Question No 28 Chapter No 18

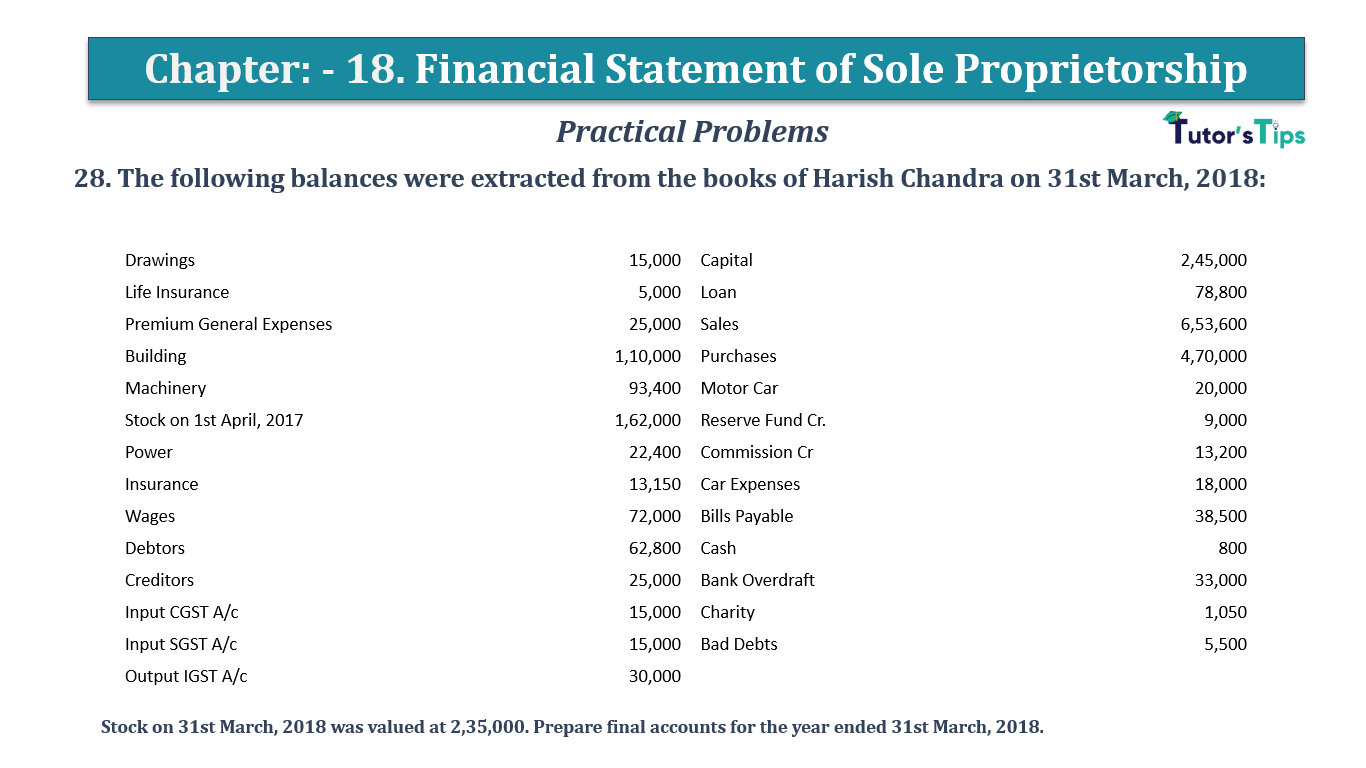

28. The following balances were extracted from the books of Harish Chandra on 31st March, 2018:

| Drawings | 15,000 | Capital | 2,45,000 |

| Life Insurance | 5,000 | Loan | 78,800 |

| Premium General Expenses | 25,000 | Sales | 6,53,600 |

| Building | 1,10,000 | Purchases | 4,70,000 |

| Machinery | 93,400 | Motor Car | 20,000 |

| Stock on 1st April, 2017 | 1,62,000 | Reserve Fund Cr. | 9,000 |

| Power | 22,400 | Commission Cr | 13,200 |

| Insurance | 13,150 | Car Expenses | 18,000 |

| Wages | 72,000 | Bills Payable | 38,500 |

| Debtors | 62,800 | Cash | 800 |

| Creditors | 25,000 | Bank Overdraft | 33,000 |

| Input CGST A/c | 15,000 | Charity | 1,050 |

| Input SGST A/c | 15,000 | Bad Debts | 5,500 |

| Output IGST A/c | 30,000 |

Stock on 31st March, 2018 was valued at 2,35,000. Prepare final accounts for the year ended 31st March, 2018.

The solution of Question No 28 Chapter No 18:-

| Trading Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Opening Stock | 1,62,000 | By Sales | 6,53,600 | ||

| To Purchases | 4,70,000 | By Closing Stock | 2,35,000 | ||

| To Power | 22,400 | ||||

| To Wages | 72,000 | ||||

| To Gross Profit | 1,62,200 | ||||

| 8,88,600 | 8,88,600 | ||||

| Profit and Loss Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To General Expenses | 25,000 | By Gross Profit | 1,62,200 | ||

| To Taxes and Insurance | 13,150 | By Commission | 13,200 | ||

| To Bad Debts | 5,500 | ||||

| To Car Expenses | 18,000 | ||||

| To Charity | 1,050 | ||||

| To Net Profit | 1,12,700 | ||||

| 1,75,400 | 1,75,400 | ||||

| Balance Sheet |

|||||

| Particular |

Amount | Particular |

Amount | ||

| Capital | 2,45,000 | Building | 1,10,000 | ||

| Add: Net Profit | 1,12,700 | Machinery | 93,400 | ||

| Less: Life Insurance Premium | 5, 000 | Motor Car | 20,000 | ||

| Less: Drawings | 15, 000 | 3,37,700 | Closing Stock | 2,35,000 | |

| Reserve Fund | 9,000 | Sundry Debtor | 62,800 | ||

| Loan | 78,800 | Cash | 800 | ||

| Bank Overdraft | 33,000 | ||||

| Bills Payable | 38,500 | ||||

| Creditors | 25,000 | ||||

| 5,22,000 | 5,22,000 | ||||

Working Note:

Output IGST-Input CGST-Input SGST= 30,000-15,000-15,000=Nil

GST Payable/Receivable=Nil

Hence, Computation of GST won’t affect the Balance Sheet.

Final Accounts: Meaning, Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

-

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping