Question 43 Chapter 6 – Unimax Class 12 Part 1 – 2021

Table of Contents

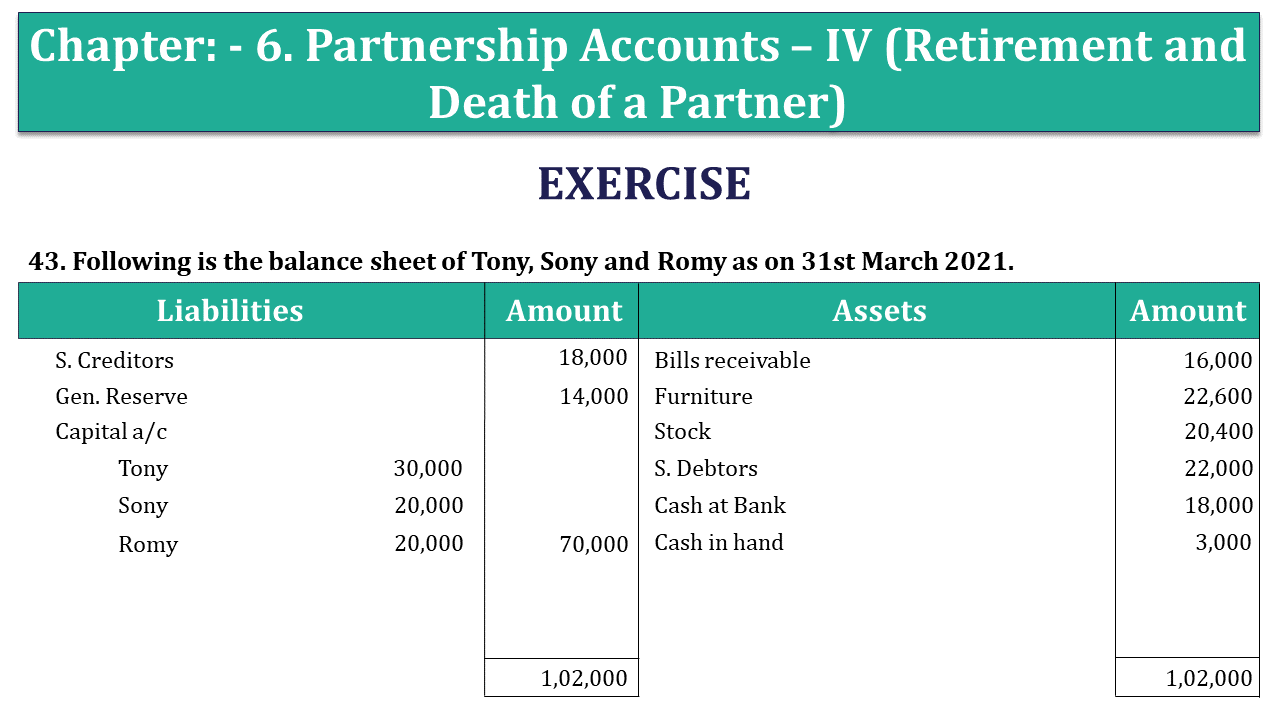

43. Following is the balance sheet of Tony, Sony and Romy as on 31st March 2021.

| Liabilities | Amount | Assets | Amount | |

| S. Creditors | 18,000 | Bills receivable | 16,000 | |

| Gen. Reserve | 14,000 | Furniture | 22,600 | |

| Capital a/c | Stock | 20,400 | ||

| Tony | 30,000 | S. Debtors | 22,000 | |

| Sony | 20,000 | Cash at Bank | 18,000 | |

| Romy | 20,000 | 70,000 | Cash in hand | 3,000 |

| 1,02,000 | 1,02,000 |

Sony died on 30th June 2021. Under the terms of the partnership deed, the executors of a deceased partner were entitled to:

- Amount standing to the credit of the partner’s capital account.

- Interest on capital at 5%per annum.

- Share of Goodwill on the basis of twice the average of the past three year’s profit.

- Share of profit from the closing of the last financial year to the date of death on the basis of the last three year’s profit. Profits for 2019, 2020 and 2021 were ₹12000, ₹ 16000, ₹ 14000 respectively. Profits were shared in the ratio of capitals.

Record the necessary Journal entries and draw up the Sony’s account to be rendered to his executors.

The solution of Question 43 Chapter 6 – Unimax Class 12 Part 1: –

Journal Entry

| Date | Particulars | L.F. | Debit | Credit | |

| Profit and loss suspense a/c | Dr. | 1,000 | |||

| To Sony’s capital a/c | 1,000 | ||||

| (Being share of profit for 3 months paid.) | |||||

| Profit and loss suspense a/c | Dr. | 250 | |||

| To interest on capital a/c | 250 | ||||

| (Being interest on capital transferred to P /L suspense a/c.) | |||||

| Interest on capital a/c | Dr. | 250 | |||

| To Sony’s capital a/c | 250 | ||||

| (Being int. On capital transferred to deceased partner’s capital a/c) | |||||

| General reserves a/c | Dr. | 14,000 | |||

| To Tony’s capital a/c | 6,000 | ||||

| To Sony’s capital a/c | 4,000 | ||||

| To Romy’s capital a/c | 4,000 | ||||

| (Being accumulated profit distributed among partners) | |||||

| Tony’s capital a/c | Dr. | 4,800 | |||

| Romy’s capital a/c | Dr. | 3,200 | |||

| To Sony’s capital a/c | 8,000 | ||||

| (Being deceased partner paid on account of Goodwill by continuing partners) | |||||

| Sony’s capital a/c | Dr. | 33,250 | |||

| To sony’s executor’s loan a/c | 33,250 | ||||

| (Being balance of Sony’s capital transferred to his executors loan a/c) |

Sony’s capital A/c

| Particulars | Amount | Particulars | Amount |

| To son’s executors loan a/c | 33,250 | By Bal. C/d | 20,000 |

| By general res. a/c 14000×2/7 | 4,000 | ||

| By Tony’s capital a/c | 4,800 | ||

| By Romy’s capital a/c | 3,200 | ||

| By profit/loss susp. a/c 14000×3/12 ×2/7 (A.P.) | 1,000 | ||

| By Interest on capital a/c 20000×5/100 ×3/12 | 250 | ||

| 33,250 | 33,250 |

1) Sony’s share of Goodwill =12000/3+16000/3+14000/3 ×2× 2/7 = ₹6000

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication