Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

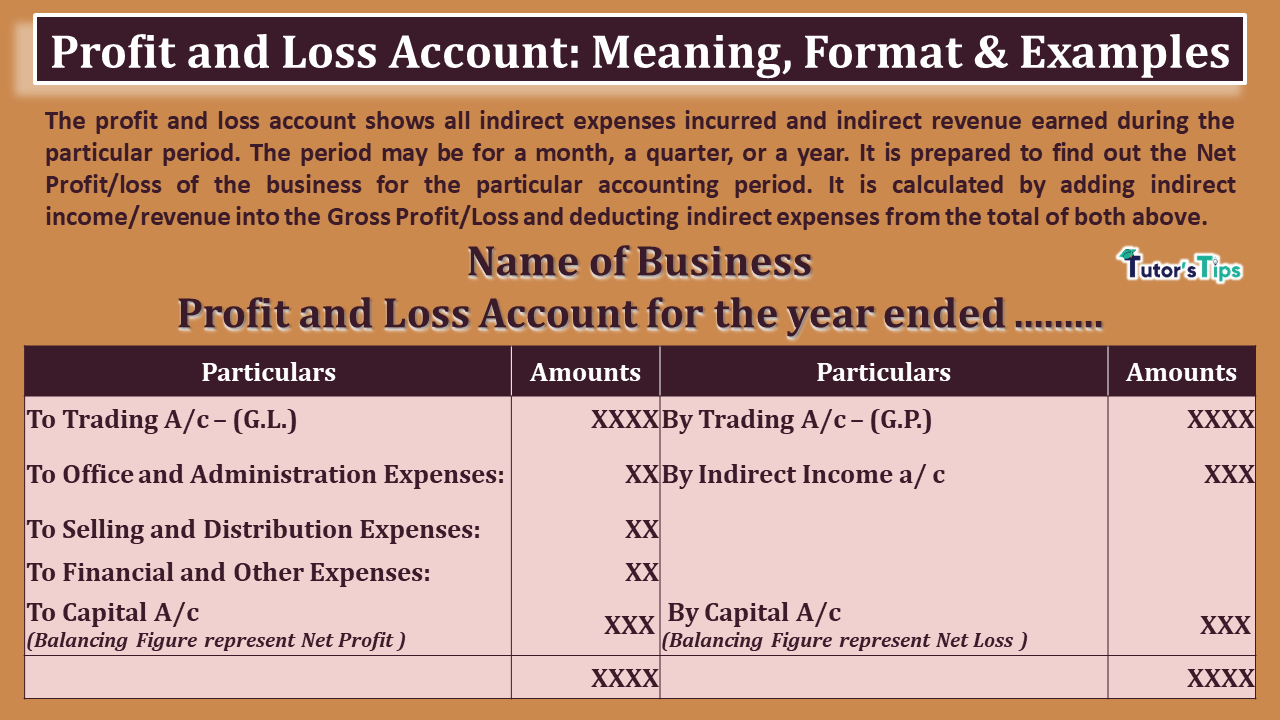

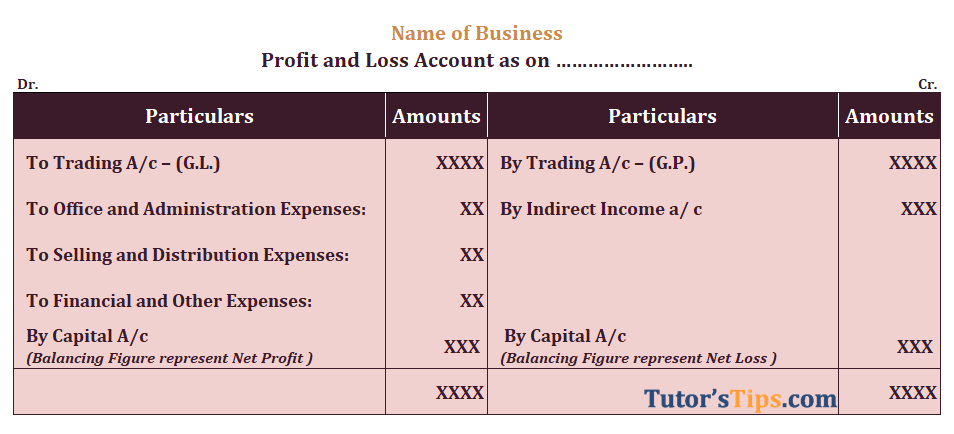

Today we are covering the Technical topic of the Profit and Loss account. So please read it very consciously and in this article, you will learn the meaning of the Profit and Loss Account, Feature, Needs, Format, and understand it in much better ways with examples.

The profit and loss account shows all indirect expenses incurred and indirect revenue earned during the particular period. The period may be for a month, a quarter, or a year. It is prepared to find out the Net Profit/loss of the business for the particular accounting period. It is calculated by adding indirect income/revenue into the Gross Profit/Loss and deducting indirect expenses from the total of both above.

Net Profit/Loss = Gross Profit/Loss + Indirect Income - Indirect Expenses

We need the Profit and Loss account to ascertain the Net profit for the year.

The P&L account helps us to calculate the NP ratio by providing us with Net Profit/Loss. (NP Ratio = Net Profit / Net sale)

It helps in determining the trend of indirect expenses and indirect income. With the help of tread, top management takes the future decision for making targets and policies.

in this account, all indirect expenses related to the business enterprise shall be incorporated. It has been seen that in many business enterprises, indirect expenses cover more than 75% of the total expenses, So proper watch on these expenses is most for effective control of expenses.

Through a comparison of the profit and Loss a/c of two different years, we will get the actual trend of our indirect expenses.

This account is the basis of the balance sheet. The result of the profit and loss account was transferred to the Balance sheet. So, in the absence of a Profit and Loss account, we cannot prepare a balance sheet.

For preparing a Profit and Loss Account, we have to close the ledger of indirect expenses or indirect income. For this we have to post the following closing journal entries in the Journal Proper: -

P&L A/c Dr.

To Accounts in Group head - Office and Administrative Expenses.

To Accounts in Group head - Selling and Distribution Expenses

To Accounts in Group head - Financial Expenses.

To Accounts in Group head - Maintenance Expenses.

To Accounts in Group head - Abnormal Losses

(Being all indirect expenses transferred to P&L Account)

The accounts in Group head - Other Income Dr.

The accounts in Group head - Non-trading Income Dr.

The accounts in Group head - Abnormal Gains

To P&L Account

(Being indirect Income transferred to P&L Account)

(i) In the case of Net Profit

P&L A/c Dr.

To Capital Account

(Being Net profit transferred to Capital account )

OR

P&L A/c Dr.

To P&L Appropriation Account

(Being Net profit transferred to profit/loss appropriation account )

(i) In the case of Gross loss

Capital Account Dr.

To P&L A/c

(Being Net loss transferred to Capital account )

Note: -

if the total of Credit side excess over Debit side = Net Profit

if the total of Debit side excess over Credit side = Net Loss

Prepare Profit and Loss account for the year ending March 31, 2018, in the books of Tutorstips Ltd. from the following balances as of March 31, 2018.

| Gross Profit | 1,000,000 |

| Salaries | 144,000 |

| Commission received | 25,000 |

| Interest charges by bank | 5,000 |

| Freight outwards | 7,000 |

| Printing & Stationery | 5,000 |

| Interest on loan | 3,500 |

| Travelling Expenses | 15,000 |

| Advertisement Expenses | 7,200 |

| Rent Received | 10,000 |

| Legal Charges | 5,000 |

| Postage and telegram | 1,200 |

| Insurance | 10,000 |

| Loss on sale of Machinery | 700 |

| Gain on sale of Furniture | 500 |

| Depreciation on Fixed Assets | 10,000 |

Also, show the closing entries.

TutorsTips Ltd.

Journal book

| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| P&L A/c | Dr. | 2,13,600 | |||

| To Salaries | 1,44,000 | ||||

| To Interest charges by bank | 5,000 | ||||

| To Freight outwards | 7,000 | ||||

| To Printing & Stationery | 5,000 | ||||

| To Interest on a loan | 3,500 | ||||

| To Travelling Expenses | 15,000 | ||||

| To Advertisement Expenses | 7,200 | ||||

| To Legal Charges | 5,000 | ||||

| To Postage and telegram | 1,200 | ||||

| To Insurance | 10,000 | ||||

| To loss on the sale of Machinery | 700 | ||||

| To Depreciation on Fixed Assets | 10,000 | ||||

| (Being all indirect expenses transferred to P&L Account) | |||||

| Commission received | Dr. | 25,000 | |||

| Rent Received | Dr. | 10,000 | |||

| Gain on sale of Furniture | Dr. | 500 | |||

| To P&L A/c | 35,500 | ||||

| (Being indirect Income transferred to P&l Account) | |||||

| P&L A/c | Dr. | 8,21,900 | |||

| To Capital Account | 8,21,900 | ||||

| (Being Net profit transferred to Capital account ) |

TutorsTips Ltd.

Profit and Loss Account for the year ended March 31 2018

| Particulars | Amounts | Particulars | Amounts |

|---|---|---|---|

| To Salaries A/c | 1,44,000 | By Trading A/c – (G.P.) | 10,00,000 |

| To Interest charges by bank A/c | 5,000 | By Commission received A/c | 25,000 |

| To Freight outwards A/c | 7,000 | By Rent Received A/c | 10,000 |

| To Printing & Stationery A/c | 5,000 | By Gain on sale of Furniture A/c | 500 |

| To Interest on the loan A/c | 3,500 | ||

| To Travelling Expenses A/c | 15,000 | ||

| To Advertisement Expenses A/c | 7,200 | ||

| To Legal Charges A/c | 5,000 | ||

| To Postage and telegram A/c | 1,200 | ||

| To Insurance A/c | 10,000 | ||

| To loss on the sale of Machinery A/c | 700 | ||

| To Depreciation on Fixed Assets A/c | 10,000 | ||

| To Capital A/c (Balancing Figure represent Net Profit ) |

8,21,900 | ||

| 10,35,500 | 10,35,500 |

Or

If you want to download the above illustration please download the following image:

Prepare Profit and Loss account for the year ending March 31, 2018, in the books of Aman Enterprise Ltd. from the following balances for the year ended March 31 2018.

| Gross loss | 50,000 |

| Salaries | 94,000 |

| Commission received | 5,000 |

| Interest charges by bank | 2,000 |

| Freight outwards | 15,000 |

| Printing & Stationery | 7,000 |

| Interest on loan | 5,500 |

| Travelling Expenses | 10,000 |

| Advertisement Expenses | 10,200 |

| Rent Received | 50,000 |

| Legal Charges | 3,000 |

| Postage and telegram | 2,200 |

| Insurance | 10,000 |

| Loss on sale of Machinery | 700 |

| Gain on sale of Furniture | 2,500 |

| Depreciation on Fixed Assets | 15,000 |

Also, show the closing entries.

Firstly solve it by yourself then saw the solution.

Solution: -

Aman Enterprise Ltd.

Journal book

| Date | Particulars | L.F. | Debit | Credit |

|---|---|---|---|---|

| P&L A/c Dr. | 1,64,600 | |||

| To salaries | 94,000 | |||

| To interest charges by bank | 2,000 | |||

| To Freight outwards | 15,000 | |||

| To Printing & Stationery | 7,000 | |||

| To Interest on the loan | 5,500 | |||

| To Travelling Expenses | 10,000 | |||

| To Advertisement Expenses | 10,200 | |||

| To Legal Charges | 5,000 | |||

| To Postage and telegram | 3,000 | |||

| To Insurance | 2,200 | |||

| To loss on the sale of Machinery | 10,000 | |||

| To Depreciation on Fixed Assets | 700 | |||

| (Being all indirect expenses transferred to P&L Account) | ||||

| Commission received Dr. | 35,000 | |||

| Rent Received Dr. | 50,000 | |||

| Gain on sale of Furniture Dr. | 2,500 | |||

| To P&L A/c | 87,500 | |||

| (Being indirect Income transferred to P&l Account) | ||||

| Capital Account Dr. | 1,27,100 | |||

| To P&L A/c | 1,27,100 | |||

| (Being Net Loss transferred to Capital account ) |

Aman Enterprise Ltd.

Profit and Loss Account for the year ended March 31 2018

| Particulars | Amounts | Particulars | Amounts |

|---|---|---|---|

| To Trading A/c – (G.L.) | 50,000 | By Commission received | 35,000 |

| To salaries | 94,000 | By Rent Received | 50,000 |

| To interest charges by bank | 2,000 | By Gain on sale of Furniture | 2,500 |

| To Freight outwards | 15,000 | By Capital A/c (Balancing Figure represent Net Loss ) |

1,27,100 |

| To Printing & Stationery | 7,000 | ||

| To Interest on the loan | 5,500 | ||

| To Travelling Expenses | 10,000 | ||

| To Advertisement Expenses | 10,200 | ||

| To Legal Charges | 5,000 | ||

| To Postage and telegram | 3,000 | ||

| To Insurance | 2,200 | ||

| To loss on the sale of Machinery | 10,000 | ||

| To Depreciation on Fixed Assets | 700 | ||

| 2,14,600 | 2,14,600 |

Or

If you want to download the above illustration please download the following image:

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Today we are covering the Technical topic of the Profit and Loss account. So please read it very consciously and in this article, you will learn the meaning of…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

27 January 2021

9 January 2022

19 January 2022