Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

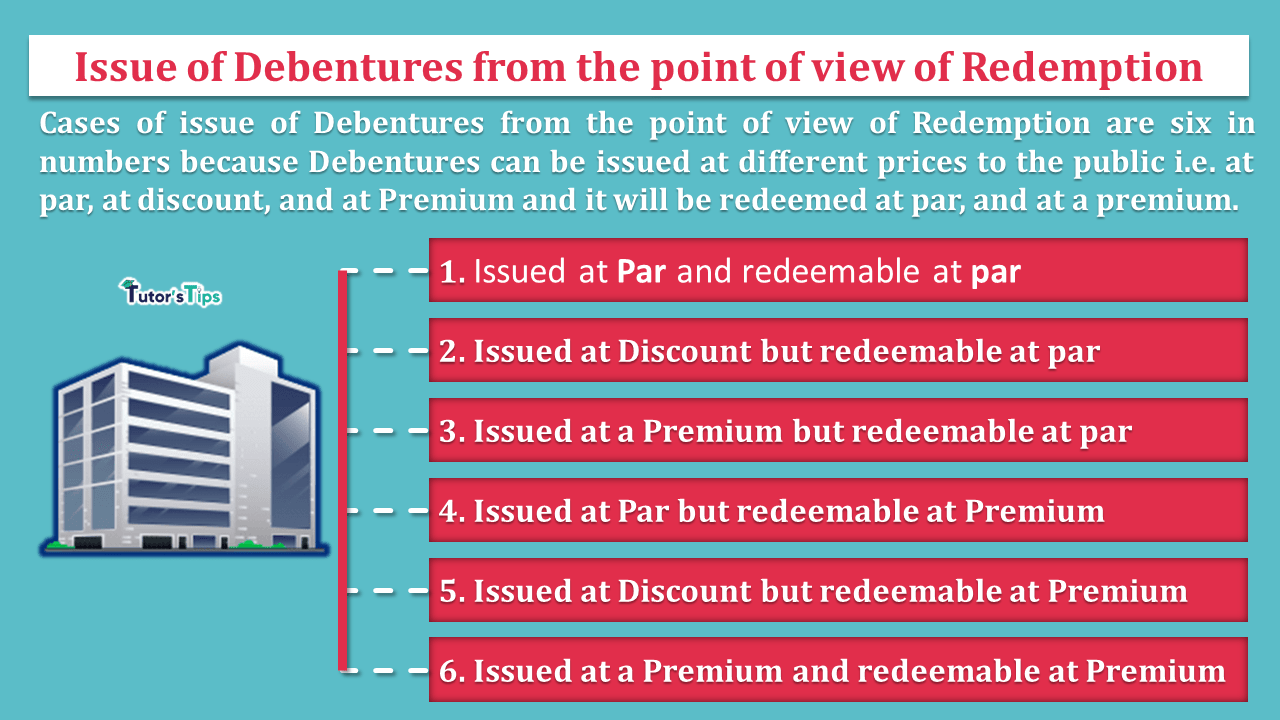

Cases of issue of Debentures from the point of view of Redemption are six in numbers because Debentures can be issued at different prices to the public i.e. at par, at discount, and at Premium and it will be redeemed at par, and at a premium. The accounting treatment of the all will be different as we have explained in this article.

There is six number of case of issue of debentures form the point of view of redemption which is shown as follows:

It means that the debentures are issued at the face(nominal) value of the debentures and also redeemable on the same value. Therefore the company not incurring any loss at the time of redemption of the debentures. The accounting treatment will be followed in this case is shown as following:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| To ___% Debentures A/c | ***** | ||||

| (Being Debenture issued at par and redeemable at par) | |||||

It means that the debentures are issued at the value less than the face(nominal) value of the debentures but redeemable on the face(nominal) value of the debentures. Therefore the company not incurring any loss at the time of redemption of the debentures. The accounting treatment will be followed in this case is shown as following:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| Discount on Issue of Deb. A/c | Dr. | *** | |||

| To ___% Debentures A/c | ***** | ||||

| (Being Debenture issued at Discount and redeemable at par) | |||||

It means that the debentures are issued at the value more than the face(nominal) value of the debentures but redeemable on the face(nominal) value of the debentures. Therefore the company not incurring any loss at the time of redemption of the debentures. The accounting treatment will be followed in this case is shown as following:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| To ___% Debentures A/c | ***** | ||||

| To Securities Premium A/c | *** | ||||

| (Being Debenture issued at a premium and redeemable at par) | |||||

It means that the debentures are issued at the face(nominal) value of the debentures but redeemable on the value more than the face(nominal) value of the debentures(at a premium). Therefore the company incurring loss at the time of redemption of the debentures. The accounting treatment will be followed in this case is shown as following:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| Loss on Issue of Deb. A/c | Dr. | *** | |||

| To ___% Debentures A/c | ***** | ||||

| To Premium on Red. of Deb. A/c | *** | ||||

| (Being Debenture issued at par and redeemable at a premium) | |||||

It means that the debentures are issued at the value less than the face(nominal) value of the debentures but redeemable on the value more than the face(nominal) value of the debentures(at a premium). Therefore the company incurring loss at the time of redemption of the debentures. The accounting treatment will be followed in this case is shown as following:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| Discount on Issue of Deb. A/c | Dr. | *** | |||

| Loss on Issue of Deb. A/c | Dr. | *** | |||

| To ___% Debentures A/c | ***** | ||||

| To Premium on Red. of Deb. A/c | *** | ||||

| (Being Debenture issued at par and redeemable at a premium) | |||||

It means that the debentures are issued at the value more than the face(nominal) value of the debentures but redeemable at the value more than the face(nominal) value of the debentures(at a premium). Therefore the company incurring loss at the time of redemption of the debentures. The accounting treatment will be followed in this case is shown as following:

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Bank A/c | Dr. | ***** | |||

| To Debentures App. A/c | ***** | ||||

| (Being Debentures application money received) | |||||

| Debentures Application A/c | Dr. | ***** | |||

| Loss on Issue of Deb. A/c | Dr. | *** | |||

| To ___% Debentures A/c | ***** | ||||

| To Securities Premium A/c | *** | ||||

| To Premium on Red. of Deb. A/c | *** | ||||

| (Being Debenture issued at par and redeemable at a premium) | |||||

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Cases of issue of Debentures from the point of view of Redemption are six in numbers because Debentures can be issued at different prices to the public i.e. at…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

10 April 2022

10 April 2022

18 November 2022

8 January 2023