Question 73 Chapter 5 – Unimax Class 12 Part 1 – 2021

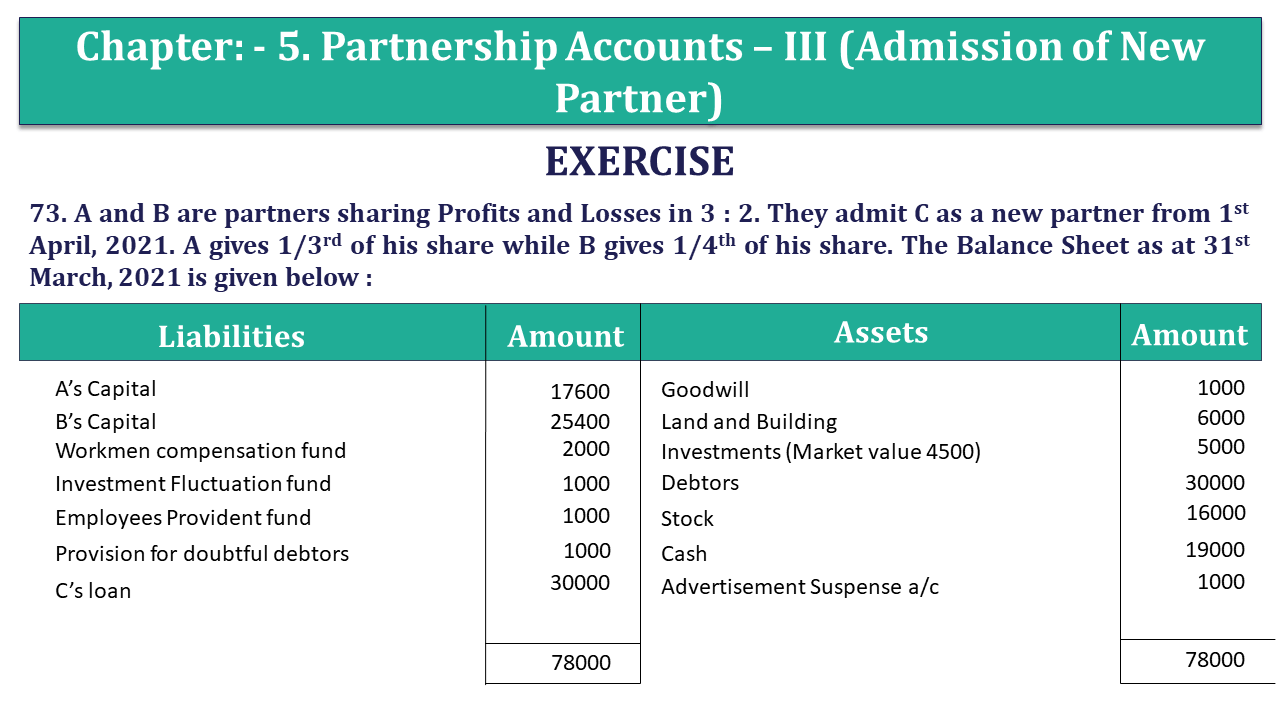

73. A and B are partners sharing Profits and Losses in 3 : 2. They admit C as a new partner from 1st April, 2021. A gives 1/3rd of his share while B gives 1/4th of his share. The Balance Sheet as at 31st March, 2021 is given below :

| Liabilities | Amount | Assets | Amount |

| A’s Capital | 17,600 | Goodwill | 1000 |

| B’s Capital | 25,400 | Land and Building | 6000 |

| Workmen compensation fund | 2,000 | Investments (Market value 4500) | 5000 |

| Investment Fluctuation fund | 1,000 | Debtors | 30000 |

| Employees Provident fund | 1,000 | Stock | 16000 |

| Provision for doubtful debtors | 1,000 | Cash | 19,000 |

| C’s loan | 30,000 | Advertisement Suspense a/c | 1000 |

| 78,000 | 78,000 |

Terms of C’s admission as follows :

- C’s loan will be converted into his capital. C brings in 60% of his share goodwill in cash.

- Goodwill is to be valued at 2 years’ purchase of Super Profits based on average profits of last three complete years. The profits were :

The normal profits are Rs. 60000. No goodwill is to appear in the books of firm. 40% of C’s share of goodwill be adjusted through a newly opened current account in his name.2018-2019 Rs. 45,000 2019-2020 Rs. 90,000 2020-2021 Rs. 13,5000 - Land and Building was found undervalued by Rs. 10000.

- Stock was found overvalued by Rs. 6000.

- Provision for doubtful debts is to be made equal to 5% of the debtors.

- Claim on account of workmen compensation is Rs. 1000.

- Capital accounts of partners be re-adjusted on the basis of their profit sharing ratio and any excess or deficiency be adjusted in cash. (C’s Capital should be taken as base.)

You are required to prepare Revaluation Account, Partner’s Capital Accounts and Balance Sheet.

The solution of Question 73 Chapter 5 – Unimax Class 12 Part 1: –

Revaluation A/c

| Particulars | Rs. | Particulars | Rs. | ||

| To Stock a/c | 6000 | By Land and Building a/c | 10,000 | ||

| To Provision for bad debts a/c | 500 | ||||

| To Profit on revaluation | |||||

| A (3 : 2) | 2100 | ||||

| B | 1400 | 3500 | |||

| 10,000 | 10,000 |

Capital Accounts

| Particulars | A | B | C | Particulars | A | B | C |

| To goodwill a/c | 600 | 400 | 1,635 | By Balance b/d | 17600 | 25400 | – |

| To advertisement suspense a/c | 600 | 400 | 1,635 | By Workers comp. | 600 | 400 | – |

| To Balance c/d | 40000 | 30000 | 30000 | By Profit on rev. | 2100 | 1400 | – |

| To Cash a/c | – | 2600 | – | By Cash a/c | 8600 | – | – |

| By Invt. Fluctuation fund a/c | 300 | 200 | – | ||||

| By C’s loan | – | – | 30000 | ||||

| By Premium a/c (10800) (60%) | 7200 | 3600 | – | ||||

| By C’s Current a/c (7200) (40%) | 4800 | 2400 | – | ||||

| 41200 | 33400 | 30000 | 41200 | 33400 | 30000 |

Balance Sheet

| Liabilities | Rs. | Assets | Rs. | |

| Workers comp. fund Investment | 1000 | Land and Building | 16000 | |

| Capital Accounts | Debtors | 30000 | ||

| A | 40000 | Stock | 10000 | |

| B | 30000 | Cash (19000 + 8600 + 10800 – 2600) | 35800 | |

| C | 30000 | 100000 | Investments | 4500 |

| Provision for bad debts (1000 + 500) | 1500 | C’s current a/c | 7200 | |

| Employees Provident fund | 1000 | |||

| 1,03,500 | 1,03,500 |

Working Note:

(A) Calculation of new PSR :

A’s new share = 3/5 – (1/3 X 3/5) = 3/5 – 1/5 = 2/5

Old Share – Sacrifice

B’s new share = 2/5 – (1/4 X 2/5) = 2/5 – 1/10 = 3/10

C’s share = 1/5 + 1/10 = 3/10

New PSR = 4 : 3 : 3

(B) Sacrificing Ratio :

A’s sacrifice = 1/3 X 3/5 = 3/15

B’s sacrifice = 1/4 X 2/5 = 1/10

S.R. = 2 : 1

(C) Calculation of Goodwill :

Average Profits = (45000 + 90000 + 135000)/3

Super Profits = Average profits – Normal profits

= 90000 – 60000 = Rs. 30000

Total goodwill of firm = 30000 X 2 = Rs. 60000

C’s share = 3/10 X 60000 = Rs. 18000

(D) Calculation of Capitals :

Total capital of firm = 30000 X 10/3 = Rs. 100000

A’s req. capital = 4/10 X 100000 = Rs. 40000

B’s req. capital = 3/10 X 100000 = Rs. 30000

What is Partnership – Meaning and Its 4 Types

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication