Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

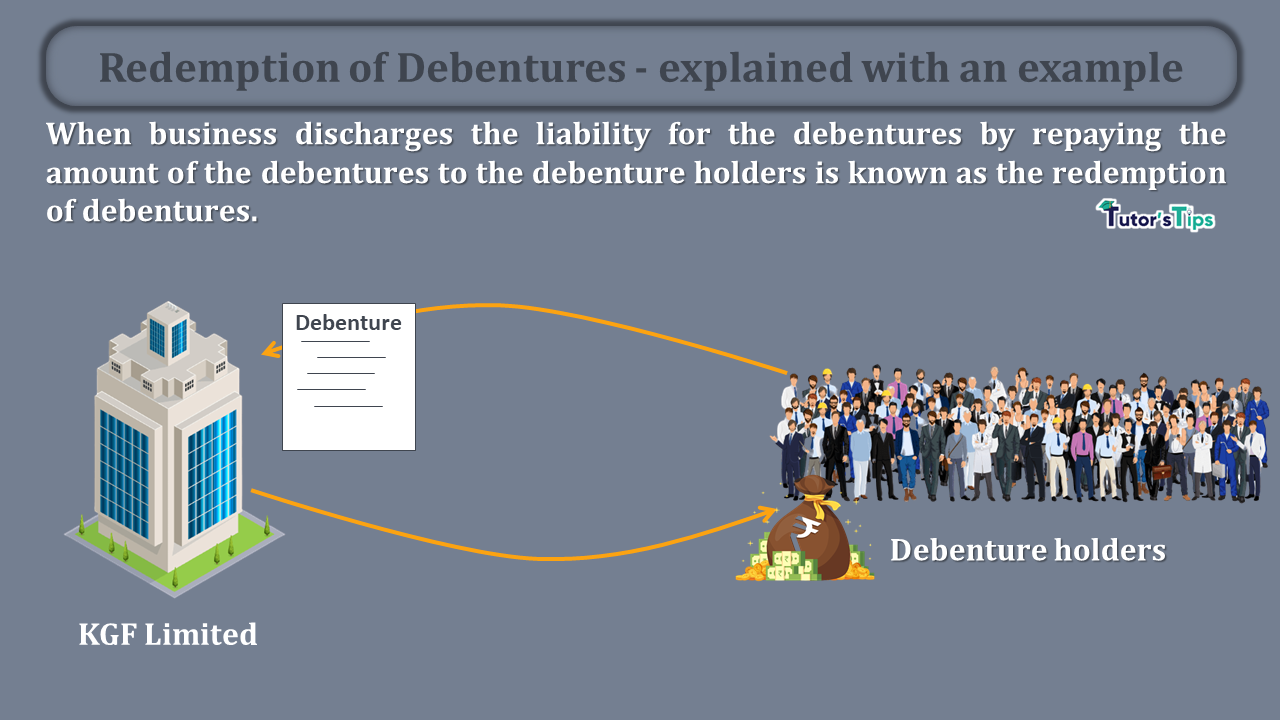

Redemption of Debentures means the repayment of liabilities of debentures after the specific period of time or on the demand of the company.

When business discharges the liability for the debentures by repaying the amount of the debentures to the debenture holders is known as the redemption of the debenture.

Mainly the debentures always repaid after a fixed period time which is decided before issuing of debentures. The date of redemption has predefined in the terms of issue of debentures. But the debentures can be redeemed in instalments by drawing lots or by purchase from the open market before the actual date of redemption.

After the purchase from the market, The debentures can be cancelled or converted into equity shares.

ABK Limited issued 12,000 Debentures @ 100 on 01/01/2019 which are redeemable after 5 years. But the company want to redeem the debenture before the actual date of redemption. Provide the solution to the company how they can redeem the debentures before the actual redemption date in three years started from 01/01/2020.

There is the company can redeem debenture in three equal instalments by drawing lots or by purchasing these from the open market and then cancel them.

Calculation of the amount of instalment:

Amount of Instalment = Number of debentures/number of years

Number of debentures = 12000

Number of Years = 3 years

Amount of Instalment = 12,000 / 3

= 4,000/-

So, If the company buy 4,000 number of debentures from the open market every year at market price then they can successfully redeem all debentures.

You have to remember the following point at the time of redemption to redeem debentures correctly:

The debentures are mainly redeemed at the predefined time of the redemption. But in some cases, it can be bought from the open market.

Amount payable will depends on the predefined terms and condition of issue of the debentures i.e. at par, or at a premium. These conditions are already explained. so you can check it from the following link:

https://tutorstips.com/issue-of-debentures-from-the-point-of-view-of-redemption/

The funds utilized to redeem the debenture have to decide first. These are the following way:

The redemption out of capital means there will be no need to create debentures redemption reserve because the funds utilize out of capital not from the surplus or profit of the business.

But the redemption only out of capital is not possible under the present instruction of the companies Act, 2013 except some the business which is specified under the law.

Out of Profit means the debenture will be redeemed from the balance of surplus or profit account. The 100% value equal to the nominal value of the debentures will be transferred from the surplus account to the Debenture redemption reserves.

In this method of the debentures will be redeemed out of the profit and partially out of capital. This is the best method to redeem the debentures for the source of the funds.

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Redemption of Debentures means the repayment of liabilities of debentures after the specific period of time or on the demand of the company. What is Redemption…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.