Question No 15 Chapter No 11

Correcting an Incorrect Trial Balance

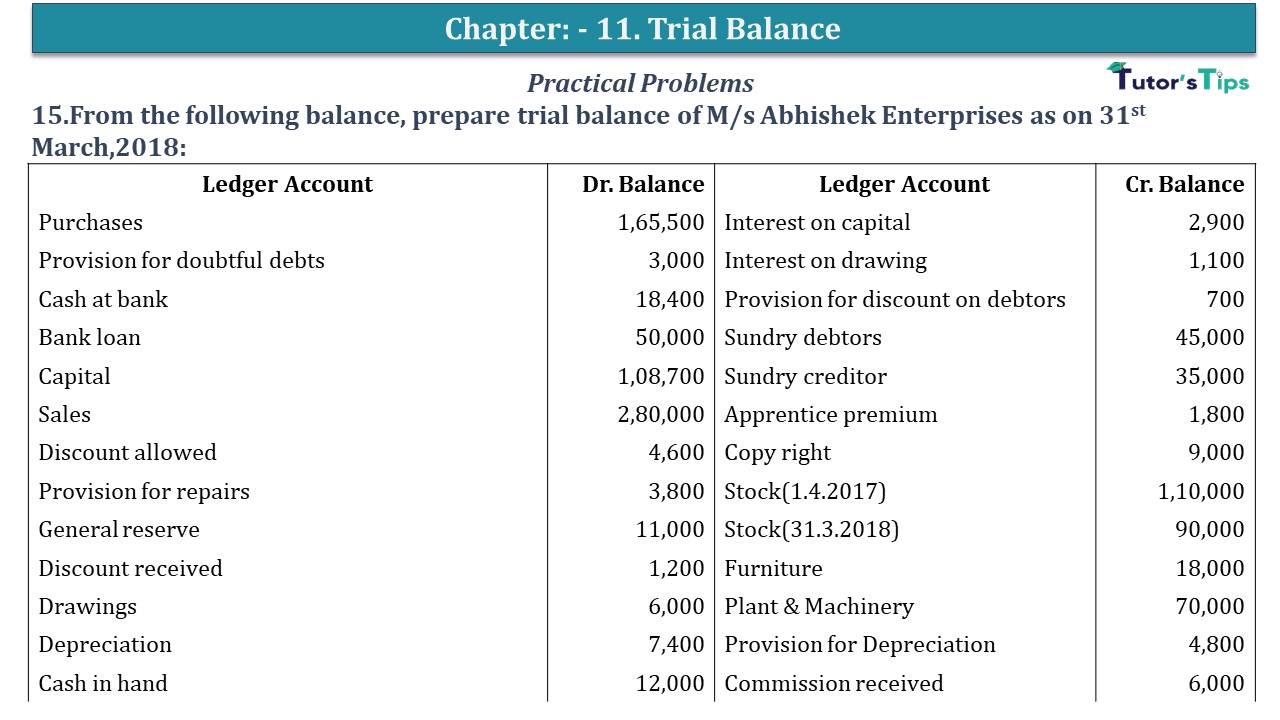

15. From the following balance, prepare a trial balance of M/s Abhishek Enterprises as on 31st March 2018:

| Ledger Account | Dr. Balance | Ledger Account | Cr. Balance |

| Purchases | 1,65,500 | Interest on capital | 2,900 |

| Provision for doubtful debts | 3,000 | Interest on drawing | 1,100 |

| Cash at bank | 18,400 | Provision for discount on debtors | 700 |

| Bank loan | 50,000 | Sundry debtors | 45,000 |

| Capital | 1,08,700 | Sundry creditor | 35,000 |

| Sales | 2,80,000 | Apprentice premium | 1,800 |

| Discount allowed | 4,600 | Copy right | 9,000 |

| Provision for repairs | 3,800 | Stock(1.4.2017) | 1,10,000 |

| General reserve | 11,000 | Stock(31.3.2018) | 90,000 |

| Discount received | 1,200 | Furniture | 18,000 |

| Drawings | 6,000 | Plant & Machinery | 70,000 |

| Depreciation | 7,400 | Provision for Depreciation | 4,800 |

| Cash in hand | 12,000 | Commission received | 6,000 |

| Rent paid | 1,500 | Commission accrued | 3,000 |

| Rent outstanding | 1,800 | Commission received in advance | 1,600 |

| Rent prepaid | 400 | Bills payable | 6,000 |

| Provident fund | 7,800 | Shares in Reliance Ltd. | 24,000 |

| Workmen compensation fund | 6,500 | Loss by fire | 3,500 |

| Purchases return | 1,600 | ||

| Salary | 12,400 | ||

| Interest on loan | 3,000 | ||

| Loan to Dhoni | 16,000 |

The solution of Question No. 15, Chapter No. 11: –

| Trail Balance A/c | |||

| Particulars |

J.F. | Debit | Credit |

| Purchases | 1,65,500 | ||

| Cash at the bank | 18,400 | ||

| Discount allowed | 4,600 | ||

| Drawings | 6,000 | ||

| Depreciation | 7,400 | ||

| Cash in hand | 12,000 | ||

| Rent paid | 1,500 | ||

| Rent prepaid | 400 | ||

| Salary | 12,400 | ||

| Interest on loan | 3,000 | ||

| Loan to Dhoni | 16,000 | ||

| Interest on capital | 2,900 | ||

| Sundry Debtors | 45,000 | ||

| Copy right | 9,000 | ||

| Opening stock | 1,10,000 | ||

| Furniture | 18,000 | ||

| Plant & Machinery | 70,000 | ||

| Commission Accrued | 3,000 | ||

| Shares in Reliance Ltd. | 24,000 | ||

| Loss by fire | 3,500 | ||

| Provision for Doubtful Debts | 3,000 | ||

| Bank loan | 50,000 | ||

| Capital | 1,08,700 | ||

| Sales | 2,80,000 | ||

| Provision for repairs | 3,800 | ||

| General Reserve | 11,000 | ||

| Discount received | 1,200 | ||

| Rent outstanding | 1,800 | ||

| Provident fund | 7,800 | ||

| Workmen compensation fund | 6,500 | ||

| Purchases return | 1,800 | ||

| Interest on Drawing | 1,100 | ||

| Provision for discount on Debtors | 700 | ||

| Sundry Creditor | 35,000 | ||

| Apprentice premium | 1,800 | ||

| Provision for depreciation | 4,800 | ||

| Commission received | 6,000 | ||

| Commission received in advance | 1,600 | ||

| Bills Payable | 6,000 | ||

| 5,32,600 | 5,32,600 | ||

Trial Balance | Explanation | Methods | Examples

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, check out the solved questions of all the Chapters: –

Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

Chapter No. 2 – Theory Base of Accounting

Chapter No. 3 – Origin of Transactions

Chapter No. 4 – Vouchers and transactions

Chapter No. 6 – Accounting for Goods and Services Tax(GST)

Chapter No. 9 – Other Subsidiary Books

Chapter No. 10 – Journal Proper

Chapter No. 11 – Trial Balance

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 14 – Provisions and Reserves

Chapter No. 15 – Bills of Exchange

Chapter No. 16 – Rectification of Errors

Chapter No. 17 – Financial Statements – (Without Adjustments)