Question No 15 Chapter No 8

Record the following transactions in the Journal of Ashoka Furniture Traders, Ludhiana(Punjab):

| 2018 | Rs | |

| Apr 01 | Suresh paid into Bank as capital | 60,000 |

| Apr 02 | He bought goods for cheque | 24,000 |

| Apr 03 | Sold to Mukand & co., Delhi | 6,700 |

| Apr 04 | Sold goods for cash | 10,900 |

| Apr 05 | Paid Sundry Expenses in Cash | 3,000 |

| Apr 08 | Paid for office Furniture and fittings by cheque | 4,000 |

| Apr 09 | Bought goods from Ramesh and Bros., Faridabad(Haryana) | 10,600 |

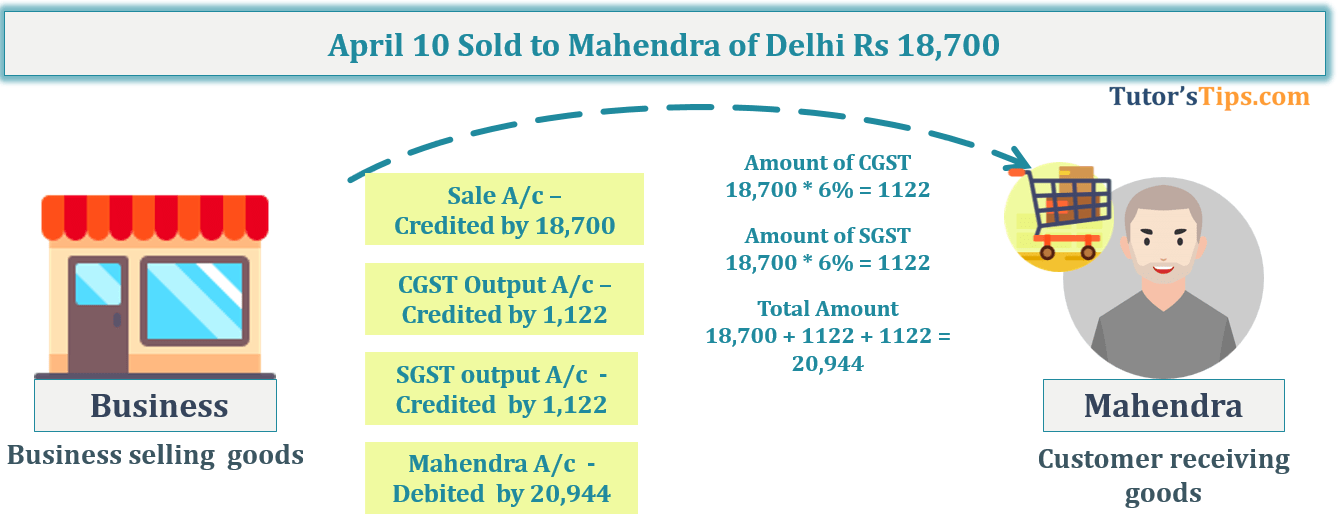

| Apr 10 | Sold to Mahendra of Delhi | 18,700 |

| Apr 11 | Returned goods to Ramesh & Bors. | 1,500 |

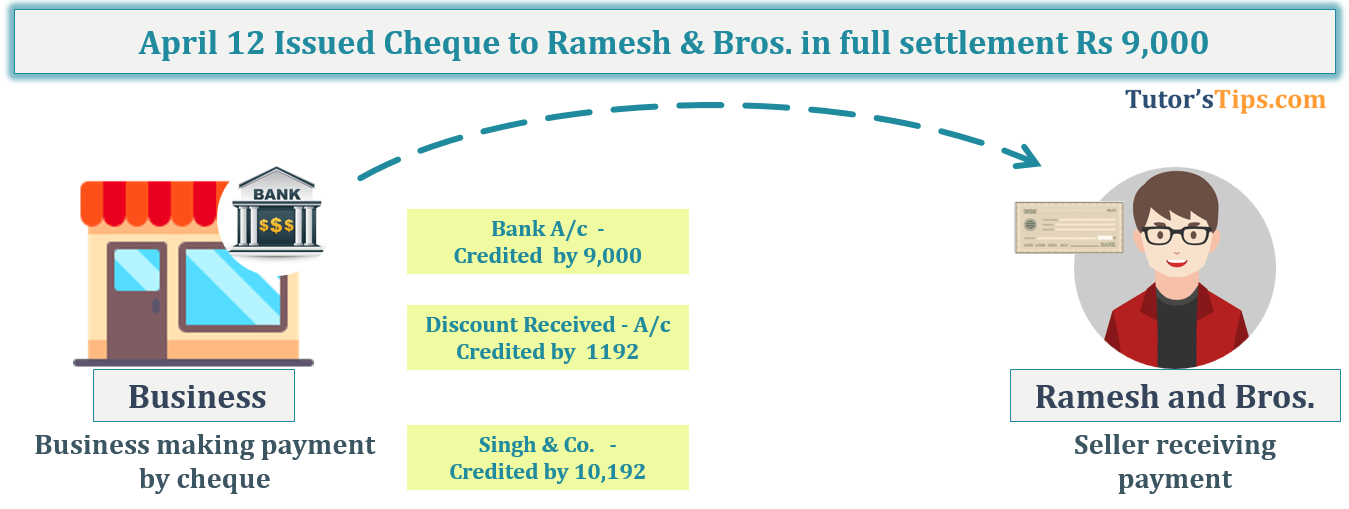

| Apr 12 | Issued Cheque to Ramesh & Bros. in full settlement | 9,000 |

| Apr 14 | Sold goods for cash | 4,900 |

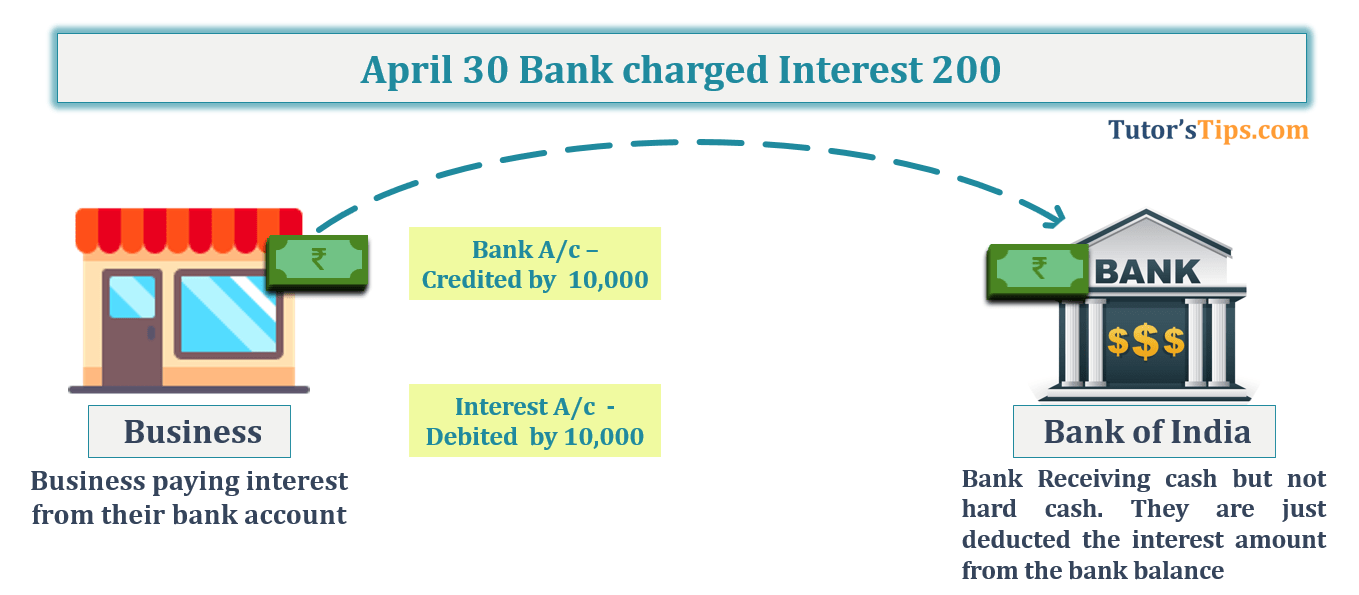

| Apr 30 | Bank charged Interest | 200 |

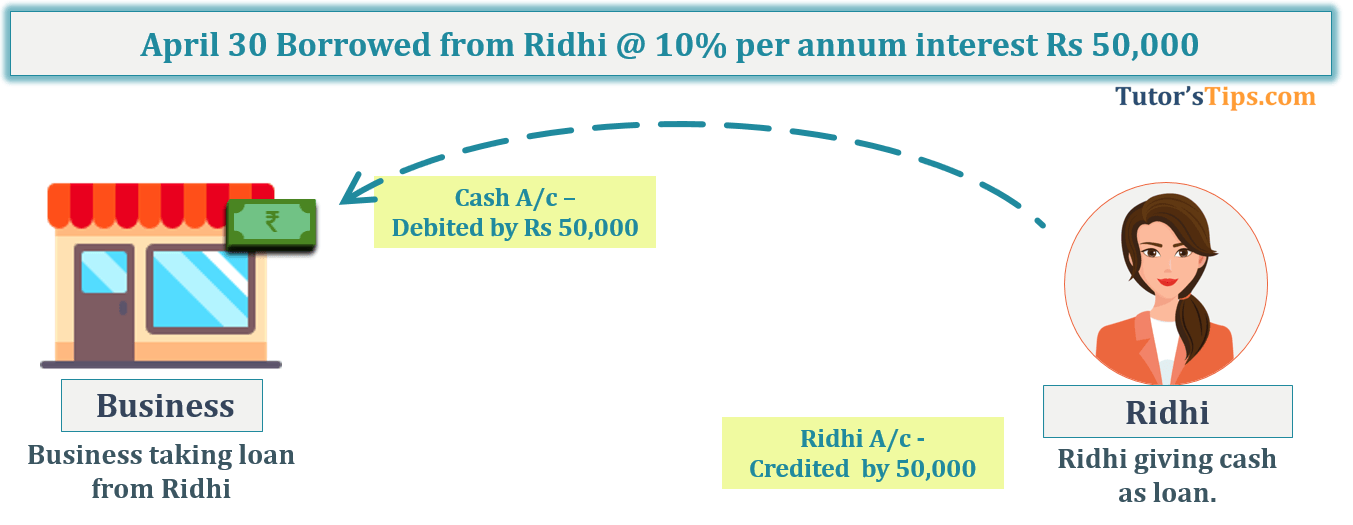

| Apr 30 | Borrowed from Ridhi @ 10% per annum interest | 50,000 |

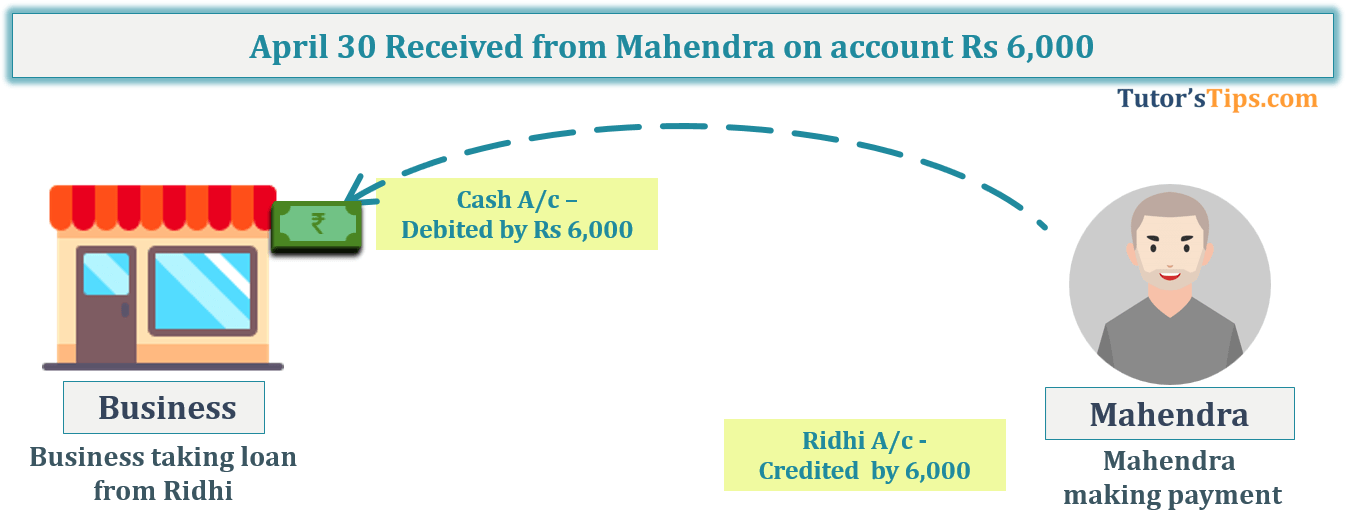

| Apr 30 | Received from Mahendra on account | 6,000 |

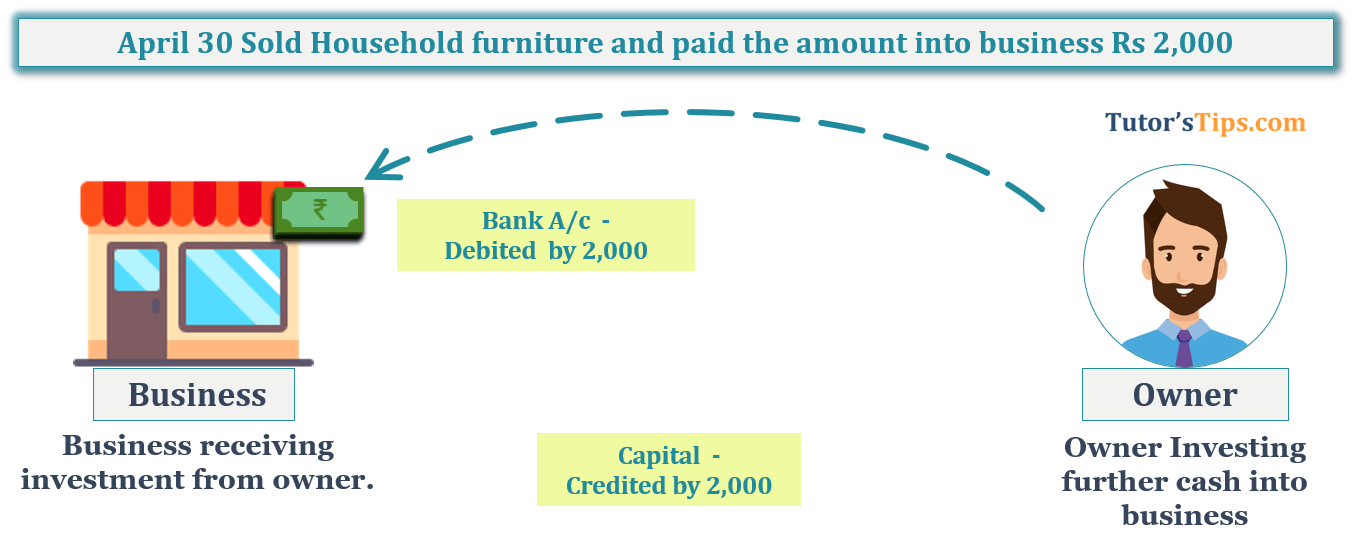

| Apr 30 | Sold Household furniture and paid the amount into business | 2,000 |

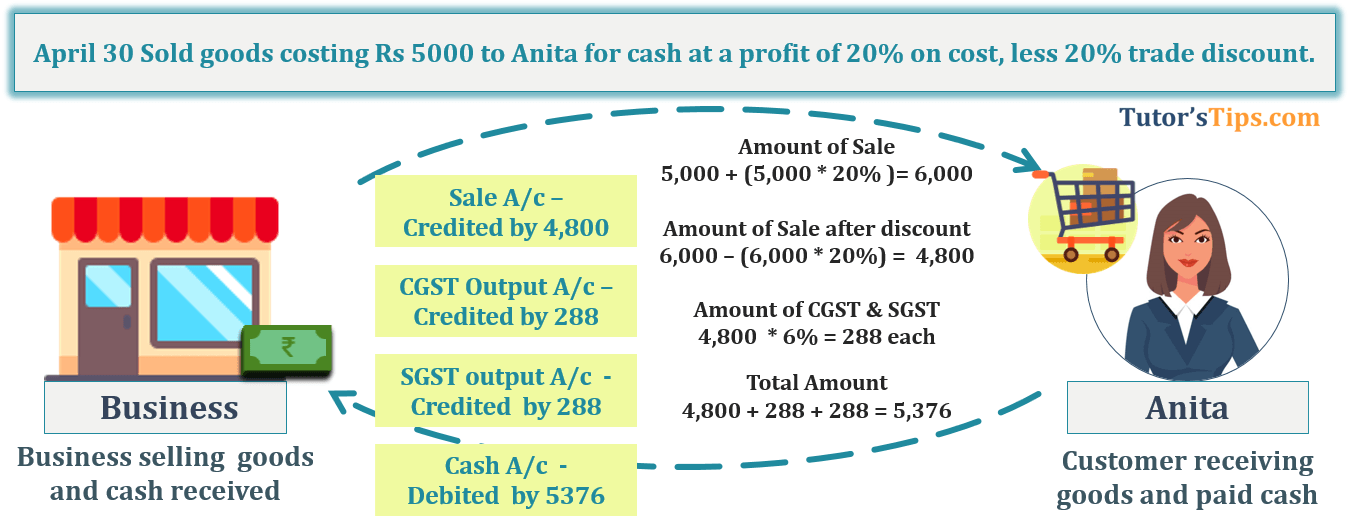

| Apr 30 | Sold goods costing Rs 5000 to Anita for cash at a profit of 20% on cost, less 20% trade discount. | |

| Apr 30 | Sold goods costing Rs 20,000 to Sunil at a profit of 20% on sale less 20% trade discount and paid cartage Rs 150(to be charged from customer) |

CGST and SGST @6% each on intra-state sale and purchase. IGST is lived @ 12% on inter-state sale and purchase.

Solution of Question No 15 Chapter No 8:

In the Books of Ashoka Furniture Trader, Ludhiana (Punjab)

| Date | Particulars |

L.F. | Debit | Credit | |

| April 1 | Bank A/c | Dr. | 60,000 | ||

| To Capital A/c | 60,000 | ||||

| (Being started business with opening a bank account) | |||||

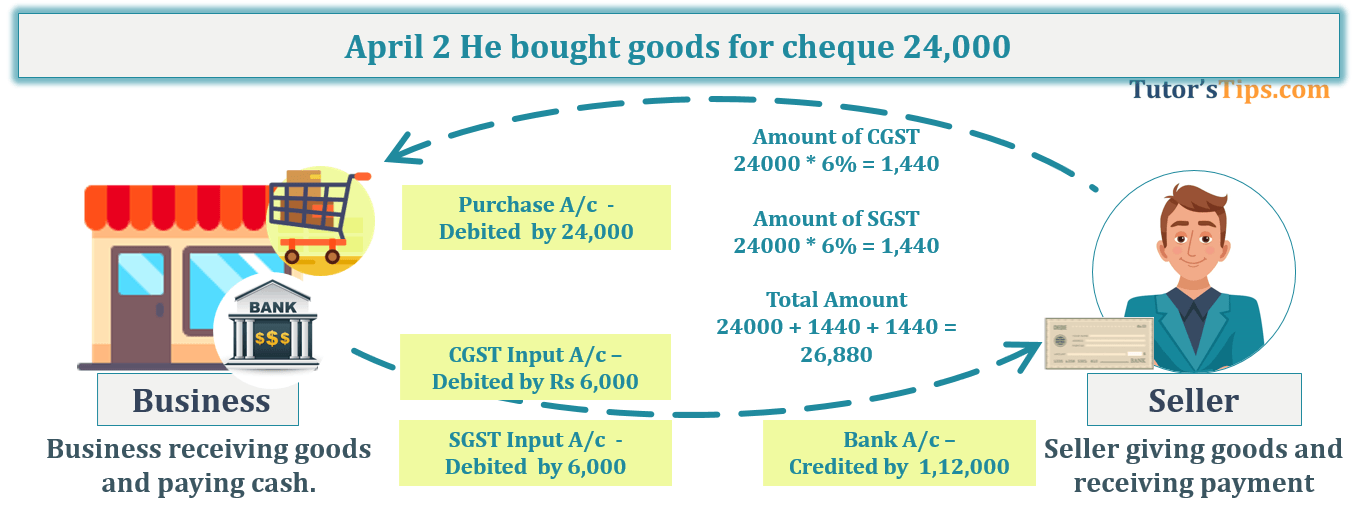

| April 2 | Purchase A/c | Dr. | 24,000 | ||

| CGST Input A/c | Dr. | 1,440 | |||

| SGST Input A/c | Dr. | 1,440 | |||

| To Bank A/c | 26,880 | ||||

| (Being goods purchased by cheque.) | |||||

| April 3 | Mukand & Co. A/c | Dr. | 7504 | ||

| To Sales A/c | 6,700 | ||||

| To CGST Output A/c | 402 | ||||

| To SGST Output A/c | 402 | ||||

| (Being goods sold to Mukand & Co.) | |||||

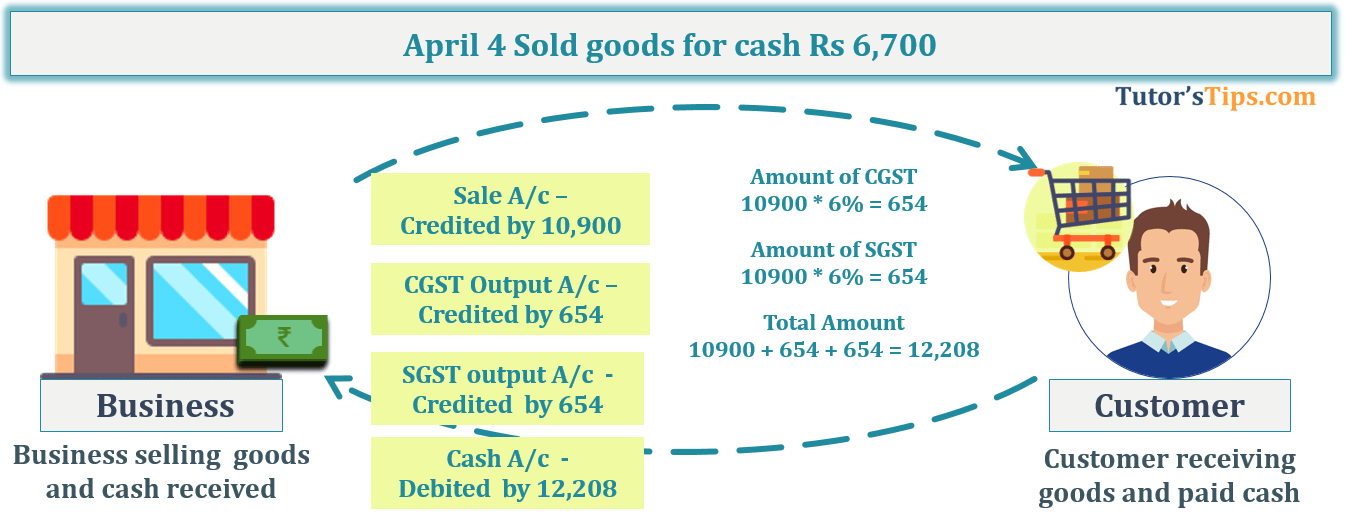

| April 3 | Cash A/c | Dr. | 12,208 | ||

| To Sales A/c | 10,900 | ||||

| To CGST Output A/c | 654 | ||||

| To SGST Output A/c | 654 | ||||

| (Being goods sold for cash) | |||||

| April 5 | Sundry Expenses A/c | Dr. | 3,000 | ||

| To Cash A/c | 3,000 | ||||

| (Being Sundry Expenses paid.) | |||||

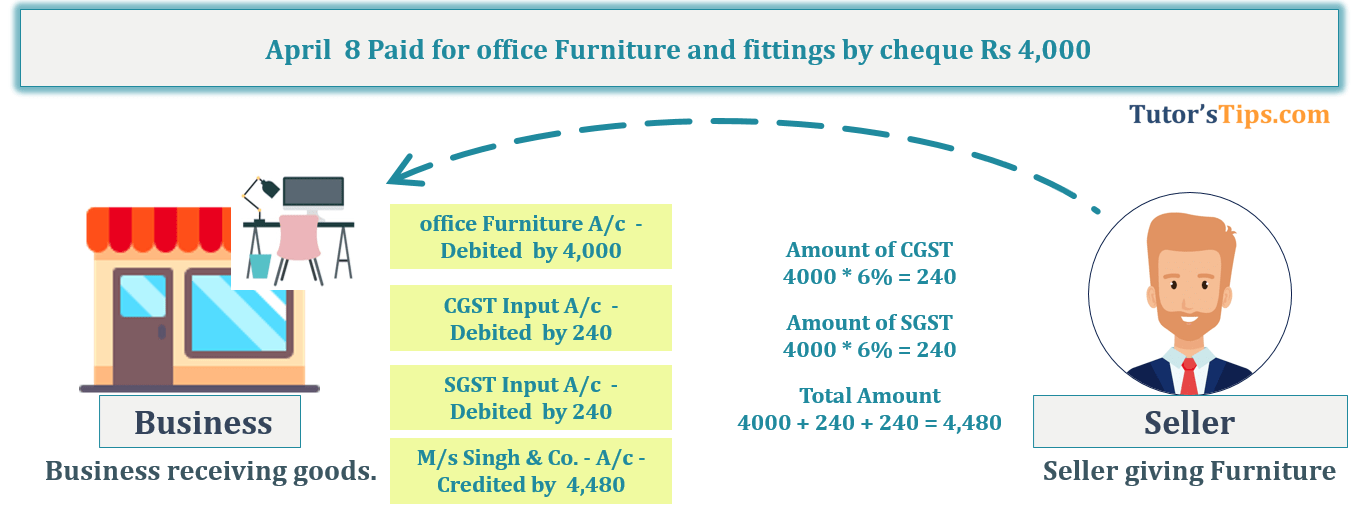

| April 8 | Office Furniture and Fitting A/c | Dr. | 4,000 | ||

| CGST Input A/c | Dr. | 240 | |||

| SGST Input A/c | Dr. | 240 | |||

| To Bank A/c | 4,480 | ||||

| (Being paid for office furniture and fitting) | |||||

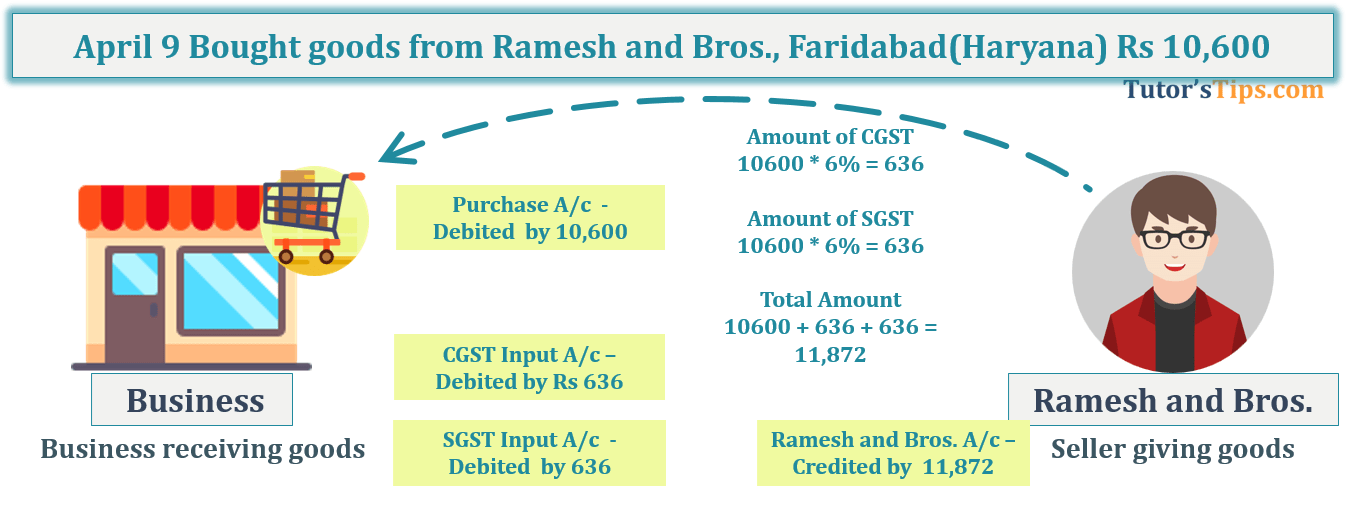

| April 9 | Purchase A/c | Dr. | 10,600 | ||

| IGST Input A/c | Dr. | 1,272 | |||

| To Ramesh and Bros., A/c | 11,872 | ||||

| (Being purchased goods from Ramesh and Bros., Faridabad) | |||||

| April 10 | Mahendra A/c | Dr. | 20,944 | ||

| To Sales A/c | 18,700 | ||||

| To CGST Output A/c | 1,122 | ||||

| To SGST Output A/c | 1,122 | ||||

| (Being goods sold to Mahendra ) | |||||

| April 11 | Ramesh and bros. A/c | Dr. | 1,680 | ||

| To Purchase Return A/c | 1,500 | ||||

| To IGST Output A/c | 180 | ||||

| (Being goods returned to Ramesh and bros ) | |||||

| April 11 | Ramesh and bros. A/c | Dr. | 10,192 | ||

| To Bank A/c | 9,000 | ||||

| To Discount Received A/c | 1,192 | ||||

| (Being goods returned to Ramesh and bros ) | |||||

| April 12 | Cash A/c | Dr. | 10,000 | ||

| Discount Allowed A/c | Dr. | 80 | |||

| To Rakesh A/c | 10,080 | ||||

| (Being paid to Ramesh and bros. by cheque and received discount ) | |||||

| April 14 | Cash A/c | Dr. | 5,488 | ||

| To Sales A/c | 4,900 | ||||

| To CGST Output A/c | 294 | ||||

| To SGST Output A/c | 294 | ||||

| (Being goods sold for cash) | |||||

| April 31 | Interest A/c | Dr. | 200 | ||

| To Bank A/c | 200 | ||||

| (Being bank charge interest.) | |||||

| April 30 | Cash A/c | Dr. | 50,000 | ||

| To Loan from Ridhi A/c | 50,000 | ||||

| (Being borrowed from Ridhi) | |||||

| April 30 | Cash A/c | Dr. | 6,000 | ||

| To MahendraA/c | 6,000 | ||||

| (Being payment received from Mahendra) | |||||

| April 30 | Cash A/c | Dr. | 2,000 | ||

| To Capital A/c | 2,000 | ||||

| (Being owner invested further capital.) | |||||

| April 30 | Cash A/c | Dr. | 5,376 | ||

| To Sales A/c | 4,800 | ||||

| To CGST Output A/c | 288 | ||||

| To SGST Output A/c | 288 | ||||

| (Being goods sold to Anita for cash) | |||||

| April 30 | Sunil A/c | Dr. | 22,550 | ||

| To Sales A/c | 20,000 | ||||

| To CGST Output A/c | 1,200 | ||||

| To SGST Output A/c | 1,200 | ||||

| To Cash A/c | 150 | ||||

| (Being goods sold to Sunil and cartage paid which charges from Sunil) | |||||

Explanation of All Transactions with images: –

This is not a part of the solution, So you don’t have to write it in the exam. So, why we explained if it is not needed. Because This explanation will help you to understand all transactions with logic and you don’t need to remember all the transactions but just understand and remember the logic use behind it.

Transaction No. 1

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Bank | Artificial Person | Personal Account | Bank receiving cash | Bank is receiver | Debit |

| Capital (Owner) | Personal | Personal Account | Depositing cash into business bank account | Owner is Giver | Credit |

Transaction No. 2

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Purchase (Goods) | Assets | Real Account | Goods received by business | Goods comes in | Debit |

| CGST Input A/c | Expenses | Nominal Account | Tax collected from buyer | All Expenses and losses | Debit |

| SGST Input A/c | Expenses | Nominal Account | Tax collected from buyer | All Expenses and losses | Debit |

| Bank A/c | A/ Person | Personal Account | Payment made with cheque | Bank is Giver | Credit |

Transaction No. 3

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Mukand & Co | A/Person | Personal Account | Goods received | He is receiver | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

Transaction No. 4

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash received by business | Cash Comes In | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

Transaction No. 5

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Sundry Expenses | Expense | Nominal Account | Expenses incurred | All Expenses and Losses | Debit |

| Cash | Assets | Real Account | Payment made in cash | Cash goes out | Credit |

Transaction No. 6

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Office Furniture | Assets | Real Account | furniture received | Furniture comes in | Debit |

| CGST Input A/c | Expenses | Nominal Account | Tax collected from buyer | All Expenses and losses | Debit |

| SGST Input A/c | Expenses | Nominal Account | Tax collected from buyer | All Expenses and losses | Debit |

| M/s Singh & Co. | A/Person | Personal Account | Goods given | They are Giver | Credit |

Transaction No. 7

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Purchase (Goods) | Assets | Real Account | Goods received by business | Goods comes in | Debit |

| CGST Input A/c | Expenses | Nominal Account | Tax collected from buyer | All Expenses and losses | Debit |

| SGST Input A/c | Expenses | Nominal Account | Tax collected from buyer | All Expenses and losses | Debit |

| Ramesh and Bros. | A/ Person | Personal Account | Giving goods ` | They are giver | Credit |

Transaction No. 8

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Mahendra | Person | Personal Account | Goods received | He is receiver | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

Transaction No. 9

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Purchase Returned (Goods) | Assets | Real Account | Goods returned by business | Goods goes out | Credit |

| CGST Input A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Input A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| Ramesh and Bros. | A/Person | Personal Account | Goods received | They are receiver | Debit |

Transaction No. 10

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Bank | A/Person | Personal Account | Bank issuing cheque | Bank is giver | Credit |

| Discount Received | gain | Nominal Account | Discount received | All income and gains | Credit |

| Ramesh and Bros. | A/Person | Personal Account | Goods received | They are receiver | Debit |

Transaction No. 11

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash received by business | Cash Comes In | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

Transaction No. 12

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash giving by business | Cash goes out | Credit |

| Bank | Personal | Personal Account | Receiving cash from business | Bank is Receiver | Debit |

Transaction No. 13

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash received by business | Cash Comes In | Debit |

| Ridhi | Person | Personal Account | Making payment to business | She is giver | Credit |

Transaction No. 14

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash received by business | Cash Comes In | Debit |

| Mahendra | Person | Personal Account | Making payment to business | he is giver | Credit |

Transaction No. 15

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash received by business | Cash Comes In | Debit |

| Capital (Owner) | Personal | Personal Account | Depositing cash into business bank account | Owner is Giver | Credit |

Transaction No. 16

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Cash | Assets | Real Account | Cash received by business | Cash Comes In | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

Transaction No. 17

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

| Sunil | Person | Personal Account | Goods received | He is receiver | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| Cash | Assets | Real Account | Cash giving by business | Cash goes out | Credit |

Thanks Please share with your friends

Comment if you have any question.

Check out T.S. Grewal +1 Book 2019 @ Amazon.in

T.S. Grewal’s Double Entry Book Keeping