | 2,800 | ||

| Less: Drawing | 5,500 | 45,330 | Bill Receivable | 5,500 | |

| Creditor | 4,000 | Machinery | 22,000 | ||

| Bill payable | 5,000 | Less: depreciation | 2,200 | 19,800 | |

| Outstanding Trade exp. | 220 | Prepaid Insurance | 50 | ||

| Outstanding Wages | 200 | Furniture | 4,000 | ||

| Building | 4,000 | ||||

| Less: depreciation | 200 | 3,800 | |||

| Closing Stock | 10,000 | ||||

| 54,750 | 54,750 | ||||

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)