Question 39 Chapter 6 – Unimax Class 12 Part 1 – 2021

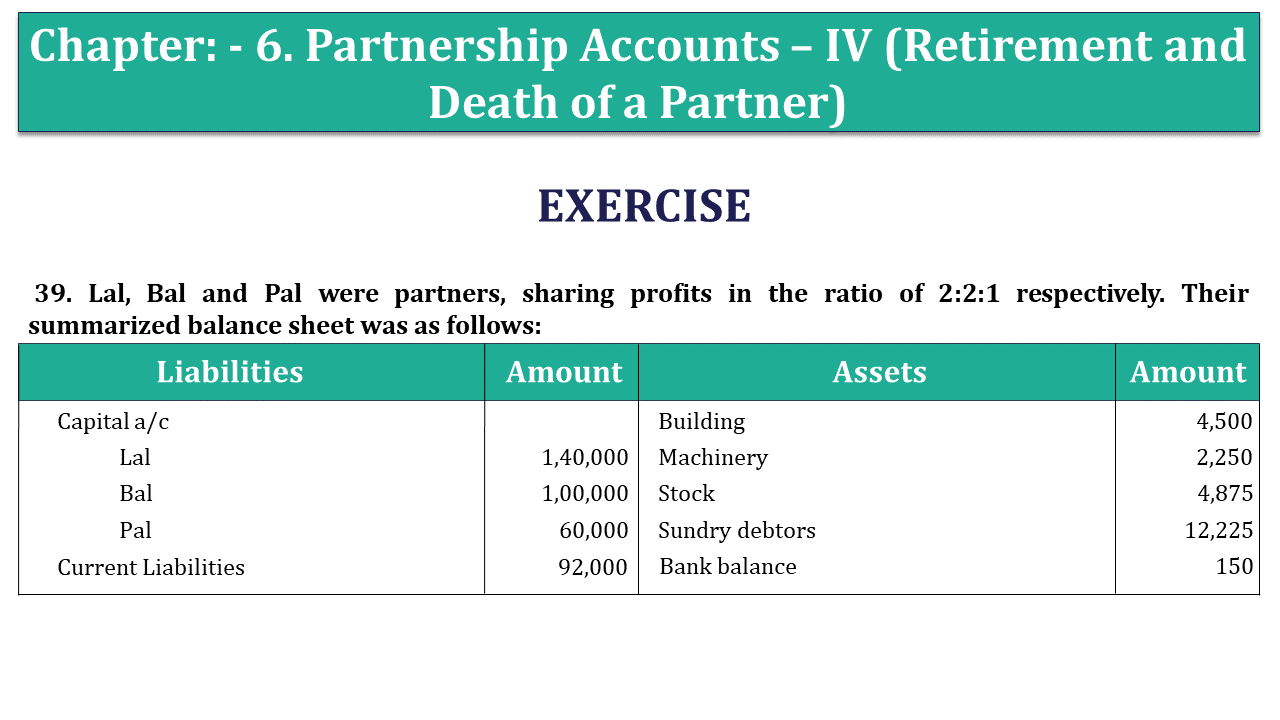

39. Lal, Bal and Pal were partners, sharing profitsin the ratio of 2:2:1 respectively. Their summarized balance sheet was as follows:

| Liabilities | Amount | Assets |

Amount | ||

| Capital a/c | Goodwill | 40,000 | |||

| Lal | 1,40,000 | Fixed assets | 1,80,000 | ||

| Bal | 1,00,000 | Debtors | 70,000 | ||

| Pal | 60,000 | Stock | 90,000 | ||

| Current Liabilities | 92,000 | Cash at Bank | 12,000 | ||

Pal retired and his interest in respect of Goodwill and capital valued at ₹80000 was purchased by Lal and Bal by bringing in cash in the proportion in which they share profits. Bsl’s son Dev was admitted to a partnership on the following terms:

- Dev would bring ₹ 100000 in the business for one-fourth share in profits, to be surrendered by Bal.

- Goodwill is to be written off and fixed assets to be revalued at ₹240000 immediately before his admission to partnership.

- Capitals of Lal and Bal to be adjusted according to new profit sharing ratio taking Dev’s

capital as base.

Prepare capital a/c, Bank a/c, Balance sheet of the reconstituted firm.

The solution of Question 39 Chapter 6 – Unimax Class 12 Part 1: –

Revaluation account

| Particulars | Rs. | Particulars | Rs. | ||

| To profit on revaluation | By fixed assets a/c | 60,000 | |||

| Lal | 30,000 | ||||

| Bal | 30,000 | 60,000 | |||

| 60,000 | 60,000 |

Partners Capital accounts

| Particulars | Lal | Bal | Pal | Dev | Particulars | Arthur | Baldwin | Curtis | |

| To Pal | 10,000 | 10,000 | By balance b/d | 1,40,000 | 1,00,000 | 60000 | |||

| To bank a/c | 80,000 | By Lal | 10000 | ||||||

| To goodwill a/c | 20,000 | 20,000 | By Bal | 10000 | |||||

| To bank a/c | 40,000 | By bank | 40,000 | 40,000 | |||||

| To balance c/d | 2,00,000 | 1,00,000 | By profit on rev. | 30,000 | 30,000 | ||||

| By bank a/c | 1,00,000 | ||||||||

| By bank a/c | 20,000 | ||||||||

| 2,30,000 | 1,70,000 | 80,000 | 1,00,000 | 2,30,000 | 1,70,000 | 80,000 | 1,00,000 |

Balance sheet

| Liabilities | Amount | Assets | Amount | ||

| Capitals | Fixed assets | 240000 | |||

| Lal | 2,00,000 | Debtors | 70000 | ||

| Bal | 1,00,000 | Stock | 90000 | ||

| Pal | 1,00,000 | 4,00,000 | Bank | 12000 | |

| Current liabilities | 92,000 | Cash (80000+100000+20000-80000 -40000) | 80000 | ||

| 4,92,000 | 4,92,000 |

WORKING NOTE:

1) Pal’s interest includes ₹80000 (₹60000 for capital and ₹20000for goodwill which is to be paid by Lal and Bal in 1:1) and paid by bringing cash ₹80000by Lal and Bal in 1:1Arthur =5/8 – 4/9= 45/72-32/72 = 13/72.

2) Revaluation and goodwill has been written off after retirement.

3) Total capital of firm =100000×4/1.

4) Dev’s capital base=₹ 400000 to be divided in ratio 2:1:1.

Retirement of a Partner – Explained with Illustration

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication