Question 40 Chapter 1 of Class 12 Part – 1

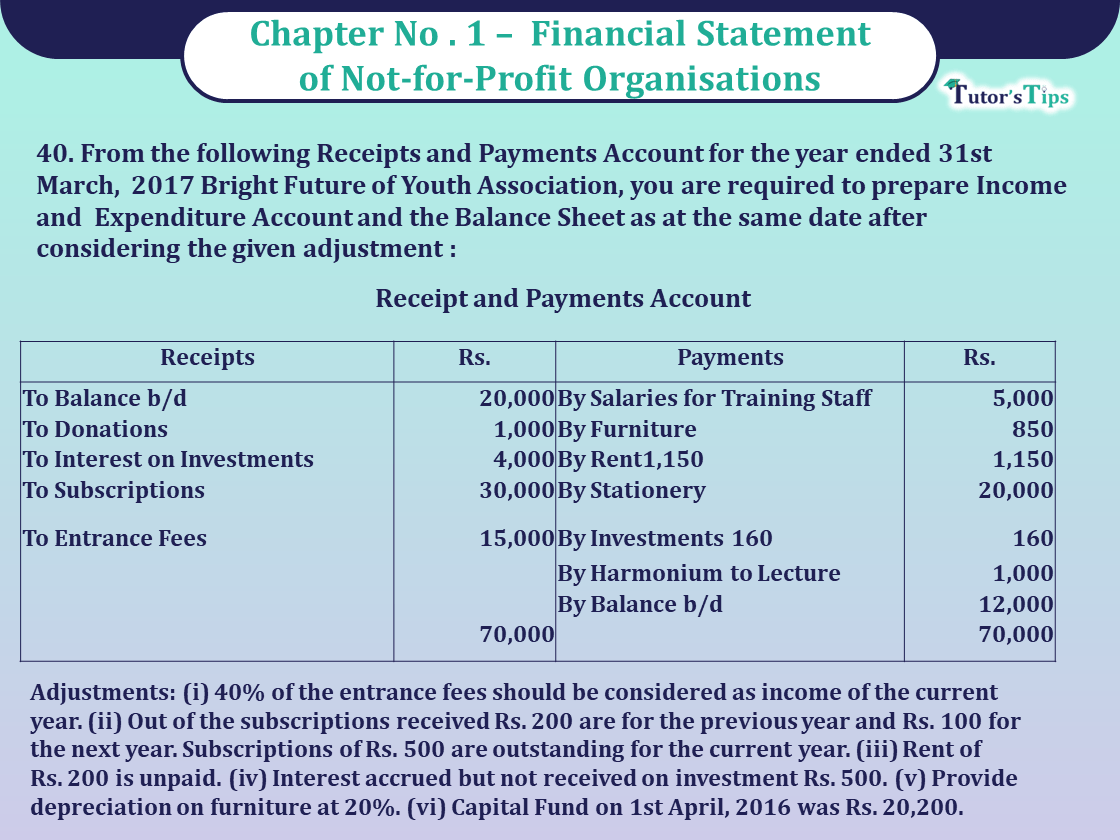

40. From the following Receipts and Payments Account for the year ended 31st March, 2017 Bright Future of Youth Association, you are required to prepare Income and Expenditure Account and the Balance Sheet as at the same date after considering the given adjustment :

Receipt and Payments Account

| Receipts | Rs. | Payments | Rs. |

| To Balance b/d | 20,000 | By Salaries for Training Staff | 5,000 |

| To Donations | 1,000 | By Furniture | 850 |

| To Interest on Investments | 4,000 | By Rent | 1,150 |

| To Subscriptions | 30,000 | By Stationery | 20,000 |

| To Entrance Fees | 15,000 | By Investments | 160 |

| By Harmonium to Lecture | 1,000 | ||

| By Balance b/d | 12,000 | ||

| 70,000 | 70,000 |

Adjustments: (i) 40% of the entrance fees should be considered as income of the current

year. (ii) Out of the subscriptions received Rs. 200 are for the previous year and Rs. 100 for the next year. Subscriptions of Rs. 500 are outstanding for the current year. (iii) Rent of

Rs. 200 is unpaid. (iv) Interest accrued but not received on investment Rs. 500. (v) Provide

depreciation on furniture at 20%. (vi) Capital Fund on 1st April, 2016 was Rs. 20,200.

The solution of Question 40 Chapter 1 of Class 12 Part – 1: –

Bright Future of Youth Association

Income and Expenditure Account

For the year ended on 31st March, 2017

| Expenditure |

Amount | Income |

Amount | ||

| To Salaries for Training | 30,000 | By Donation | 1,000 | ||

| To Rent | 850 | By Interest on Investment | 4,000 | ||

| Add. Outstanding | 200 | 1,050 | Add: Accrued Interest | 500 | 4,500 |

| To Stationery | 1,150 | By Subscriptions | 30,000 | ||

| To Honorarium to Lecturer | 1,000 | Less: Received for previous year | (200) | ||

| To Depreciation on Furniture | 1,000 | Less: Received in advance for next year | (100) | ||

| To Surplus, ie., Excess of Income over Expenditure | 7,500 | Add: Outstanding for current year | 500 | 30,200 | |

| By Entrance fees (40% of Rs. 15,000) | 6,000 | ||||

| 41,700 | 41,700 | ||||

Balance Sheet (as at 31st March 2018)

| Liabilities |

Amount | Assets |

Amount | ||

| Capital Fund | 20,200 | Investment | 20,000 | ||

| Add. Surplus | 7,500 | 27,700 | Add: Accrued Interest | 500 | 20,500 |

| Outstanding Rent | 200 | Furniture | 5,000 | ||

| Entrance fees (15,000-6,000) | 9,000 | Less: Depreciation | 1,000 | 4,000 | |

| Subscriptions received in advance | 100 | Cash | 12,000 | ||

| Outstanding Subscriptions | 500 | ||||

| 37,000 | 37,000 | ||||

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of all Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

Chapter No. 1 – Accounting Not for Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Introduction)

Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

Chapter No. 1 – Financial Statements of a Company

Chapter No. 2 – Financial Statement Analysis

Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

Chapter No. 4 – Ratio Analysis

Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication