Question 62 Chapter 5 – Unimax Class 12 Part 1 – 2021

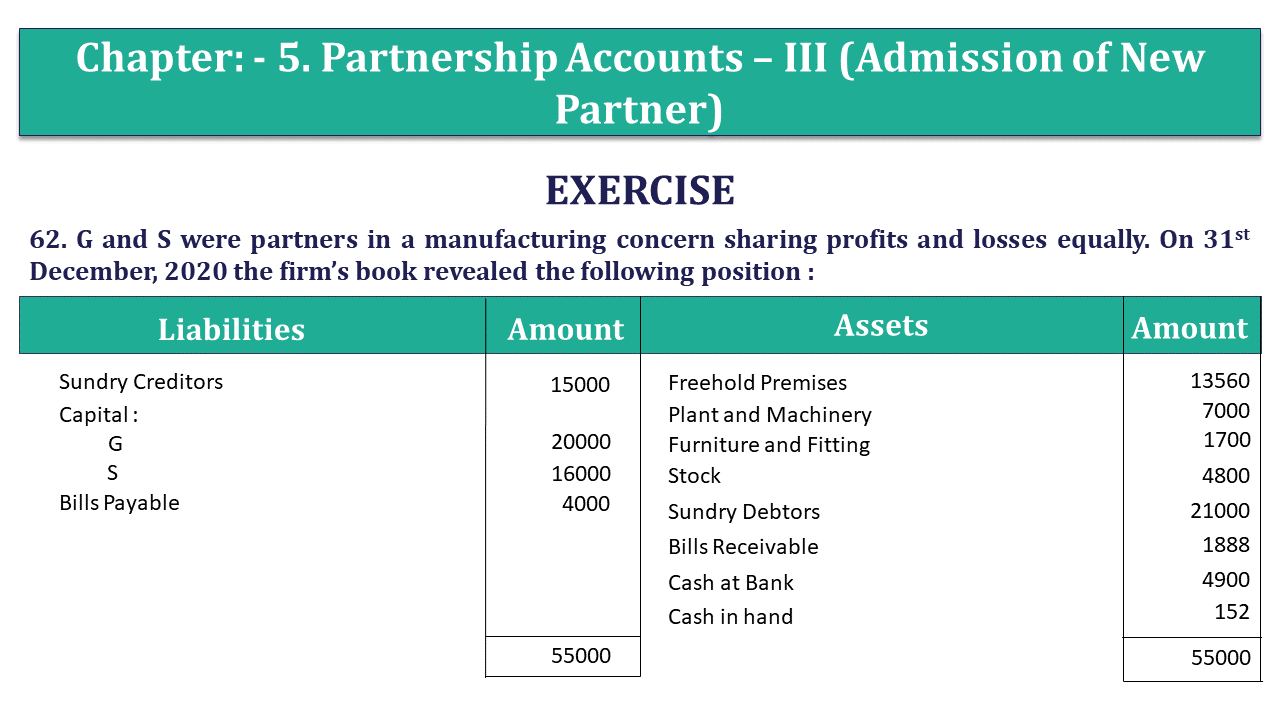

62. G and S were partners in a manufacturing concern sharing profits and losses equally. On 31st December, 2020 the firm’s book revealed the following position :

| Liabilities | Amount | Assets | Amount |

| Sundry Creditors | 15,000 | Freehold Premises | 13,560 |

| Capital : | Plant and Machinery | 7,000 | |

| G | 20,000 | Furniture and Fitting | 1,700 |

| S | 16,000 | Stock | 4,800 |

| Bills Payable | 4,000 | Sundry Debtors | 21,000 |

| Bills Receivable | 1,888 | ||

| Cash at Bank | 4,900 | ||

| Cash in hand | 152 | ||

| 55,000 | 55,000 |

On 1st January, 2021 it was agreed to admit T into the partnership on the following terms :

That he should bring into business sundry debtors amounting to Rs. 2400 (less provision of 10% for bad debts), sundry creditors of Rs. 500 and also stock of his business at a valuation of Rs. 1500. His capital in the new business is to be Rs. 5000, the balance of which he pays in cash and in consideration there of, he receives 1/5th share of profits of the firm.

It was mutually agreed that the following adjustments should be made as regards the business of G and S.

Stocks to be reduced by Rs. 800 ; Plant and Machinery to be increased by Rs. 300 ; Furniture and Fittings to be completely written off. It was further agreed that after the above adjustments had been effected, S should bring in sufficient cash to make his capital equal to that of G.

From the above particulars, show the opening Balance Sheet of the new firm as on 1st January, 2021 and state in what proportion the future profits and losses are to be shared.

The solution of Question 62 Chapter 5 – Unimax Class 12 Part 1: –

Revaluation A/c

| Particulars | Rs. | Particulars | Rs. | |

| To Stock a/c | 800 | By Plant and Machinery a/c | 300 | |

| To Furniture and Fittings a/c | 1700 | By Loss on revaluation | ||

| G ( 1 : 1 ) | 1100 | |||

| S | 1100 | 2200 | ||

| 2500 | 2500 |

Capital Accounts

| Particulars | G | S | T | Particulars | G | S | T |

| To Loss on revaluation | 1,100 | 1,100 | – | By Balance b/d | 20000 | 16000 | – |

| To Sundry Creditors | – | – | 500 | By Sundry drs. a/c | – | – | 2400 |

| To Balance c/d | 18,900 | 18,900 | 5,000 | By Stock a/c | – | – | 1500 |

| To Provision for bad debts | – | – | 240 | By Cash a/c | – | – | 1840 |

| By Cash a/c | – | 4000 | – | ||||

| 20,000 | 20,000 | 5,740 | 20,000 | 20,000 | 5,740 |

Balance Sheet

| Liabilities | Rs. | Assets | Rs. | ||

| Bills Payable | 4,000 | Freehold Premises | 13,560 | ||

| Capital Accounts | Debtors | 23,400 | |||

| G | 18,900 | Less : Provision | 240 | 23,160 | |

| S | 18,900 | Cash in hand (152 + 1840 + 4000) | 5,992 | ||

| T | 5000 | 42,800 | Plant and Machinery | 7,300 | |

| Creditors (15000 + 500) | 15,500 | Stock (4800 + 1500 – 800) | 5,500 | ||

| Cash at Bank | 4,900 | ||||

| Bills Receivable | 1,888 | ||||

| 62,300 | 62,300 |

Working Note:

Calculation of new PSR :

Let total profit = 1

T’s Share = 1/5

Remaining share = 1 – 1/5 = 4/5

G’s new share = 1/2 X 4/5 = 2/5

S’s new share = 1/2 X 4/5 = 2/5

T’s share = 1/5

New PSR = G : S : T = 2 : 2 : 1

T will bring capital in cash :

| S Drs. A/c | Dr. | 2400 | ||

| Stock A/c | Dr. | 1500 | ||

| Cash A/c | Dr. | 1840 (B/F) | ||

| To T’s Capital a/c | 5740 (5000 + 740) | |||

| T’s Capital A/c | Dr. | 740 | ||

| To Sundry Creditors a/c | 500 | |||

| To Provision for doubtful debts a/c | 240 |

What is Partnership – Meaning and Its 4 Types

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication