Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

| Basis of Difference | Journal | Ledger |

|---|---|---|

| Meaning | Journal in Accounting is the process of analyzing and recording business transactions in chronological (day-to-day) order. | Ledger is a book of accounts in which we kept all the transactions of a particular account separately. |

| Type | it is the subsidiary book | It is the final book of account. |

| Order of Recording | In the journal, all transactions are recorded in chronological (day-to-day) order. | In the Ledger, the transactions related to a single account(Cash, Bank, etc.) are recorded in chronological (day to day) order in a particular ledger account. |

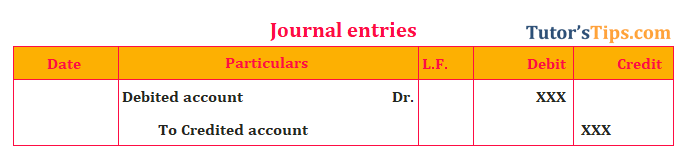

| Name of Process | Journalizing | Posting from journal to ledger. |

| Format | In the format of the journal, debit and credit are two different columns. | In the format of the Ledger, debit and credit are two different sides of an account. |

| Nature of Account | All transactions are recorded in the same book called a journal. | All transactions are posted in the particular ledger account according to the nature of an account. |

| Balance | It is very difficult to know the balance of a particular account. | The ledger is prepared to know the balance of a particular account. |

| Narrations | Journal contains a narration for every transaction | Ledger may or may not contain a narration of every transaction. |

| Also known as | The book of prime or original entry book | The book of second entry and statement of account. |

| Process of Balancing | It does not include the process of balancing. | It includes the process of balancing or closing a ledger account. |

| Financial Statement | We can not prepare financial statement directly from the journal | We can prepare financial statements directly from the ledger but not so easy for larger businesses. |

| Revenue | The Journal not providing any information about the total revenue earned during the year. | In the ledger, we can get to know about the revenue earned during the year from the total Sales accounts. |

| Closing Balances of the Assets | It is very difficult to know the closing balance of the assets at the end of a particular accounting period. | It is very easy to know the closing balance of the assets at the end of a particular accounting period. |

| Folio | Journal contains a ledger folio column. | The ledger contains a journal folio column. |

| Total Columns | Journal contains a total of five columns | The ledger contains a total of eight columns. |

| Sides | It does not have any side. | It has two sides i.e. debit and credit side. |

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Difference between Journal and Ledger", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Differences in financial accounting class 11.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Difference between Journal and Ledger" instantly.