Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

At the time of receiving payment in the bank without the information of the sender or payer then we will post this transaction into the suspense account till we did not get to know the name of the sender or payer or customer or trade receivable.

For Example: - Date 01/11/2018, The bank statement shows the credit entry of Rs 15,000/- But in narration name of the sender or payer not mention. Solution: - In this case, we open a suspense account and posted the journal entry with the help of it. This process is shown below: -| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 01/11/2018 | Bank A/c | Dr. | 15,000 | ||

| To Suspense a/c | 15,000 | ||||

| (Being the payment received in the bank but the sender name was not clear. So, transferred to Suspense a/c) | |||||

| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 01/11/2018 | Suspense A/c | Dr. | 15,000 | ||

| To M/s A&b Co. Ltd. a/c | 15,000 | ||||

| (Being the name of the customer is got now, so amount transferred to the original linked account) | |||||

The total of both sides of the trial balance is always agreed or matched with each other. So, In the case when these have disagreed, we will prepare new accounts named suspense account and the amount of difference will be posted into it and it will be shown on the shorter side of the trial balance.

| Particulars | L.F. | Debit | Credit |

|---|---|---|---|

| Capital | 10,00,000 | ||

| Cash | 25,000 | ||

| Bank | 3,25,000 | ||

| Furniture | 150,000 | ||

| Land and Building | 10,00,000 | ||

| The loan from Mr. A | 5,00,000 | ||

| Salary | 2,00,000 | ||

| Wages | 1,00,000 | ||

| Purchases | 10,00,000 | ||

| Sales | 15,00,000 | ||

| 28,00,000 | 30,00,000 |

Trial Balance of Ms. Ram and sons as on 31/03/18

| Particulars | L.F. | Debit | Credit |

|---|---|---|---|

| Capital a/c | 10,00,000 | ||

| Cash a/c | 25,000 | ||

| Bank a/c | 3,25,000 | ||

| Furniture a/c | 150,000 | ||

| Land and Building a/c | 10,00,000 | ||

| The loan from Mr. A a/c | 5,00,000 | ||

| Salary a/c | 2,00,000 | ||

| Wages a/c | 1,00,000 | ||

| Purchases a/c | 10,00,000 | ||

| Sales a/c | 15,00,000 | ||

| Suspense a/c | 2,00,000 | ||

| 30,00,000 | 30,00,000 |

In some time, An data entry operator did not understand the actual business transaction, in that case, he will open a suspense account and record this transaction into it. The benefit in the recording in the suspense account is that when an accountant finalizes the books of account first all he will clear the all pending transaction in the suspense account. So if he posted it in the wrong account then there will chance of error which will be located after the audit process or if he did not record it then there is a chance of missing the voucher for the transaction.

For Example: - Date 01/11/2018, The owner paid Rs 10,000/- to an employee along with the salary. Solution: - In this case, The data entry operator did not know how to treat this amount. He is confused in that, will be treated this amount as part of the salary or treated separately. So, for the time being, he records this amount in the suspense account shown as follows: -| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 01/11/2018 | Suspense A/c | Dr. | 15,000 | ||

| To Bank a/c | 15,000 | ||||

| (Being the payment made to the employee but the name of the account is not clear, So, recorded in the suspense a/c) | |||||

| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 01/11/2018 | Commission on turnover A/c | Dr. | 15,000 | ||

| To Suspense a/c | 15,000 | ||||

| (Being the name of the expense account is clear. So, an amount is transferred to the original account) | |||||

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

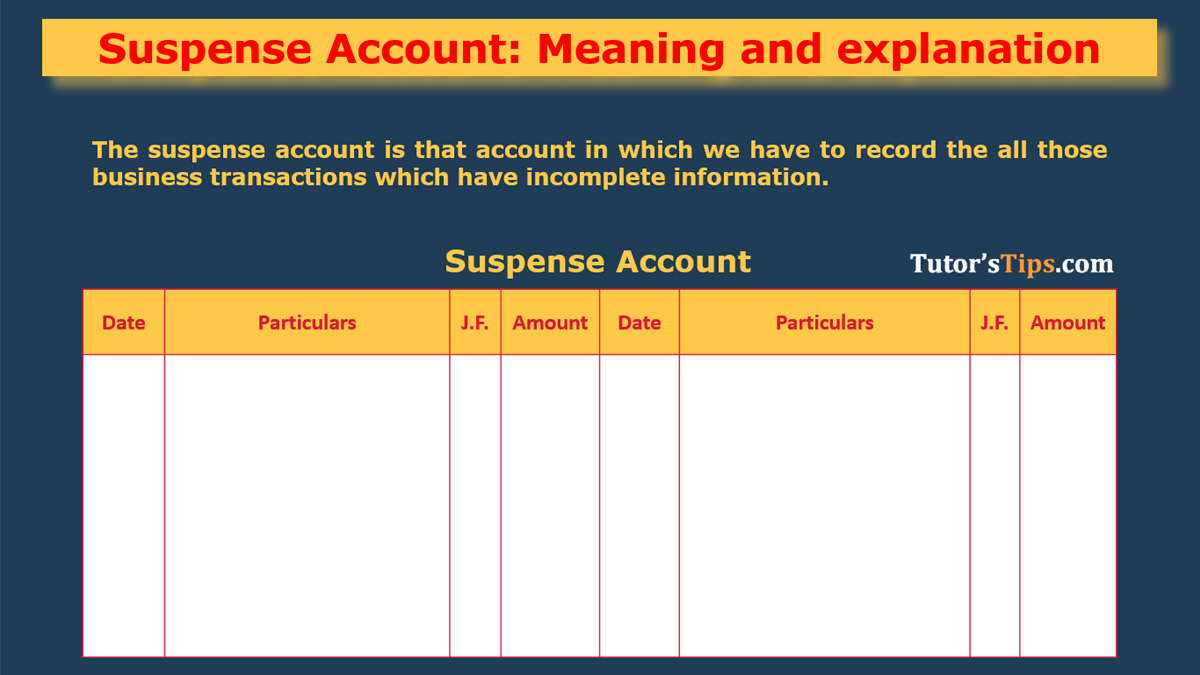

Suspense Account: - The suspense a/c is that account in which we have to record all those business transactions which have incomplete information. Sometimes,…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

7 October 2020

30 September 2021

5 October 2021