Question 70 Chapter 4 of +2-B

Table of Contents

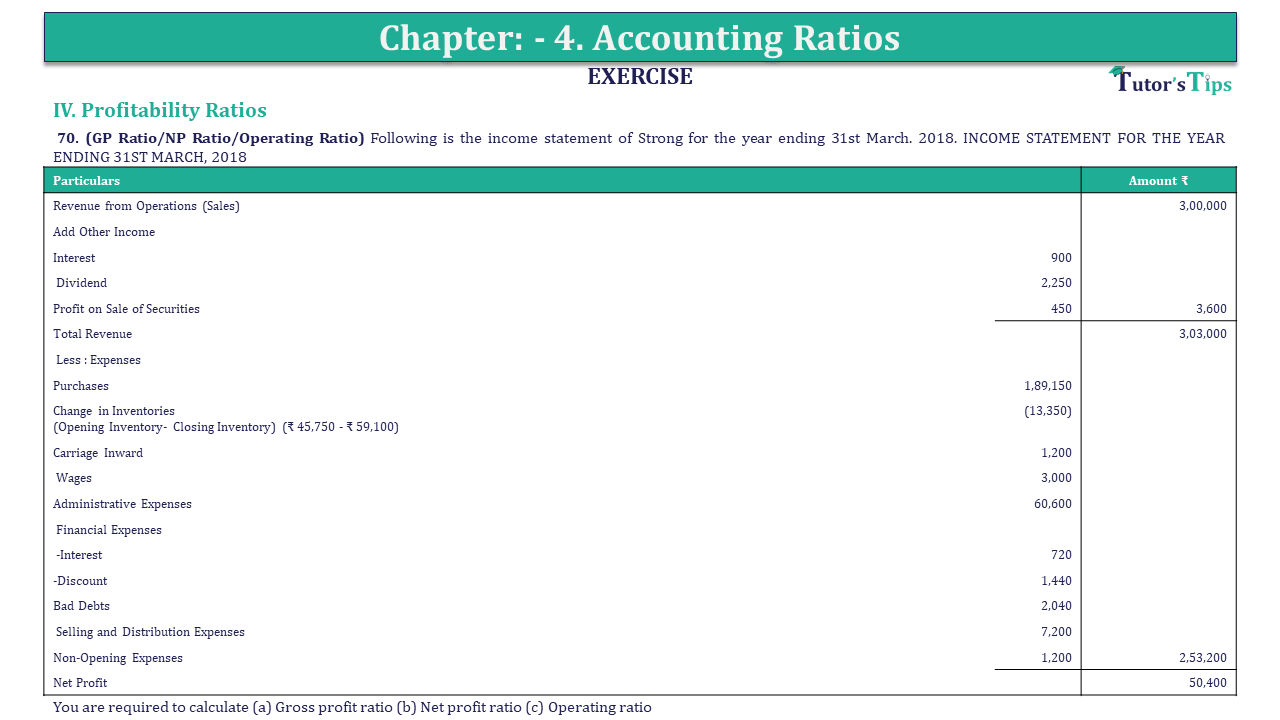

IV. Profitability Ratios

70. (GP Ratio/NP Ratio/Operating Ratio) Following is the income statement of Strong for the year ending 31st March. 2018. INCOME STATEMENT FOR THE YEAR ENDING 31ST MARCH, 2018

| Particulars | Amount ₹ | |

| Revenue from Operations (Sales) | 3,00,000 | |

| Add Other Income | ||

| Interest | 900 | |

| Dividend | 2,250 | |

| Profit on Sale of Securities | 450 | 3,600 |

| Total Revenue | 3,03,000 | |

| Less : Expenses | ||

| Purchases | 1,89,150 | |

| Change in Inventories | -13,350 | |

| (Opening Inventory- Closing Inventory) (₹ 45,750 – ₹ 59,100) | ||

| Carriage Inward | 1,200 | |

| Wages | 3,000 | |

| Administrative Expenses | 60,600 | |

| Financial Expenses | ||

| -Interest | 720 | |

| -Discount | 1,440 | |

| Bad Debts | 2,040 | |

| Selling and Distribution Expenses | 7,200 | |

| Non-Opening Expenses | 1,200 | 2,53,200 |

| Net Profit | 50,400 |

You are required to calculate (a) Gross profit ratio (b) Net profit ratio (c) Operating ratio

The solution of Question 70 Chapter 4 of +2-B: –

| (1) Gross Profit Ratio | = | ₹ 1,20,000 | X | ₹ 2,00,000 |

| ₹ 3,00,000 | ||||

| = | 40% |

| (2) Net Profit Ratio | = | ₹ 50,400 | X | 8,00,000 |

| ₹ 3,00,000 | ||||

| = | 16.8% |

| (c) Operating Ratio | = | Operating Cost* | X | 100 |

| Net sales | ||||

| = | ₹ 2,50,000 | X | 100 | |

| ₹ 3,00,000 | ||||

| = | 84% |

| Cost of goods sold | = | Opening Inventory – Closing Inventory + Purchase + Carriage Inwards + Wages |

| = | ₹ 45,750 – ₹ 59,100+ ₹ 1,89,150 + ₹ 1,200 + ₹ 3,000 | |

| = | ₹ 1,80,000 | |

| Gross Profit | = | Sales – Cost of goods sold |

| = | ₹ 3,00,000 – ₹ 1,80,000 | |

| = | ₹ 1,20,000 | |

| Operating Cost | = | Cost of goods sold + Operating Expenses |

| = | ₹ 1,80,000 + ₹ 72,000 | |

| = | ₹ 2,52,000 |

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication