Question 46 Chapter 1 of +2-Part-1

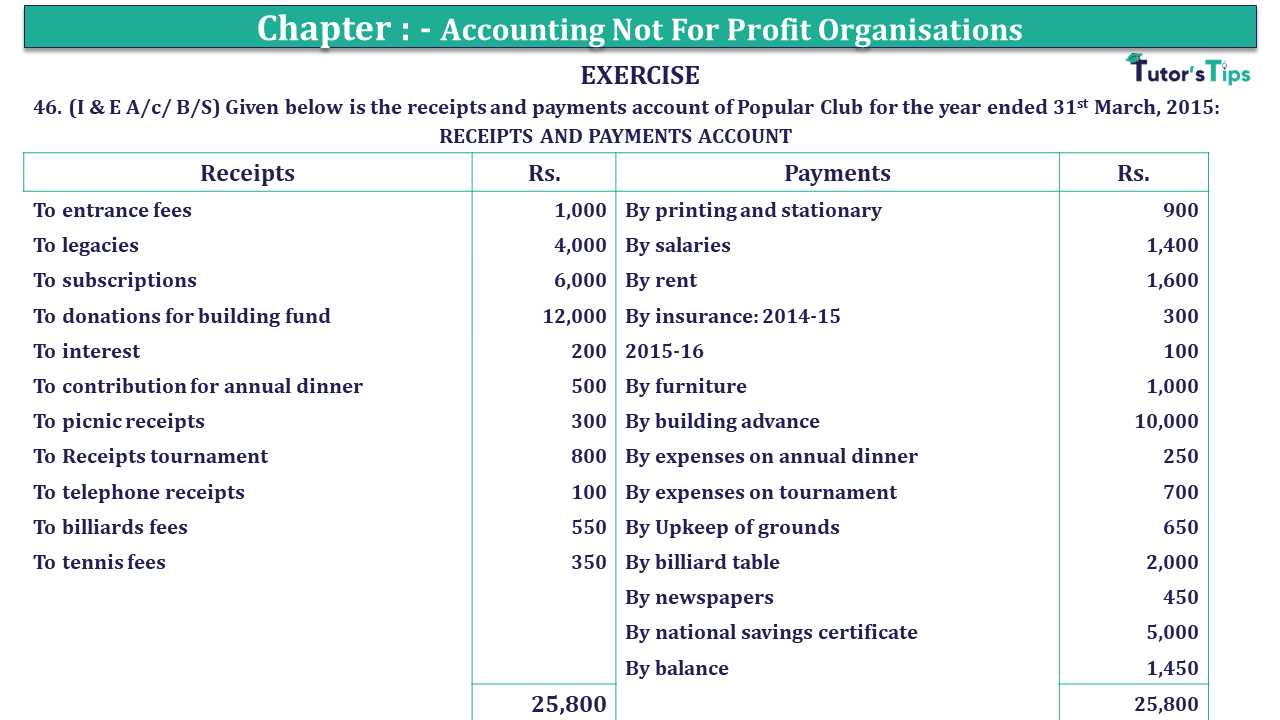

46. (I & E A/c/ B/S) Given below is the receipts and payments account of Popular Club for the year ended 31st March 2015:

| RECEIPTS AND PAYMENTS ACCOUNT | |||

| Receipts | Rs. | Payments | Rs. |

| To entrance fees | 1,000 | By printing and stationary | 900 |

| To legacies | 4,000 | By salaries | 1,400 |

| To subscriptions | 6,000 | By rent | 1,600 |

| To donations for the building fund | 12,000 | By insurance: 2014-15 | 300 |

| To interest | 200 | 2015-16 | 100 |

| To contribution to annual dinner | 500 | By furniture | 1,000 |

| To picnic receipts | 300 | By building advance | 10,000 |

| To Receipts tournament | 800 | By expenses on annual dinner | 250 |

| To telephone receipts | 100 | By expenses on a tournament | 700 |

| To billiards fees | 550 | By Upkeep of grounds | 650 |

| To tennis fees | 350 | By billiard table | 2,000 |

| By newspapers | 450 | ||

| By national savings certificate | 5,000 | ||

| By balance | 1,450 | ||

| 25,800 | 25,800 | ||

Further information:

1) Subscriptions include subscriptions for 2016- Rs.500

2) Subscriptions outstanding for the current year- Rs.800 of which Rs. 200 are considered as doubtful.

3) 60% of the entrance fees are to be capitalized.

4) 12% National Savings Certificates were bought on 31-3-2015

5) Sundry persons owed Rs.200 for advertisement in the club’s yearbook

6) Provide Rs.50 as depreciation on furniture.

You are required to prepare:

(a) the Income and Expenditure Account for the year ended 31st March 2015 and

(b) the balance sheet as of that date.

The solution of Question 46 Chapter 1 of +2 Part-1: –

| Income and Expenditure account of Popular Club For the year ending 31.3.2015 |

|||||

| Expenditure |

Amount | Income |

Amount | ||

| To printing and stationary | 900 | By entrance fees (40%) | 400 | ||

| To salaries | 1,400 | By subscriptions | 6,000 | ||

| To rent | 1,600 | Add: subscription outstanding | 800 | ||

| To insurance | 300 | Less: received in advance | 500 | ||

| To expenses on annual dinner | 250 | Less: provision for doubtful subscription | 200 | 6,100 | |

| To expenses on a tournament | 700 | By interest | 200 | ||

| To Upkeep of grounds | 650 | By interest on NSC | 300 | ||

| To newspapers | 450 | By contribution for annual dinner | 500 | ||

| To depreciation on furniture | 50 | By picnic receipts | 300 | ||

| By Receipts tournament | 800 | ||||

| By telephone receipts | 100 | ||||

| By billiards fees | 550 | ||||

| By tennis fees | 350 | ||||

| By advertisement amount due | 200 | ||||

| To surplus | 3,500 | ||||

| 9,800 | 9,800 | ||||

| Balance Sheet As of 31st March 2015 |

|||||

| Liabilities |

Amount | Assets |

Amount | ||

| Capital Fund: | Insurance prepaid | 100 | |||

| -Balance | – | Building advance | 10,000 | ||

| Add: Surplus | 3,500 | 3,500 | Billiard Table | 2,000 | |

| Entrance fees | 600 | National Savings Certificate | 5,000 | ||

| Donations for building | 12,000 | Furniture | 1,000 | ||

| Subscriptions received in advance | 500 | Less: Depreciation | 50 | 950 | |

| Legacies | 4,000 | Interest on NSC due | 300 | ||

| Cash | 1,450 | ||||

| Advertisement amount due | 200 | ||||

| Subscription outstanding | 600 | ||||

| 20,600 | 20,600 | ||||

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication