Question No 19 Chapter No 17

Trading and Profit & Loss Account and Balance Sheet

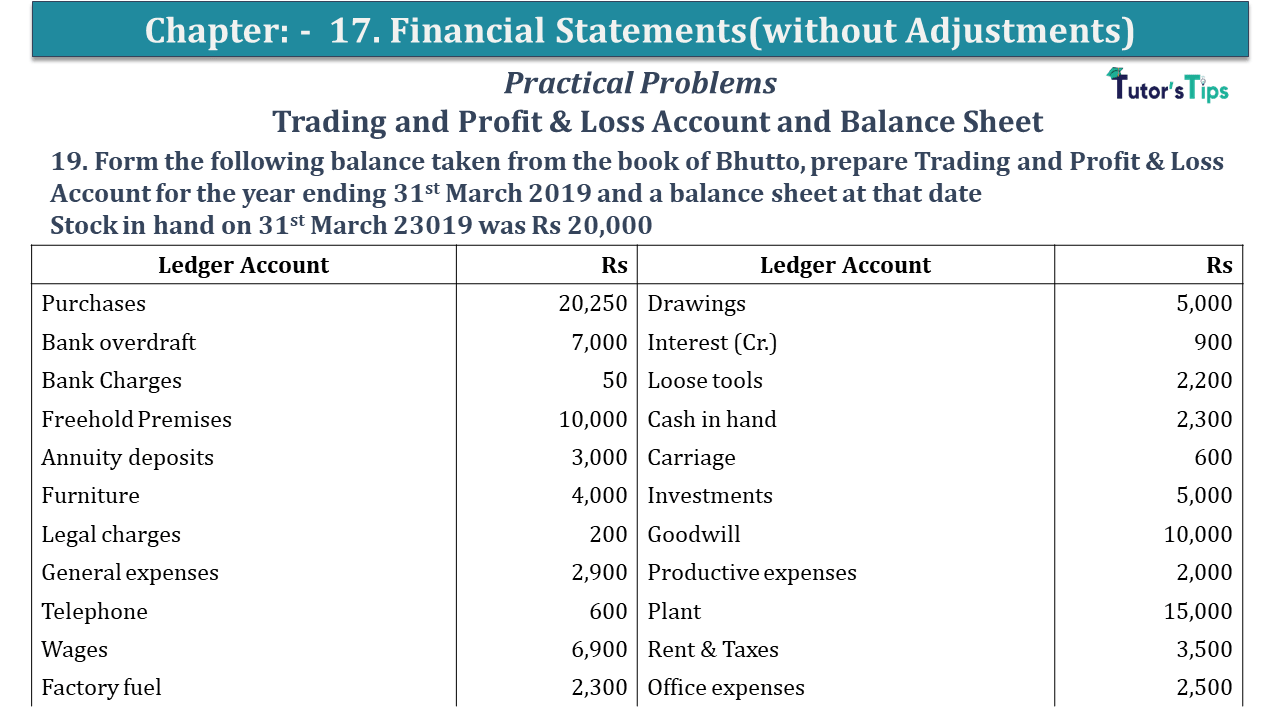

19. Form the following balance taken from the book of Bhutto, prepare Trading and Profit & Loss Account for the year ending 31st March 2019 and a balance sheet at that date

Stock in hand on 31st March 23019 was Rs 20,000

| Ledger Account | Rs | Ledger Account | Rs |

| Purchases | 20,250 | Drawings | 5,000 |

| Bank overdraft | 7,000 | Interest (Cr.) | 900 |

| Bank Charges | 50 | Loose tools | 2,200 |

| Freehold Premises | 10,000 | Cash in hand | 2,300 |

| Annuity deposits | 3,000 | Carriage | 600 |

| Furniture | 4,000 | Investments | 5,000 |

| Legal charges | 200 | Goodwill | 10,000 |

| General expenses | 2,900 | Productive expenses | 2,000 |

| Telephone | 600 | Plant | 15,000 |

| Wages | 6,900 | Rent & Taxes | 3,500 |

| Factory fuel | 2,300 | Office expenses | 2,500 |

| Creditor | 25,000 | Stock(1-4-2018) | 9,700 |

| Capital | 50000 | Debtors | 25,000 |

| Sales | 40,920 | Bills payable | 18,000 |

| Bill receivable | 5,320 | Loans to staff | 2,000 |

The solution of Question No 19 Chapter No 17:-

| Trading A/c |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Opening Stock A/c | 9,700 | By Sale A/c | 40,920 | ||

| To Purchases A/c | 20,250 | ||||

| To Wages A/c | 6,900 | By Closing Stock | 20,000 | ||

| To Factory Fuel A/c | 2,300 | ||||

| To Carriage A/c | 600 | ||||

| To Productive Expenses A/c | 2,000 | ||||

| To Gross Profit A/c | 19,170 | ||||

| 60,920 | 60,920 | ||||

| Profit/Loss A/c |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Bank Charges A/c | 50 | By Gross Profit A/c | 19,170 | ||

| To Legal Charges A/c | 200 | By Interest A/c | 900 | ||

| To Insurance A/c | 600 | ||||

| To General Expenses A/c | 2,900 | ||||

| To Telephone Charges A/c | 600 | ||||

| To Rent and Taxes A/c | 3,500 | ||||

| To Office expenses A/c | 2,500 | ||||

| To Net profit A/c | 9,720 | ||||

| 20,070 | 20,070 | ||||

| Balance Sheet | |||||

| Labilities |

Amount | Assets |

Amount | ||

| Capital A/c | 50,000 | Cash in hand | 2,300 | ||

| Add: Net Profit | 9,720 | Annuity Deposits | 3,000 | ||

| Less: Drawing | 5,000 | Bill receivable | 5,320 | ||

| Less: Insurance premium | 900 | 53,820 | Investments | 5,000 | |

| Bank Overdraft | 7,000 | S. Debtors | 25,000 | ||

| S. creditor | 25,000 | Closing Stock | 20,000 | ||

| Bill Payable | 18,000 | Loan to Staff | 2,000 | ||

| Freehold Premises | 10,000 | ||||

| Furniture | 4,000 | ||||

| Loose tolls | 2,200 | ||||

| Plant | 15,000 | ||||

| Goodwill | 10,000 | ||||

| 1,03,820 | 1,03,820 | ||||

Final Accounts: Definition and Explanation

Profit and Loss Account: Meaning, Format & Examples

Balance Sheet: Meaning, Format & Examples

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)