Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

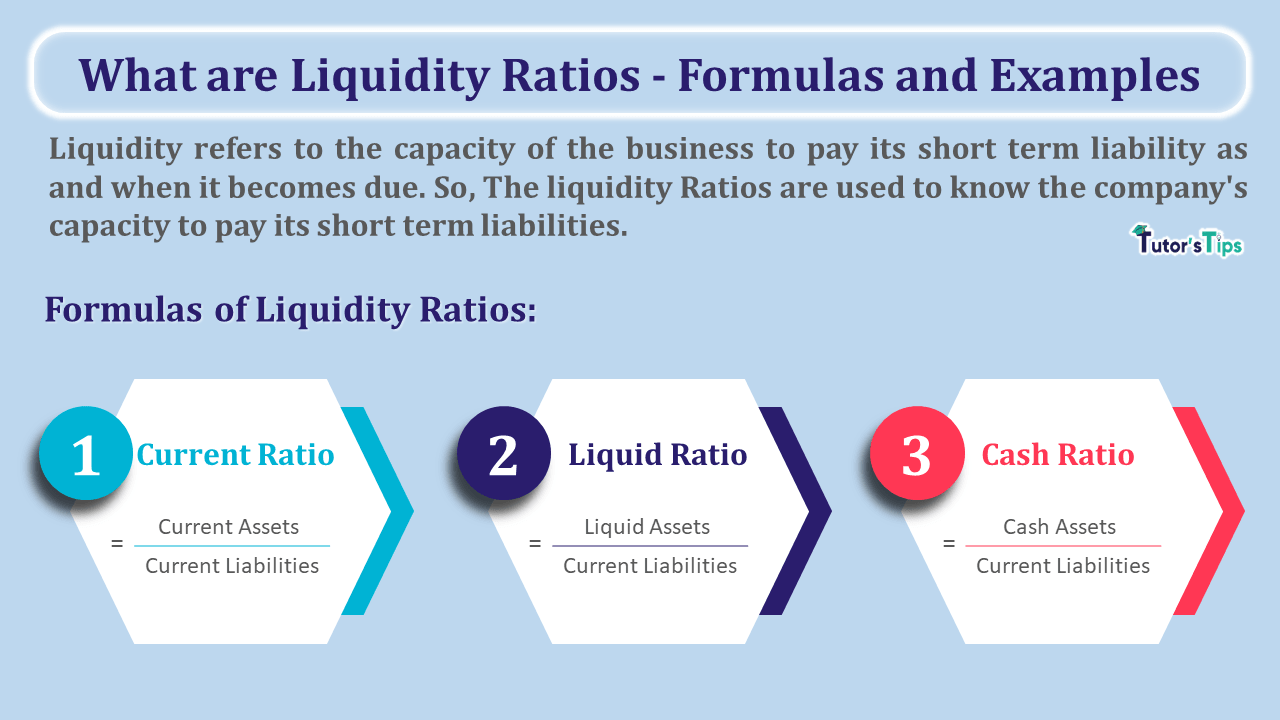

Liquidity Ratios show the capacity of the company to repay its current liabilities by realising the current assets. It is the basic ratio of the accounting ratios.

Liquidity refers to the capacity of the business to pay its short term liability as and when it becomes due. So, The liquidity Ratios are used to know the company's capacity to pay its short term liabilities.

To pay the short term liabilities means paid the total due amount of short term liabilities by realising amount from the company's short term assets.

Liquidity ratio provides us with information about the liquidity of the business. The high liquidity ratio ensures that the company is in a good position to meet its financial obligation and the low liquidity ratio shows the low capacity of the firm to meet its financial obligation and it will lead to bankruptcy and fall down the credit rating of the business.

To Check out the liquidity of the business we can use the following three formulas:

The current ratio is used to compare the current assets with current liabilities of the business.

| Current Ratio | = | Current Assets |

| Current Liabilities |

The Quick or liquid Ratio is used to compare the Liquid assets with current liabilities of the business.

| Current Ratio | = | Liquid Assets |

| Current Liabilities |

The Absolute liquid or cash ratio is used to compare the Absolute liquid assets with current liabilities of the business.

| Current Ratio | = | Absolute liquid Assets |

| Current Liabilities |

The following table will help you to understand the type of assets which are included in these assets:

| Type of Asset | Included in |

||

|---|---|---|---|

| Current Assets | Liquid Assets | Cash Assets | |

| Cash and cash equivalents - i.e. Cash in hand, cash at bank, cheques/demand draft in hand, etc. |

Yes | Yes | Yes |

| Marketable or short term Security | Yes | Yes | Yes |

| Trade Receivables - i.e. Sundry Debtors and Bills receivable - provision of doubtful debts. |

Yes | Yes | No |

| Inventory : Raw material, Work in progress and Finished goods |

Yes | No | No |

| Prepaid Expenses | Yes | No | No |

| Short term loans and advances |

Yes | No | No |

You can use it as a ready reckoner for solving the questions of liquidity ratios.

The following is the extracted balance sheet which shows the current assets and current liabilities. Calculate the liquid ratios.

Balance Sheet as on 31st March 2020

| Particulars | Note No. | 31, March 2020 |

|---|---|---|

| I. Equity and Liabilities | ||

| (3) Current Liabilities | ||

| (a) Sundry Creditors | 75,000 | |

| (b) Bills payables | 15,000 | |

| (c) Outstanding Expenses | 5,000 | |

| (d) Bank Overdraft | 55,000 | |

| Total Current Liabilities | 1,50,000 | |

| II. Assets | ||

| (2) Current Assets | ||

| (a) Cash in hand | 10,000 | |

| (b) Cash at Bank | 40,000 | |

| (c) Inventories | 1,35,000 | |

| (d) Trade Receivables | 75,000 | |

| (e) Marketable security | 25,000 | |

| (f) Prepaid Expenses | 15,000 | |

| Total Current Assets | 3,00,000 | |

| Total Assets |

1. Calculation of Current Ratio:

| Current Ratio | = | Current Assets |

| Current Liabilities |

| = | Cash in hand + Cash at Bank + Inventories + Trade Receivables + Marketable security + Prepaid Expenses |

| Sundry Creditors + Bills payables + Outstanding Expenses + Bank Overdraft |

| = | 10,000 + 40,000 + 1,35,000 + 75,000 + 25,000 + 15,000 |

| 75,000 + 15,000 + 5,000 + 55,000 |

| = | 3,00,000 |

| 1,50,000 |

Current Ratio = 2 : 1

2. Calculation of Liquid Ratio:

| Liquid Ratio | = | Liquid Assets |

| Current Liabilities |

| = | Cash in hand + Cash at Bank + Trade Receivables + Marketable security |

| Sundry Creditors + Bills payables + Outstanding Expenses + Bank Overdraft |

| = | 10,000 + 40,000 + 75,000 + 25,000 |

| 75,000 + 15,000 + 5,000 + 55,000 |

| = | 1,50,000 |

| 1,50,000 |

Liquid Ratio = 1 : 1

2. Calculation of Absolute Liquid or cash Ratio:

| Absolute Liquid or cash Ratio | = | Absolute Liquid or cash Assets |

| Current Liabilities |

| = | Cash in hand + Cash at Bank + Marketable security |

| Sundry Creditors + Bills payables + Outstanding Expenses + Bank Overdraft |

| = | 10,000 + 40,000 + 25,000 |

| 75,000 + 15,000 + 5,000 + 55,000 |

| = | 75,000 |

| 1,50,000 |

Absolute Liquid or cash Ratio = 0.5 : 1

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Liquidity Ratios show the capacity of the company to repay its current liabilities by realising the current assets. It is the basic ratio of the accounting…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.