Question 31 Chapter 7 of +2-Part-1

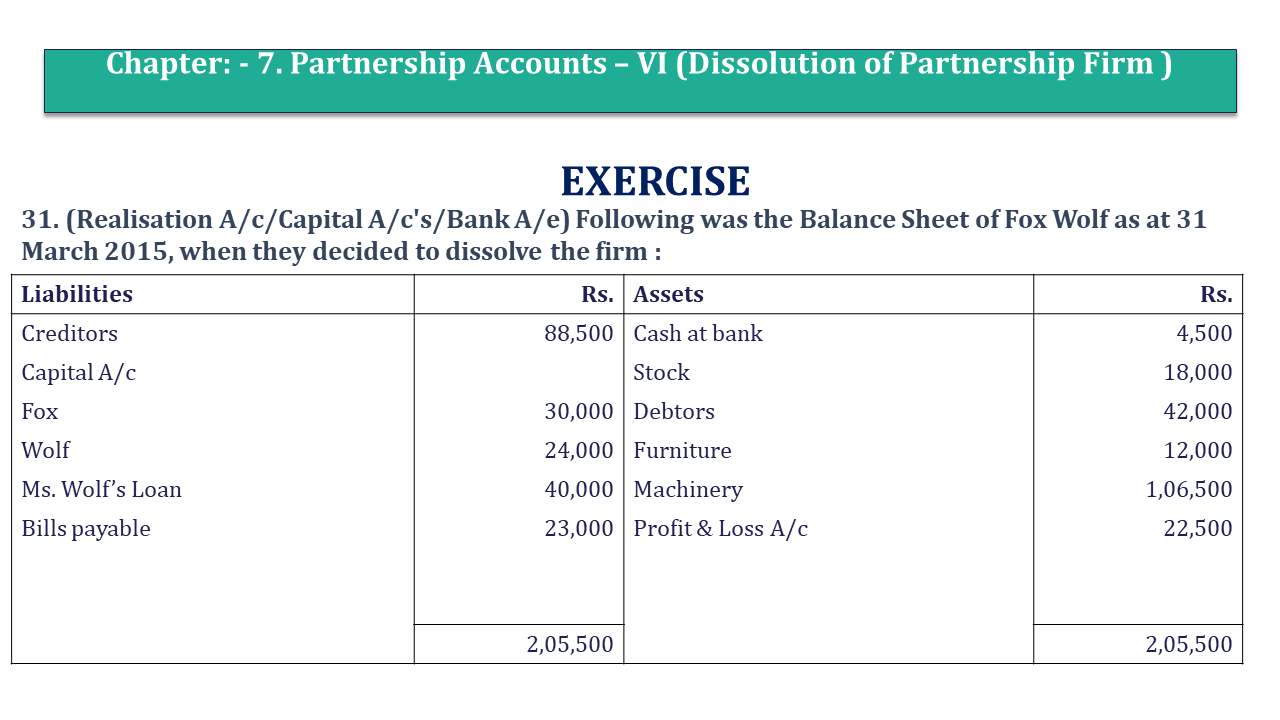

31. (Realisation A/c/Capital A/c’s/Bank A/e) Following was the Balance Sheet of Fox Wolf as at 31 March 2015, when they decided to dissolve the firm :

| Liabilities | Rs. | Assets | Rs. |

| Creditors | 88,500 | Cash at bank | 4,500 |

| Capital A/c | Stock | 18,000 | |

| Fox | 30,000 | Debtors | 42,000 |

| Wolf | 24,000 | Furniture | 12,000 |

| Ms. Wolf’s Loan | 40,000 | Machinery | 1,06,500 |

| Bills payable | 23,000 | Profit & Loss A/c | 22,500 |

| 2,05,500 | 2,05,500 |

The assets realised stock Rs. 10,500. Debtors 27,750, Machinery Rs. 89,000 Furniture was taken by Fox at Rs. 7,500. Bills payable were paid in full, while creditors were settled at 2% discount. Ms. Wolf accepted Rs. 38,500 in full settlement of her loan account There was claim for damages against the firm for Rs. 4,000 which was settled at Rs. 2,000.

One customer, whose account was written off as bad, now paid Rs. 1,800, which is not include in Rs. 27,750 given above actual realisation expenses amounted to Rs. 2,100.

Prepare the Realisation Account, Partner’s Capital Account and Bank Account to close the books of the firm.

The solution of Question 31 Chapter 7 of +2 Part-1: –

| Revaluation A/c |

|||||

| Particulars |

Amount | Particulars | Amount | ||

| To Sundry Assets Transfer | By Sundry liabilities | ||||

| To Stock A/c | 18,000 | Transfer creditors A/c | 88,500 | ||

| Debtors A/c | 42,000 | Bills payable A/c | 23,000 | ||

| Furniture | 12,000 | Ms. Wolf A/c | 40,000 | 1,51,500 | |

| Machinery A/c | 1,06,500 | 1,78,500 | By Bank A/c | ||

| To Bank A/c | Assets realised | ||||

| Liabilities paid off | Stock | 10,500 | |||

| Bills payable | 23,000 | Debtors | 27,750 | ||

| Creditors | 86,730 | Machinery | 89,000 | 1,27,250 | |

| Mrs. Wolf | By Fox ’s capital A/c | ||||

| Loan | 38,500 | Furniture taken over | 7,500 | ||

| Claim for damages | 2,000 | 1,50,230 | By Bank A/c (recovery for bad debts ) | 1,800 | |

| To Bank A/c Expenses | 2,100 | By loss on realisation | |||

| Fox ’s capital A/c | 21,390 | ||||

| Wolf ’s capital A/c | 21,390 | 42,780 | |||

| 3,30,830 | 3,30,830 | ||||

| Partners’ Capital Account |

|||||

| Particulars | Fox | Wolf | Particulars | Fox | Wolf |

| To Profit & loss A/c | 11,250 | 11,250 | By Balance b/d | 30,000 | 24,000 |

| To Realisation A/c – – | By Bank A/c | 10,140 | 8,640 | ||

| Furniture taken over | 7,500 | ||||

| To Realisation A/c – loss | 21,390 | 21,390 | |||

| 40,140 | 32,640 | 40,140 | 32,640 | ||

| Bank A/c |

|||||

| Particulars | Amount | Particulars | Amount | ||

| To balance b/d | 4,500 | By Realisation A/c | 1,50,230 | ||

| To Realisation A/c | By Bank A/c | 2,100 | |||

| Assets realised | 1,27,250 | ||||

| Recovery for bad debts | 1,800 | 1,29,050 | |||

| To Fox ’s capital A/c (cash brought in ) | 10,140 | ||||

| To Wolf’s capital A/c (cash brought in ) | 8,640 | ||||

| 1,52,330 | 1,52,330 | ||||

Note : 1. Profit sharing ratio is not given . Therefore , profit/losses shall be shared equally .

2. Claim for damages was Rs. 4,000 but it was settled for Rs. 2,000 . Therefore , Rs. 2,000 shall be debited to Realisation Account .

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication