The basic difference between Reserve Capital and Capital Reserve(CR) is that one is part of the capital and another is part of the capital profit respectively. To know the difference between these two, we must clarify the meaning of these terms and explain as follows: –

Meaning of Reserve Capital:

It is the part of subscribed Capital that is not called up yet. These types of shares are known as subscribed but not fully paid up. The company will call this capital in the event of being wound up. We have explained it with the help of the following:

Example:

M/s RAJ Industries Ltd. issued a 50,000 share at Rs. 100. All shares were subscribed by the public. The share money is called up by the following 4 calls:

on Application Rs 25,

on Allotment Rs 35,

on 1st calls Rs 15,

on 2nd and final calls Rs 25

Company Called up the value of shares up to the 1st calls only.

Calculate the amount of Reserved Capital.

Solution: –

Reserved Capital = UnCalled Capital

= Total Numbers of share X uncalled Call

= 50,000 X 25

= 12,50,000/-

Meaning of Capital Reserve:

It is the part of capital profit created for capital expenditure not free to distribute as dividends. It can be created in many ways. But we are showing one way with the help of the following example:

Example:

M/s RAJ Industries Ltd. issued a 50,000 share at Rs. 100. All shares were subscribed by the public. The share money is called up by the following 4 calls:

on Application Rs 25,

on Allotment Rs 35,

on 1st calls Rs 15,

on 2nd and final calls Rs 25

All shares are fully paid except Mr Nand Lal who is holding 100 shares failed to pay 2nd and final call. So after some time, His shares were forfeited and reissued as fully paid up @ Rs 100.

Calculate the balance of Shares forfeited transferred to CR.

Solution: –

Calculation of Balance of Share forfeited:

Total amount received from the Mr Nand Lal

= 100 * (25+35+15)

= 100 * 75

= 7,500/-

All calls were received except 2nd and final call.

All forfeited shares were reissued at face value so the total balance of the share forfeited account will be transferred to the CR.

= 7,500/-

So, it is created.

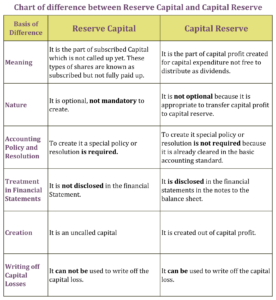

Chart of Difference Between Reserve Capital and Capital Reserve

|

Basis of Difference |

Reserve Capital |

Capital Reserve |

| Meaning | It is the part of subscribed Capital that is not called up yet. These types of shares are known as subscribed but not fully paid up. | It is the part of capital profit created for capital expenditure not free to distribute as dividends. |

| Nature | It is optional, not mandatory to create. | It is not optional because it is appropriate to transfer capital profit into it. |

| Accounting Policy and Resolution | To create it a special policy or resolution is required. | To create it special policy or resolution is not required because it is already cleared in the basic accounting standard. |

| Treatment in Financial Statements | It is not disclosed in the financial Statement. | It is disclosed in the financial statements in the notes to the balance sheet. |

| Creation | It is an uncalled capital | It is created out of capital profit. |

| Writing off Capital Losses | It can not be used to write off the capital loss. | It can be used to write off the capital loss. |

Download the chart in PNG and PDF:-

If you want to download the chart please download the following image and PDF file:-

Conclusion:

Thus, both terms are very different from each other because one is part of the capital and the other is part of the capital profit. These are not dependent on each other. Only one can also be there in the books.

Thanks for reading the topic.

please comment with your feedback with whatever you want. If you have any questions please ask us by commenting.

Check out T.S. Grewal’s +2 Book 2020 Official Website of Sultan Chand Publication