Question No 21 Chapter No 7

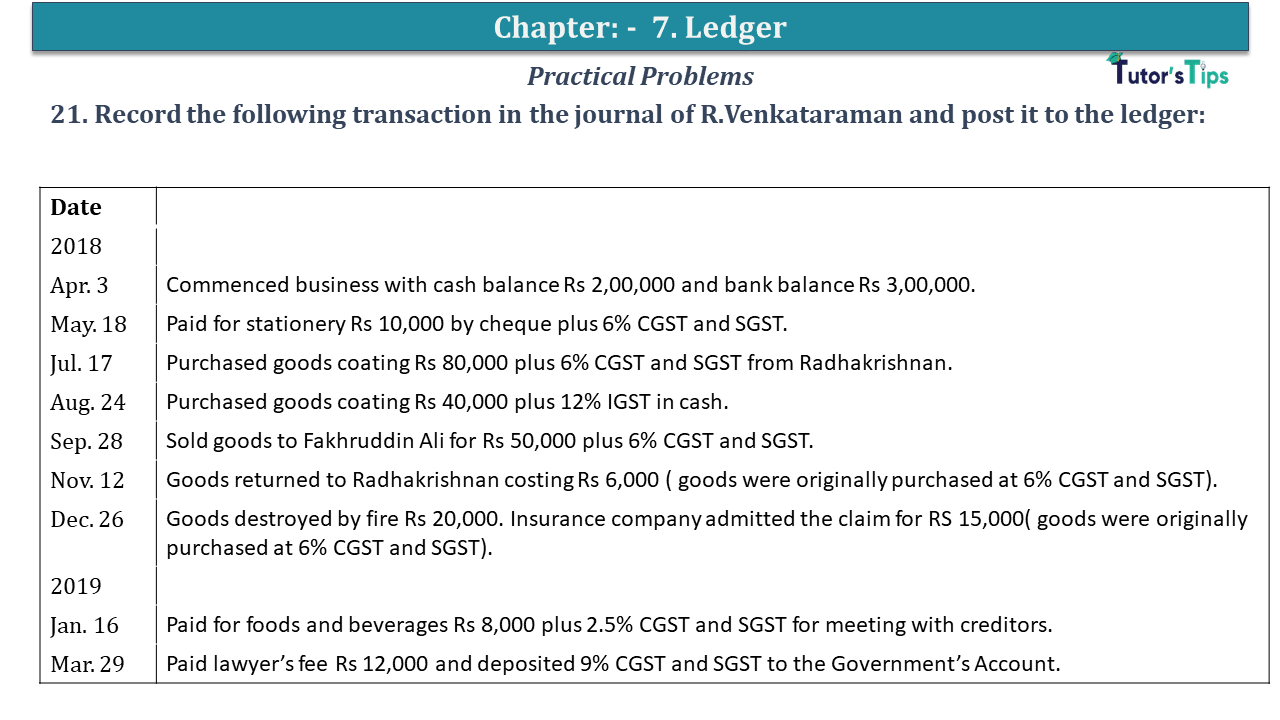

21. Record the following transaction in the journal of R.Venkataraman and post it to the ledger:

| Date | |

| 2018 | |

| Apr. 3 | Commenced business with cash balance Rs 2,00,000 and bank balance Rs 3,00,000. |

| May. 18 | Paid for stationery Rs 10,000 by cheque plus 6% CGST and SGST. |

| Jul. 17 | Purchased goods costing Rs 80,000 plus 6% CGST and SGST from Radhakrishnan. |

| Aug. 24 | Purchased goods costing Rs 40,000 plus 12% IGST in cash. |

| Sep. 28 | Sold goods to Fakhruddin Ali for Rs 50,000 plus 6% CGST and SGST. |

| Nov. 12 | Goods returned to Radhakrishnan costing Rs 6,000 ( goods were originally purchased at 6% CGST and SGST). |

| Dec. 26 | Goods destroyed by fire Rs 20,000. Insurance company admitted the claim for RS 15,000( goods were originally purchased at 6% CGST and SGST). |

| 2019 | |

| Jan. 16 | Paid for foods and beverages Rs 8,000 plus 2.5% CGST and SGST for meeting with creditors. |

| Mar. 29 | Paid lawyer’s fee Rs 12,000 and deposited 9% CGST and SGST to the Government’s Account. |

The solution of Question No 21 Chapter No 7: –

Journal

| Date | Particulars |

L.F. | Debit | Credit | |

| 2018 | |||||

| Apr.1 | Cash A/c | Dr. | 2,00,000 | ||

| Bank A/c | Dr. | 3,00,000 | |||

| To Capital A/c | 5,00,000 | ||||

| (Being business started with cash and bank) | |||||

| May. 18 | Stationery A/c | Dr. | 10,000 | ||

| Input CGST A/c | Dr. | 600 | |||

| Input SGST A/c | Dr. | 600 | |||

| To Bank A/c | 11,200 | ||||

| (Being bought stationery plus 6% CGST and SGST) | |||||

| Jul. 17 | Purchases A/c | Dr. | 80,000 | ||

| Input CGST A/c | Dr. | 4,800 | |||

| Input SGST A/c | Dr. | 4,800 | |||

| To Radhakrishnan A/c | 89,600 | ||||

| (Being bought goods plus 6% CGST and SGST) | |||||

| Aug. 24 | Purchases A/c | Dr. | 40,000 | ||

| Input IGST A/c | Dr. | 4,800 | |||

| To Cash A/c | 44,800 | ||||

| (Being bought goods plus 12% IGST) | |||||

| Sep.28 | Fakhruddin Ali A/c | Dr. | 56,000 | ||

| To Sale A/c | 50,000 | ||||

| To Output CGST A/c | 3,000 | ||||

| To Output SGST A/c | 3,000 | ||||

| (Being goods sold Fakhruddin Ali 6% CGST and SGST) | |||||

| Nov. 12 | Radhakrishnan A/c | Dr. | 6,720 | ||

| To Purchases return A/c | 6,000 | ||||

| To Input CGST A/c | 360 | ||||

| To Input SGST A/c | 360 | ||||

| (Being goods sold Fakhruddin Ali 6% CGST and SGST) | |||||

| Dec. 26 | Goods destroyed by Fire A/c | Dr. | 7,400 | ||

| Insurance Company A/c | Dr. | 15,000 | |||

| To Purchases A/c | 20,000 | ||||

| To Output CGST A/c | 1,200 | ||||

| To Output SGST A/c | 1,200 | ||||

| (Being goods sold Fakhruddin Ali 6% CGST and SGST) | |||||

| 2019 | |||||

| Jan. 16 | Referment A/c | Dr. | 8,000 | ||

| Input CGST A/c | Dr. | 200 | |||

| Input SGST A/c | Dr. | 200 | |||

| To Cash A/c | 8,400 | ||||

| (Being cash paid for food and beverages plus 2.5% CSGST and SGST) | |||||

| Mar. 29 | Lawyer’s fee A/c | Dr. | 9,000 | ||

| Input CGST A/c | Dr. | 1,080 | |||

| Input SGST A/c | Dr. | 1,080 | |||

| To Cash A/c | 11,160 | ||||

| (Being paid to lawyer’s fee and plus 9% CGST and SGST ) | |||||

| Dr. | Cash A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr. 1 | To Capital A/c | 2,00,000 | Aug. 24 | By Purchases A/c | 40,000 | ||

| Aug. 24 | By Input IGST A/c | 4,800 | |||||

| Jan. 16 | By Referment A/c | 8,000 | |||||

| Jan. 16 | By Input CGST A/c | 800 | |||||

| Jan. 16 | To Input SGST A/c | 800 | |||||

| 2019 | |||||||

| Mar. 29 | By Lawyer’s fee A/c | 9,000 | |||||

| Mar. 29 | By Input CGST A/c | 1,080 | |||||

| Mar. 29 | By Input SGST A/c | 1,080 | |||||

| Mar. 31 | By Balance c/d | 1,34,440 | |||||

| 2,00,000 | 2,00,000 | ||||||

| Dr. | Capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | |||||||

| Apr. 1 | By Cash A/c | 2,00,000 | |||||

| 2019 | Apr. 1 | By Bank A/c | 3,00,000 | ||||

| Mar. 31 | To Balance c/d | 5,00,000 | |||||

| 5,00,000 | 5,00,000 | ||||||

| Dr. | Purchases A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2019 | 2018 | ||||||

| Jan. 24 | To Radhakrishnan A/c | 80,000 | Dec. 26 | By Goods destroyed by Fire A/c | 5,000 | ||

| Dec. 26 | By Insurance Company A/c | 15,000 | |||||

| 2019 | |||||||

| Mar. 31 | By Balance c/d | 60,000 | |||||

| 80,000 | 80,000 | ||||||

| Dr. | Bank A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Apr.1 | To Capital A/c | 3,00,000 | May. 18 | By Stationery A/c | 10,000 | ||

| May. 18 | By Input CGST A/c | 600 | |||||

| May. 18 | By Input SGST A/c | 600 | |||||

| 2019 | |||||||

| Mar. 31 | By Balance c/d | 1,66,400 | |||||

| 3,00,000 | 3,00,000 | ||||||

| Dr. | Fakhruddin Ali A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Sep.28 | To Sale A/c | 50,000 | |||||

| Sep.28 | To Output CGST A/c | 3,000 | |||||

| Sep.28 | To Output SGST A/c | 3,000 | 2019 | ||||

| Mar. 31 | By Balance c/d | 56,000 | |||||

| 56,000 | 56,000 | ||||||

| Dr. | Radhakrishnan A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Nov. 12 | To Purchases return A/c | 6,000 | Jul. 17 | By Purchases A/c | 80,000 | ||

| Nov. 12 | To Input CGST A/c | 360 | Jul. 17 | By Input CGST A/c | 4,800 | ||

| Nov. 12 | To Input SGST A/c | 360 | Jul. 17 | By Input SGST A/c | 4,800 | ||

| 2019 | |||||||

| Mar. 31 | To Balance c/d | 82,880 | |||||

| 89,600 | 89,600 | ||||||

| Dr. | Referment A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan. 16 | To Cash A/c | 8,000 | |||||

| Mar. 31 | By Balance c/d | 8,000 | |||||

| 8,000 | 8,000 | ||||||

| Dr. | Lawyer’s fee A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Mar. 29 | To Cash A/c | 9,000 | |||||

| Mar. 31 | By Balance c/d | 9,000 | |||||

| 9,000 | 9,000 | ||||||

| Dr. | Stationery A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| May. 18 | To Bank A/c | 10,000 | |||||

| Mar. 31 | By Balance c/d | 10,000 | |||||

| 10,000 | 10,000 | ||||||

| Dr. | Input CGST A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| May. 18 | To Cash A/c | 600 | Nov. 12 | By Radhakrishnan A/c | 360 | ||

| Jul. 17 | To Radhakrishnan A/c | 4,800 | Dec. 26 | By Goods destroyed by Fire A/c | 1,200 | ||

| Nov. 12 | To Cash A/c | 200 | |||||

| Mar. 29 | To Cash A/c | 1,080 | |||||

| Mar. 31 | By Balance c/d | 5,120 | |||||

| 6,680 | 6,680 | ||||||

| Dr. | Input CGST A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| May. 18 | To Cash A/c | 600 | Nov. 12 | By Radhakrishnan A/c | 360 | ||

| Jul. 17 | To Radhakrishnan A/c | 4,800 | Dec. 26 | By Goods destroyed by Fire A/c | 1,200 | ||

| Nov. 12 | To Cash A/c | 200 | |||||

| Mar. 29 | To Cash A/c | 1,080 | |||||

| Mar. 31 | By Balance c/d | 5,120 | |||||

| 6,680 | 6,680 | ||||||

| Dr. | Output IGST A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Aug. 24 | By Cash A/c | 4,800 | |||||

| Mar. 31 | To Balance c/d | 4,800 | |||||

| 4,800 | 4,800 | ||||||

| Dr. | Sale A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Sept. 28 | By Fakhruddin Ali A/c | 50,000 | |||||

| Mar. 31 | To Balance c/d | 50,000 | |||||

| 50,000 | 50,000 | ||||||

What is Ledger in accounting – explain its Types

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)

Chapter No. 18 – Financial Statements – (With Adjustments)