Focus Topic:Triple Column Cash Book | Explained with Example

Estimated Reading Time:4 mins

In Cashbook, we will record the all-cash transaction of the business. This book keeps a record of all cash payments and cash receipts. In this article, we will…

Syllabus-aligned study material with detailed definitions, formats, and practical examples.

Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

In Cashbook, we will record the all-cash transaction of the business. This book keeps a record of all cash payments and cash receipts. In this article, we will discuss the Triple Column Cash Book, its format and example.

What is the Triple Column Cash Book?

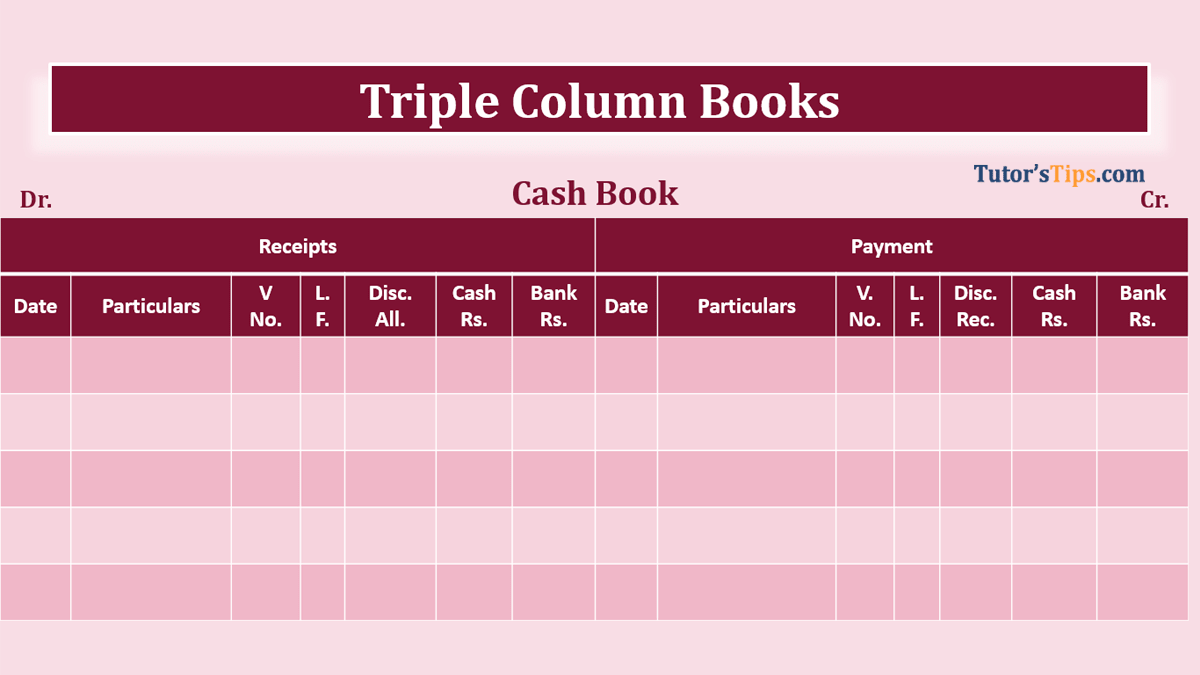

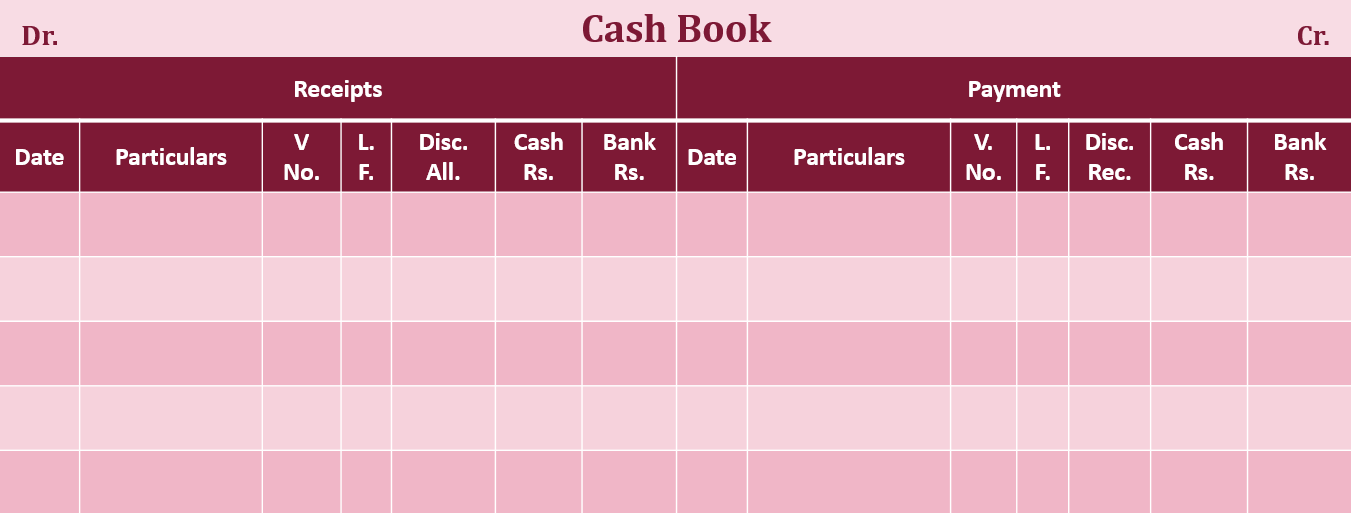

In Triple Column Cash Book there are three columns in the cash book because every Businessman has a minimum of one current account in the bank. It is a very convenient way for him to get paid by cheque and make payments to others by cheque. So, he has to record these payments and receipts in the cash book for this an additional column will require a named bank column. So now a total three-column will be required to record the proper payment and receipts in the cash book these are shown below

The format of the triple Column Cash Book is explained as under:

The Columns of the Triple Column Cash Book are explained Below:-

Date:

Particulars:

V. NO (Voucher Number):

L.F. (Ledger Folio):

Amount ( It Included three columns i.e. 1. Discount, 2. Cash and 3. Bank.)

Explanation of all columns:

1. Date:

The date of the transaction is written in this column —in the first row, we will write the year till it will not change and in the subsequent rows, write the name of the month followed by the actual date.

2. Particulars:

In this column, the name of the opposite account is written (the second aspect of cash transaction). Below is written the narration of the transaction.

3. Voucher Number (V. NO.):

The voucher number for each item of receipt and payment is also written. A voucher is necessary for each item of receipt and payment. Generally, a voucher has a serial number and this number is written in this column (V. No).

4. L.F. (Ledger Folio):

The page number of the Ledger where the concerned (opposite ) account has been opened, is written in this column. This will help to locate the account from the Ledger. It may be noted that in a Ledger account, J.F. is written as the reference, while in a Cash Book L.F. is written.

5. Amount Columns:

All the Above columns are the same as the single & double-column cash book but instead of the amount column, three different columns are prepared i.e. 1. Discount, 2. Cash and 3. Bank.

1. Discount Column:

In the discount Column, we have to record the discount received on the credit side of the cash book and the discount allowed on the debit side of the cash book.

2. Cash Column:

All the payments and receipts made by cash are recorded in this column.

3. Bank Column:

All the payments and receipts made by the bank/ Cheque are recorded in this column.

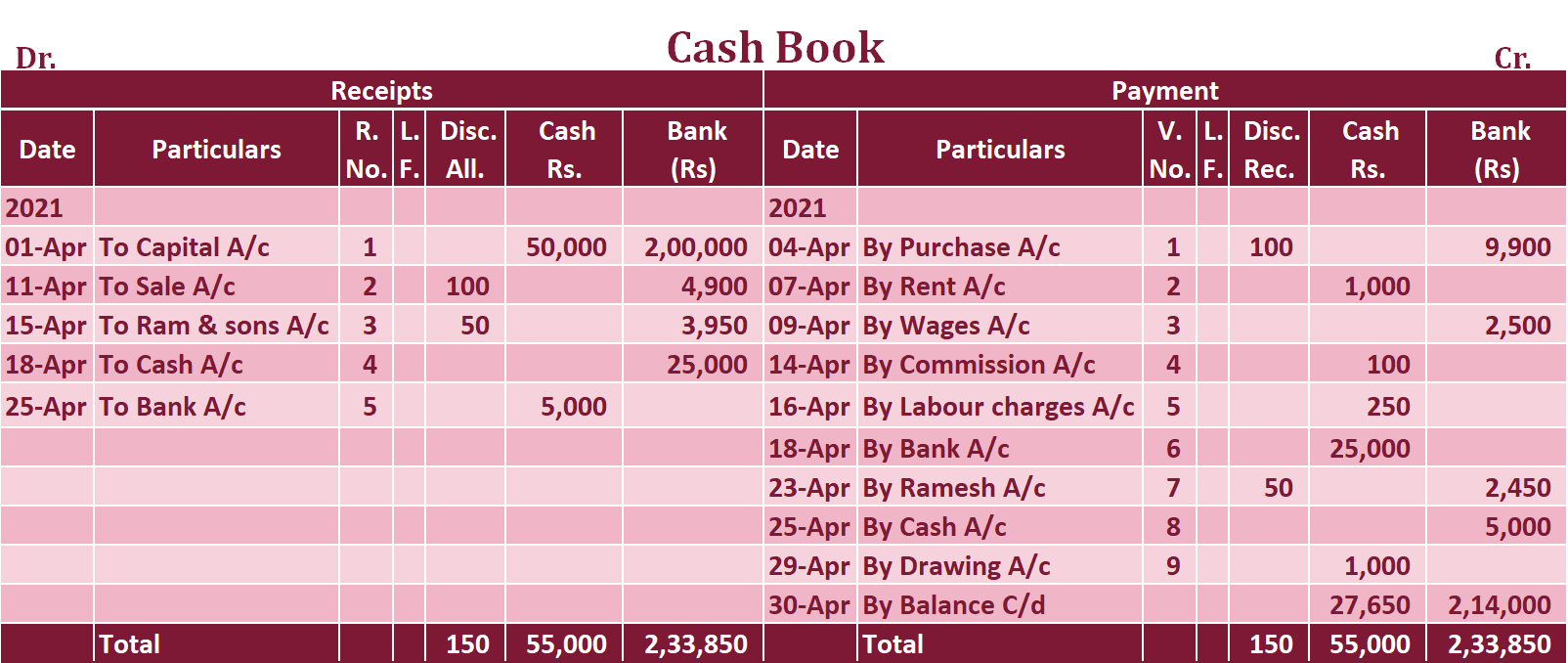

Example of Triple Column Cash Book :

Prepare the triple-column cash book from the following business transactions:

01/04/21 Started a business with cash Rs 50,000/- and bank balance of Rs 2,00,000/-

04/04/21 Goods purchase worth Rs 10,000/- and payment made immediately By cheque and get discount Rs 100/-

07/04/21 Rent paid for the building Rs 1,000/-

09/04/21 Wages paid for Rs 2,500/- by Cheque

11/04/21 Sold goods worth Rs 5,000/- and to receive payment immediately by cheque and allow discount Rs 100/-

12/04/21 Sold goods to Ram & sons Rs 4,000/-

14/04/21 Commission paid to Rohan Rs 100/-

15/04/21 Payment received from Ram & Sons Rs 3,950 by cheque. and allowed them a discount of Rs 50/-

16/04/21 Labour charges paid for Rs 250/-

18/04/21 Cash deposited into Bank Rs 25,000/-

21/04/21 Purchased goods worth Rs 2,500/- from Ramesh.

