Question 10 Chapter 5 – Unimax

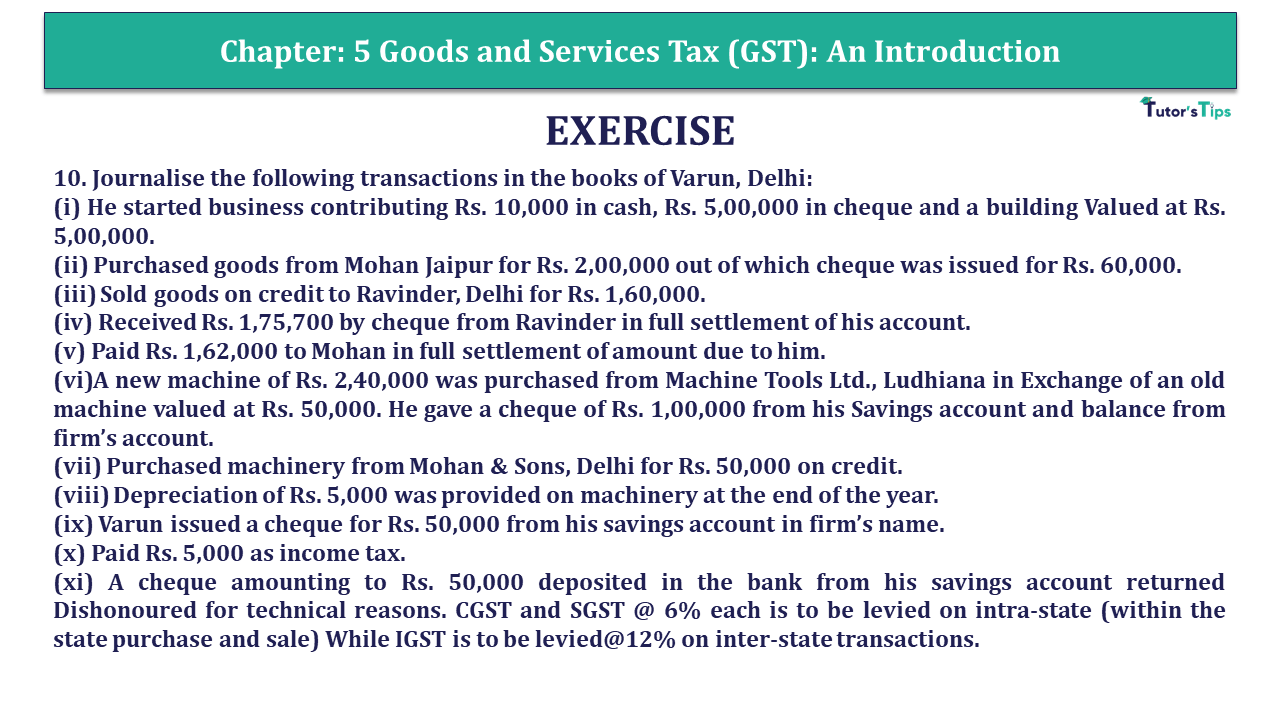

10. Journalise the following transactions in the books of Varun, Delhi:

(i) He started business contributing Rs. 10,000 in cash, Rs. 5,00,000 in cheque and a building Valued at Rs. 5,00,000.

(ii) Purchased goods from Mohan Jaipur for Rs. 2,00,000 out of which cheque was issued for Rs. 60,000.

(iii) Sold goods on credit to Ravinder, Delhi for Rs. 1,60,000.

(iv) Received Rs. 1,75,700 by cheque from Ravinder in full settlement of his account.

(v) Paid Rs. 1,62,000 to Mohan in full settlement of amount due to him.

(vi)A new machine of Rs. 2,40,000 was purchased from Machine Tools Ltd., Ludhiana in Exchange of an old machine valued at Rs. 50,000. He gave a cheque of Rs. 1,00,000 from his Savings account and balance from firm’s account.

(vii) Purchased machinery from Mohan & Sons, Delhi for Rs. 50,000 on credit.

(viii) Depreciation of Rs. 5,000 was provided on machinery at the end of the year.

(ix) Varun issued a cheque for Rs. 50,000 from his savings account in firm’s name.

(x) Paid Rs. 5,000 as income tax.

(xi) A cheque amounting to Rs. 50,000 deposited in the bank from his savings account returned Dishonoured for technical reasons. CGST and SGST @ 6% each is to be levied on intra-state (within the state purchase and sale) While IGST is to be levied@12% on inter-state transactions.

The solution of Question 10 Chapter 5 – Unimax:

IN THE BOOKS OF MR. VARUN JOURNAL

| Date | Particulars | L.F. | Debit | Credit | |

| (i) | Cash A/c | Dr. | 10,000 | ||

| Bank A/c | Dr. | 5,00,000 | |||

| Building A/c | Dr. | 5,00,000 | |||

| To Capital A/c | 10,10,000 | ||||

| (Being the business started with cash 10,000, cheque 5,00,000 and building of 5,00,000) | |||||

| (ii) | Purchases A/c | Dr. | 2,00,000 | ||

| Input IGST A/c | Dr. | 24,000 | |||

| To Bank A/c | 60,000 | ||||

| To Mohan A/c | 1,64,000 | ||||

| (Being the goods purchased from Mohan Jaipur paying GST 12%, issued cheque for 60,000) | |||||

| (iii) | Ravinder A/c | Dr. | 1,79,200 | ||

| To Sales A/c | 1,60,000 | ||||

| To Output CGST A/c | 9,600 | ||||

| To Output SGST A/c | 9,600 | ||||

| (Being the intra-state sale of goods to Ravinder, Delhi on Credit for 1,60,000, charging CGST and SGST 6% 1,75,700 Each) | |||||

| (iv) | Bank A/c | Dr. | 1,75,700 | ||

| Discount Allowed A/c | Dr. | 3,500 | |||

| To Ravinder A/c | 1,79,200 | ||||

| (Being the cheque received from Ravinder and allowed him Discount of 4,000) | |||||

| (v) | Mohan A/c | Dr. | 1,64,000 | ||

| To Bank A/c | 1,62,000 | ||||

| To Discount Received A/c | 2,000 | ||||

| (Being 1,62,000 paid to D. Lal in full settlement of his dues And discount received) | |||||

| (vi) | Machinery A/c (New) | Dr. | 2,40,000 | ||

| Input IGST A/c | Dr. | 28,800 | |||

| To Machine Tools A/c | 2,68,800 | ||||

| (Being a new machine purchased, paying IGST 12%) | |||||

| Machine Tools A/c | Dr. | 2,68,800 | |||

| To Machinery A/c | 50,000 | ||||

| To Output CGST A/c | 6,000 | ||||

| To Capital A/c | 1,00,000 | ||||

| To Bank A/c | 1,12,800 | ||||

| (Being an old machine given in settlement charging IGST 12%, a cheque of 1,00,000 from savings account and Balance from Firms account) | |||||

| (vii) | Machinery A/c | Dr. | 50,000 | ||

| Input CGST A/c | Dr. | 3,000 | |||

| Input SGST A/c | Dr. | 3,000 | |||

| To Sales A/c | 56,000 | ||||

| (Being the purchase of machinery on credit from Mohan & Sons) | |||||

| (viii) | Depreciation A/c | Dr. | 5,000 | ||

| To Machinery A/c | 5,000 | ||||

| (Being the depreciation charged on machinery for the year) | |||||

| (ix) | Bank A/c | Dr. | 50,000 | ||

| To Capital A/c | 50,000 | ||||

| (Being the cheque from proprietor’s savings account) | |||||

| (x) | Drawings A/c | Dr. | 5,000 | ||

| To Cash A/c | 5,000 | ||||

| (Being the income tax paid) | |||||

| (xi) | Capital A/c | Dr. | 50,000 | ||

| To Bank A/c | 50,000 | ||||

| (Being the cheque deposited into bank dishonoured) | |||||

Note: An old machine given in exchange means sale of an old machine. Therefore, IGST is charged, it being inter-state sale.

This is all about the Question 10 Chapter 5 – Unimax. You can check out the following article to better understand:

Opening Journal Entry – its Rules and Examples

You Can also read all above articles in Hindi on our Hindi Website

Opening Journal Entry – its Rules and Examples – In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in the Question 10 Chapter 5 – Unimax.

You can also Check out the solved question of other Chapters: –

Advanced Accountancy – Unimax Class 11 – 2021 – Solution.

Part-I

- Chapter No. 1 – Introduction of Accounting

- Chapter No. 2 – Theory Base of Accounting

- Chapter No. 3 – Vouchers and Transactions

- Chapter No. 4 – Journal

- Chapter No. 5 – Goods and Services Tax (GST) : An Introduction

- Chapter No. 6 – Ledger

- Chapter No. 7 – Special Purpose Book – Cash Book

- Chapter No. 8 – Other Subsidiary Books

- Chapter No. 9 – Trial Balance

- Chapter No. 10 – Rectification of Errors

- Chapter No. 11 – Depreciation

- Chapter No. 12 – Provision and Reserves

- Chapter No. 13 – Bank Reconlciliation Statement

- Chapter No. 14 – Bills of Exchange

Students may Choose only one part from the Part II and Part III

Part-II

- Chapter No. 15 – Financial Statements (Without Adjustments)

- Chapter No. 16 – Financial Statements (With Adjustments)

- Chapter No. 17 – Accounts from Incomplete Records – Single Entry System

Part-III

- Chapter No. 18 – Introduction to Compurters and Accounting information System

- Chapter No. 19 – Computerised Accounting

- Chapter No. 20 – Accounting Software : Tally

- Chapter No. 21 – Data Base System

- Chapter No. 22 – Concept of Entity and Relationship

You can also Check out the other Books’ Solution: –

- Usha Publication – Elements of Book-Keeping PSEB (Class 11) – Solution

- T.S. Grewal’s Double Entry Book Keeping (Class +1) – Solution

- D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution