Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

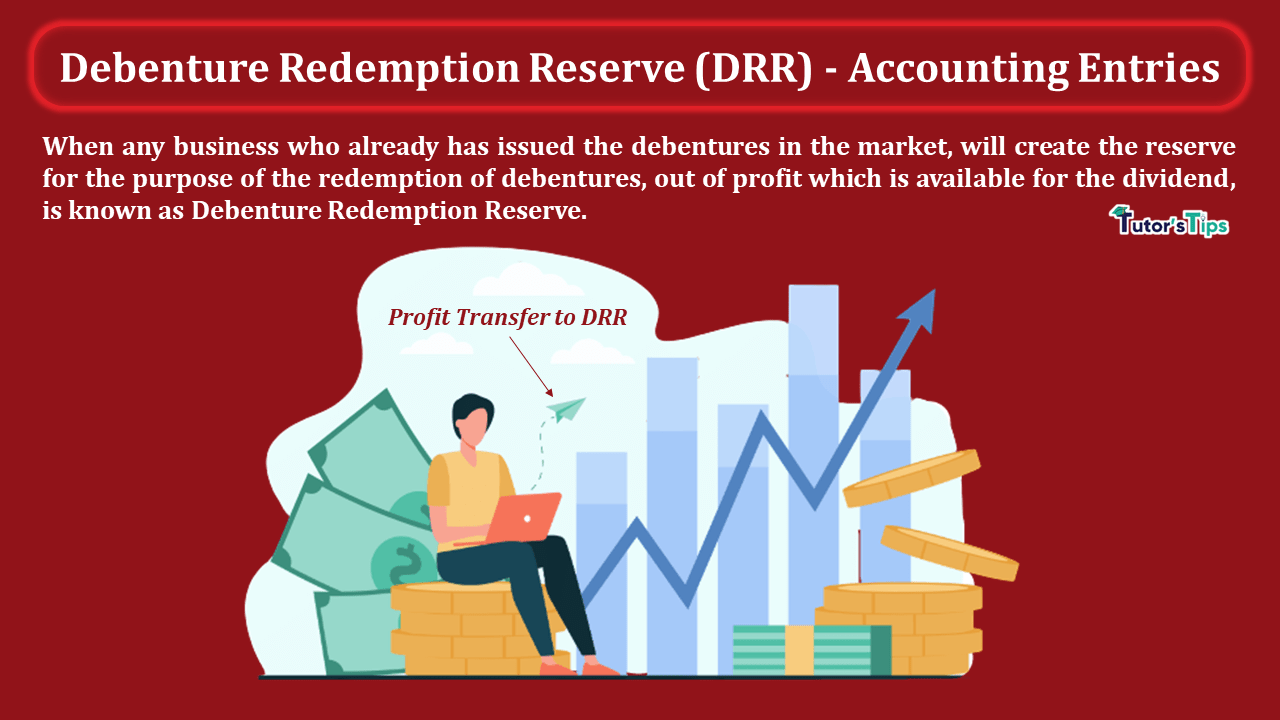

Debenture Redemption Reserve is the type of provision which is created by the company who issued the debentures in the market. This reserve ensuring the investor against the default by the company.

When any business who already has issued the debentures in the market, will create the reserve for the purpose of the redemption of debentures, out of profit which is available for the dividend, is known as Debenture Redemption Reserve. It provides insurance to the debenture holder against any default by the company. It is also known as DRR. It is created before the starting of the process of redemption of the debentures.

The rules regarding the debenture redemption reserve are mention in the act show as below: -

Debenture Redemption Reserve (DRR) is a reserve set aside out of profits available for distribution as a dividend for the purpose of redemption of debentures. The amount transferred to Debentures Redemption Reserve (DRR) Before the process of redemption of debentures begins.

The process of redemption begins with setting aside(creating) Debentures Redemption Reserve (DRR) out of profit available for distribution as dividend. besides the transferred of the amount to DRR, Rule 18(7)(c) of companies (Share Capital and Debentures) Rules, 2014 prescribes that the company required to create DRR shall invest the amount in securities specified.

The Companies Act, 2013 Together with Rule 18(7)(b) of the Companies (Share Capital and Debentures) Rules, 2014 exempts following classes or kinds of companies from creating DRR:

Besides, DRR is not created on fully convertible debentures. and where the debentures are partly convertible, DRR is created only on the non-convertible part of debentures.

[Rule 18(7)(d) of the Companies (Share Capital and Debentures) Rules, 2014]

The Companies Act, 2013 [Section 71940] prescribes that

Rule 18(7)(b) of Companies (Share Capital and Debentures) Rules, 2014 prescribes that company shall transfer at least 25 per cent of the nominal (face) value of the outstanding debentures to DRR.

In case, Debentures are redeemed out of profits only, DRR is created by transferring an amount that is equal to 100 per cent of the nominal(face) value of the total outstanding debentures.

Note for students: -

If in case, the question is silent about the percentage or amount of the DRR then you have to transfer the amount equal to the 25% of the nominal (face) value of the outstanding Debentures.

In case, in the question, the amount of DRR is more than 25% or less then 100% then you should go with the given amount so you don't need to calculate the amount of the DRR.

| Date | Particulars |

L. F. | Debit | Credit | |

|---|---|---|---|---|---|

| General Reserve A/c | Dr. | ***** | |||

| Dividend Equalisation Reserve | Dr. | ***** | |||

| Profit and Loss(Surplus) A/c | Dr. | ***** | |||

| To Debenture Redemption Reserve A/c | ***** | ||||

| (Being the amount transferred to DRR) | |||||

| Debenture Redemption Reserve A/c | Dr. | ***** | |||

| To General Reserve a/c | |||||

| (Being the amount of DRR transferred to the General Reserve at the time of redemption of debentures) | |||||

Thanks for reading the topic.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Debenture Redemption Reserve is the type of provision which is created by the company who issued the debentures in the market. This reserve ensuring the…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Advanced Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.