Today we are covering the Technical topic of Error Rectification. So please read it very carefully and in this article, you will learn the meaning of the Error, Types of Errors, and ways of Error Rectification, and understand it in much better ways with examples.

Error Rectification in Accounting:-

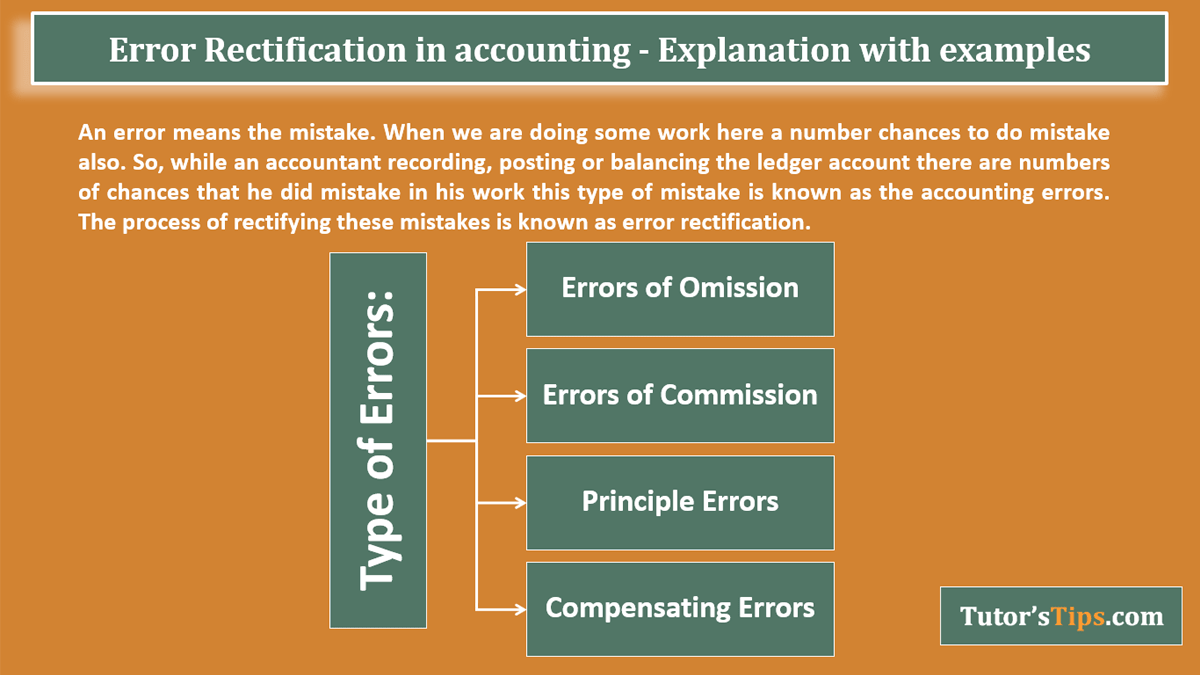

An error means a mistake. When we are doing some work there are several chances to make mistakes also. So, while an accountant records, posts or balances the ledger account there are several chances that he made a mistake in his work this type of mistake is known as accounting errors. The process of rectifying these mistakes is known as

error rectification.

The trial balance is prepared to check the arithmetical accuracy of recording the transactions in the journal, posting to the ledger and balancing of ledger accounts. When the trial balance is agreed then it is assumed that the process of journalizing, posting and balancing has no error. If the trial balance is not agreed then it means there are errors in any above-said processes and efforts are made to detect an error.

However, the agreement of the trial balance is not proof of all error-free accounting there are some types of errors which will not affect the total trial balance. For example, Non-recording of the whole transactions in the books, will not affect the total of the trial balance because we recorded neither debit nor credit. So, we can divide all errors into two main headings, i) Errors which are revealed by the trial balance and, ii) Errors which are not revealed by the trial balance.

Type of Errors: -

In the books of accounts, errors may occur at any stage like journalizing, posting, balancing and preparation of trial balance. So, all the errors, whether affecting trial balance or not, are classified based on their nature into the following four categories:-

- Errors of Omission

- Errors of Commission

- Principle Errors

- Compensating Errors

1. Errors of Omission:-

When the transaction is not recorded in the original entry books or not posted into the ledger account is known as an error of omission. An error of omission can be divided into two types i.e. Completely omitted or Partially omitted.

- Completely omitted: - Those transactions which are completely omitted to record in the books of original entry and thus cannot be posted in the ledger account. These types of errors do not affect the agreement of trial balance. For example, goods purchased from Mr A on credit but not recorded in the purchase book. So, it will also not be posted into the ledger account and not shown in the trial balance whole.

