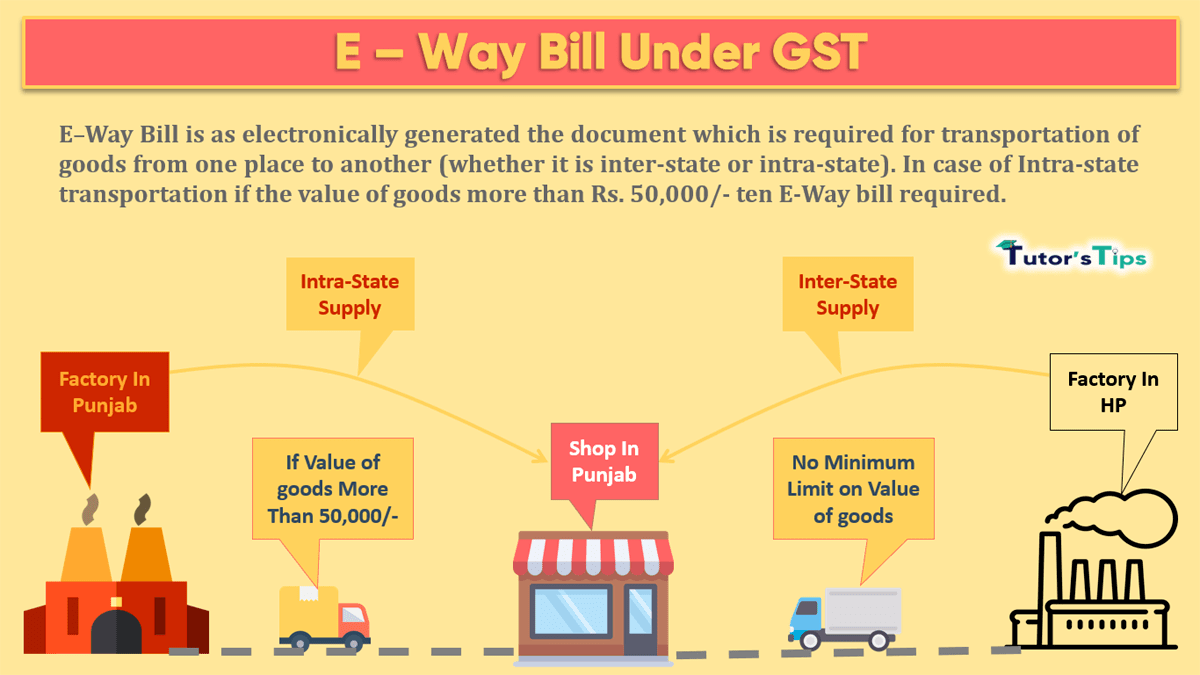

What is E-Way Bill? E–Way Bill is an electronically generated document that is required for transportation of goods from one place to another (whether it is…

Syllabus-aligned study material with detailed definitions, formats, and practical examples.

Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

What is E-Way Bill?

E–Way Bill is an electronically generated document that is required for transportation of goods from one place to another (whether it is inter-state or intra-state) if the value of goods more than Rs. 50,000/-.

Important Point: -

It is the mandatory document from 01/02/2018 for the movement of goods from one place to another.

If the transporter carrying multiple consignments then he needs to generate a consolidated E–Way Bill for all.

If In any case, the transporter needs to transferred goods from one vehicle to another, then he has to generate a new E–Way Bill for a new vehicle.

E–Way Bill can be generated and canceled from GST Portal, app, and by SMS.

When an E–Way Bill is generated a unique E–Way Bill number (EBN) is allocated and is available to the supplier, recipient, and the transporter

For certain specified Goods, the E–Way Bill needs to be generated mandatorily even if the value of the consignment of Goods is less than Rs. 50,000:

Inter-State movement of Goods by the Principal to the Job-worker

Inter-State Transport of Handicraft goods by a dealer exempted from GST registration

Latest Update

As per Official Notification-11/2018 dated 2nd February 2018: Mandatory Implementation of e-Way Bill is now canceled from 1st February 2018.

When E–Way Bill Needed to generate?

E-way-Bill-when-required

When the value of goods more than 50,000/-(either single invoice value is 50,000/- or consolidate of all invoices value which is carrying one vehicle/conveyance)

If goods are transferred in relation to a supply (i.e. sale of goods)

If goods are transferred for a reason other than supply (i.e. Sale Return/Branch transfer)

If goods are supplied by an unregistered dealer to a registered dealer.

What is a supply under E–Way Bill?

Sale - Means transferred goods for some consideration (Payment)

Transfer – if goods transferred from head office to branch

Exchange/Barter – if goods transferred against consideration of other goods from the recipient.

Who needs to generate an E–Way Bill?

E–Way Bill generator chart

Registered Person – E-way bill must be generated when there is a movement of goods of more than Rs 50,000 in value to or from a Registered Person. A Registered person or the transporter may choose to generate and carry an e-way bill even if the value of goods is less than Rs 50,000.

Unregistered Persons – Unregistered persons are also required to generate an e-Way Bill. However, where a supply is made by an unregistered person to a registered person, the receiver will have to ensure all the compliances are met as if they were the supplier.

Transporter – Transporters carrying goods by road, air, rail, etc. also need to generate an e-Way Bill if the supplier has not generated an e-Way Bill.

Note: -

Unregistered Transporters will be issued Transporter ID on enrolling on the e-way bill portal after which e-way bills can be generated.

If a transporter is transporting multiple consignments in a single conveyance, they can use the form GST EWB-02 to produce a consolidated e-way bill, by providing the e-way bill numbers of each consignment.

Part B of the e-Way Bill is not required to be filled where the distance between the consigner or consignee and the transporter is less than 10 Kms and transport is within the same state.

When E-Way Bill is not required

In the following cases, an E-way bill is not required to generate: -

Goods are moved from the port, airport, air cargo complex for clearance by Customs.

The specified goods Transported

The goods are transported by non-motor vehicle

The validity of e-Way Bill

The validity of the e-way bill depends on distance, which will travel by goods from where E-way bill generated. (either from the supplier or the transporter address). Validity starts from the date and time of generation of it.

If you have any question about this topic please ask it in the comment section below: -

Thanks

👤

Author & Educator

Sarbjit SinghB.Com and M.Com

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

❓ Frequently Asked Questions

What does "E–Way Bill under GST" cover?

What is E-Way Bill? E–Way Bill is an electronically generated document that is required for transportation of goods from one place to another (whether it is…

Who is this guide meant for?

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Goods and Services Tax (GST).

Can I test myself on "E–Way Bill under GST"?

Yes — this page includes a short interactive quiz so you can check your understanding straight away.