Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

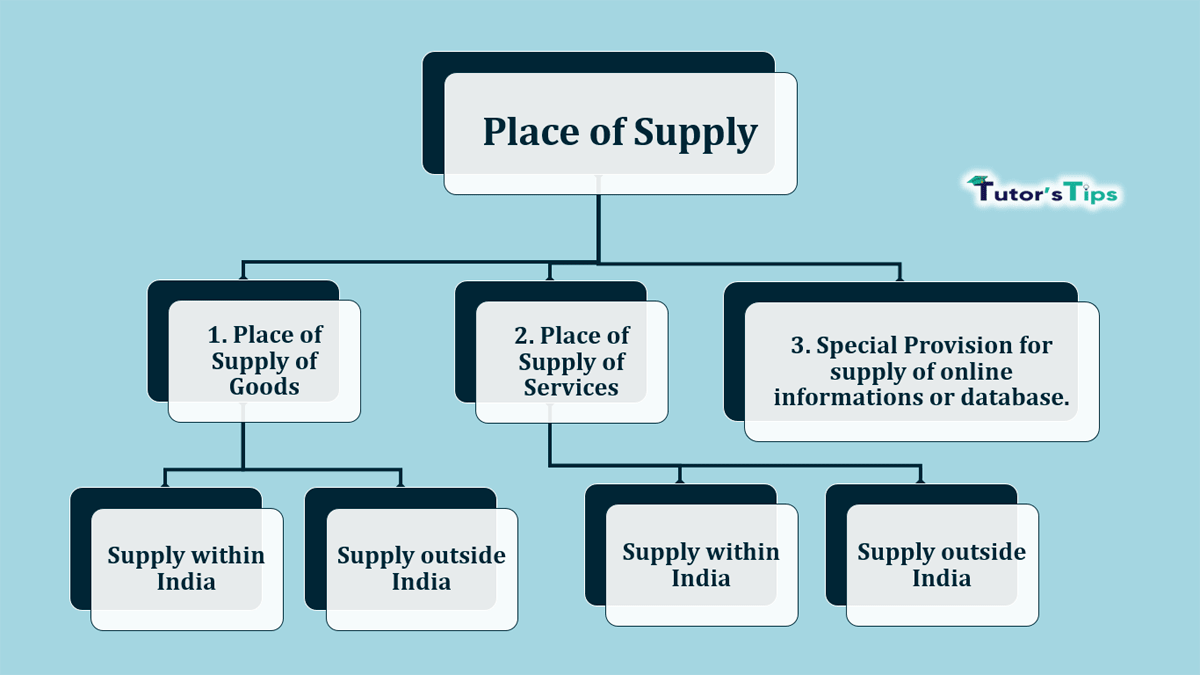

| Section/ Sub Section | Services | Place of Supply of Services |

|---|---|---|

| 12(1) & 12 (2) | All services which are not covered in Subsection 3 to 12 | As explained above in two points |

| 12 (3) | Directly in relation to immovable property like architecture, construction, accommodation, event etc. | The location of such immovable property |

| 12 (4) | Restaurants, catering, grooming health services including cosmetic and plastic surgery | Place where such services are actually performed |

| 12 (5) | Training and performance appraisals | Registered recipient - Place of the recipient. Unregistered Recipient – where the Services are actually performed |

| 12 (6) | Admission to the cultural, artistic event, amusement park etc. | Place where such an event is held or where such park is located |

| 12 (7) | Organizing of cultural, entertainment, conferences, Trade fairs etc. | B2B - Place of Recipient B2C – where the event actually held |

| 12 (8) | Transportation of Goods including mail or courier | B2B - Place of Recipient B2C – where goods are handed over to Transporter |

| 12 (9) | Transportation of Passengers | B2B - Place of Recipient B2C – Place where Passenger embarks on the conveyance of the continuous journey. But Return journey shall be treated as a separate journey. |

| 12 (10) | Services onboard a conveyance | Frist Scheduled point of departure of that conveyance For Example - M/s Kingfisher airline hires a doctor for the passengers travelling from Delhi to Mumbai. In such a case although the services by a doctor have been provided onboard the place of supply shall be Delhi |

| 12 (11) | Telecommunication Services

|

|

| 12 (12) | Banking and Financial Services (Including stock Broking) | Location of the recipient of the services else location of the supplier. |

| 12 (13) | Insurance Services | B2B – Place of Recipient B2C – Location of the recipient of records of the supplier |

| 12 (14) | Advertisement services to Government | Location of the state of advertisement |

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Place of Supply of Services under GST", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Goods and Services Tax (GST).

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Place of Supply of Services under GST" instantly.

27 February 2018