23/04/21 Payment made to Ramesh Rs 2,450 by Cheque and received the discount of Rs. 50/-

25/04/21 Cash withdrawal from Bank for office use Rs 5,000/-.

29/04/21 An owner withdraw cash from the business for personal use of Rs1,000.

Solution: -

Example of Triple Column Cash BookNote: -Transaction Dated 12/04/17 & 21/04/17 are not recorded in the cash book because these are credit business transactions.If you have any questions about this topic of Triple Column Cash Book please ask it in the comment section below.Thanks

Check out Financial Accounting Books@ Amazon. in

👤

Author & Educator

Sarbjit SinghB.Com and M.Com

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

❓ Frequently Asked Questions

What does "Triple Column Cash Book | Explained with Example" cover?

In Cashbook, we will record the all-cash transaction of the business. This book keeps a record of all cash payments and cash receipts. In this article, we will…

Who is this guide meant for?

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Can I test myself on "Triple Column Cash Book | Explained with Example"?

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

Sir ,if total amnt is 5000 and discount allowed is 100 how should we post this amnt .whether 4900 or 5000.

S

Sarbjit Singh

14 October 2021

Okay,

I think you are confused about the following transaction:

"11/04/21 Sold goods worth Rs 5,000/- and to receive payment immediately by cheque and allow discount Rs 100/-"

In the above transaction the goods worth Rs 5,000 were sold but the amount received in cash after discount is Rs 4,900, and in the cash book we have to record the amount which the business received not the total due amount.

So that's why we have recorded only 4,900 in the bank column and Rs. 100 in the discount column,

K

Kanya

3 April 2022

Shall i know why have we recorded that 4900 in the bank coloum?

A

Amanpreet Kaur

8 April 2022

Because in the transaction method of payment is given. The payment has been made with a cheque.

11/04/21 Sold goods worth Rs 5,000/- and to receive payment immediately by cheque and allow discount of Rs 100/-

M

Ms. Shamalka Thilakarathne

27 April 2022

If there is a transaction as bought a motor vehicle in cash for 300,000 ( not for the business use)

and paid motor expenses in cash 50,000, how do we report them in the cash book?

A

Amanpreet Kaur

4 May 2022

If it is not for business use it means that will be for owner's personal use.

So,

The both amount will be debited to Drawing account

E

Elugbindin Dorcas

18 July 2022

Yes very confused 😖

A

Amanpreet Kaur

14 August 2022

what happens?

You can check our video lecture of triple column Cash Book by clicking on following link:

https://youtu.be/Djr_akOJIFg

L

Lilian mugo

1 November 2022

When you are given a question of opened a bank account and deposited 40000 in the middle of the month how do you go about it

A

Amanpreet Kaur

8 January 2023

It's simple just record contra entry.

1st record it in the debit side of the Bank account.

and then record it in the credit side of the cash account.

T

Tosin

11 May 2023

I don't understand how u got 4,900,when he sold goods of 5000 and immediately received payment by cheque with a discount of 100

O

Ologun ayomide

4 June 2023

Received cash of 800 in full settlement account of 850

A

Amanpreet Kaur

5 June 2023

Thanks for question.

Please write 800 in the Cash column and Rs50 will be written in the discount allowed column.

A

Amanpreet Kaur

5 June 2023

okay let me explain it more:

In the transaction, the amount of payment received is not given so we have to calculate it.

So now the question is how we can calculate it.

we can calculate it with simple formula i.e

Amount received = Amount due/Sale value - the amount of discount.

so,

Amount received = 5,000 - 100

4,900/-

s

suhani

2 November 2024

i am confused about last entry because drawings are recorded in bank column in credit side .

A

Amanpreet Kaur

11 November 2024

Cash is withdrawal from the business is means drawing out of business cash not from bank account. So thats why it is posted on credit side of business cash account.

The Columns of the Triple Column Cash Book are explained Below:-

The Columns of the Triple Column Cash Book are explained Below:-