- Partial Omitted:- Those transactions which are recorded partial in the books of accounts are known as an error of partial omission. In other words, every transaction involves a minimum of two accounts, So, if an accountant fails to post the transaction into the one ledger account and posts it in another one account this is known as an error of partial omission. These types of errors do affect the agreement of trial balance. Example: - Goods sold to Mr B posted in the sales account but not posted in Mr B's account then the wrong balance of Mr B's account will be transferred to the trial balance.

2. Errors of Commission: -

An error of commission incurred due to the wrong recording of financial transactions in the books of accounts. Like wrong totalling or balance of ledger accounts, wrong posting into the ledger account, the wrong amount carry forward and over or under-casting the balance of an account. These types of errors can be divided into the following types: -

- Recording Error: - When an accountant records a transaction with the wrong amount in the original entry book. For Example - The salary was paid to the Employee for Rs 10,000/-, But recorded in the cash account and Salary account for Rs 1000/- These types of did not affect the agreement of trial balance.

- Ledger Balancing Error: - These types of errors arise due to the wrong balancing of some ledger accounts. These types of errors affect the agreement of trial balance. For Example - The balance of the furniture and fixture account was taken more than Rs 1000/-, So due to this error the debit side of the trial balance will also be in excess by Rs 1,000/-.

- Posting Error: - These errors arise when the correct transaction is recorded in the original entry book but wrongly posting the ledger account. It may be divided into the following type

- Posted with the incorrect amount on the correct side of the ledger,

- Posted with the correct amount on the incorrect side of the ledger.

- The incorrect amount was posted in the incorrect ledger account but on the correct side.

- The correct amount was posted in the incorrect ledger.

- Posting twice in the ledger account.

- An error of Carrying forward the wrong balance: - This error occurs when an accountant carries forward the wrong balance of the ledger account into the next year or in the trial balance. These types of errors will affect the agreement of the trial balance.

3. Principle Errors: -

The Errors of principle mean the violation of the GAAP(generally accepted accounting principles) viz incorrect allocation of expenditure or income between capital and revenue Expenditure or income. it is worth mentioning the proper allocation between these two items is very important in the sense that improper allocation would lead to wrong and misleading results through financial statements. This type of error will show the undervalued or overvalued assets, expenses, liabilities, or income in the trial balance. it can be a dividend in the following two types

- Treating Capital items as the revenue item

- Treating Revenue item as a capital item.

4. Compensating Error: -

When two or more errors are raised in such a way that the effect of one error is compensated by the effect of another, is known as compensating error. These errors do not affect the agreement of trial balance.

For Example - A sum of Rs 1000 was paid to Mr A on 01/01/18 but recorded in the books of account of Mr A for Rs 100/-. So, the effect of this error will be shown in the trial balance as less total debit side by Rs 900/- because the account of Mr A has to be debited. but on 05/01/18 Rs 100 was paid to Mr B but recorded in the books of account of Mr B for Rs 1000/- SO, the effect of this error will be shown in the trial balance as excess in the total of debit side by Rs 900/- because an account of Mr B has to credit. So, in the end, these errors compensate each other.

Error Rectification: -

So far we discussed various types of accounting Errors and now we will discuss the rectification of these errors.

We can broadly divide the type of errors into two categories i.e.

- An error that did not affect the agreement (totalling) of the trial balance.

- An error that affects the agreement (totalling) of the trial balance.

1. An error that did not affect the agreement (totalling) of the trial balance.

These errors are also known as two side errors. It includes the following types of errors

- The error of Complete omission of the transaction

- Wrong recording of the books of original entry.

- The error of recording the correct amount but in the wrong account.

- Principle Errors

- Compensating Errors.

Error Rectification process: -

The process of rectification included the following steps: -

- What has been done?

- What was to be done?

- What action should be taken for rectification?

We will rectify it in the three following steps: -

- Recorded entry (i.e. the entry that has been recorded in the books)

- Correct Entry (i.e the entry which has to be recorded in the books)

- Rectification Entry

For Example: -

Goods sold to Mr A for Rs 1000 but recorded in the Purchase book.

Solution: -

This is an error of wrong recording in the original entry books.

Entry recorded in the books of accounts: -

It is an incorrect entry because the transaction of sales accounts is recorded in the purchase book.

Purchase a/c Dr 1,000

To Mr A a/c 1,000

The corrected entry would be: -

Mr A a/c Dr 1,000

To Sales a/c 1,000

Error Rectification Entry would be: -

So, now we know the correct or incorrect transaction and we will rectify the transaction with the help of a single journal entry.

Mr A a/c Dr 2,000

To Sales a/c 1,000