Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Cash -> | Assets -> | Real Account -> | cash comes In the business -> | What comes In -> | Debit |

| Building -> | Assets -> | Real Account -> | Building Comes In the business -> | What comes In -> | Debit |

| Furniture -> | Assets -> | Real Account -> | Furniture Comes In the business -> | What comes In -> | Debit |

| Capital->*1 | Personal -> | Personal Account -> | Owner giving cash and other assets to business-> | The Giver -> | Credit |

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

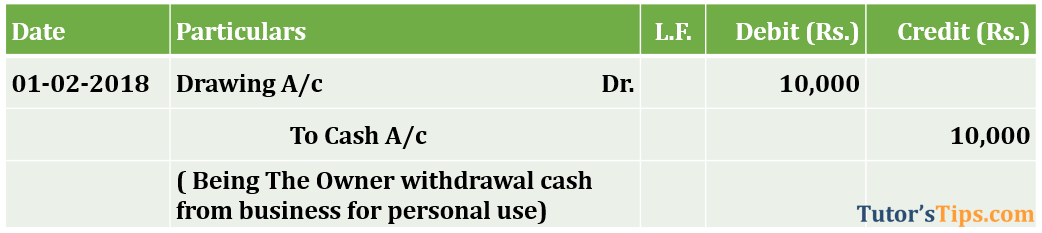

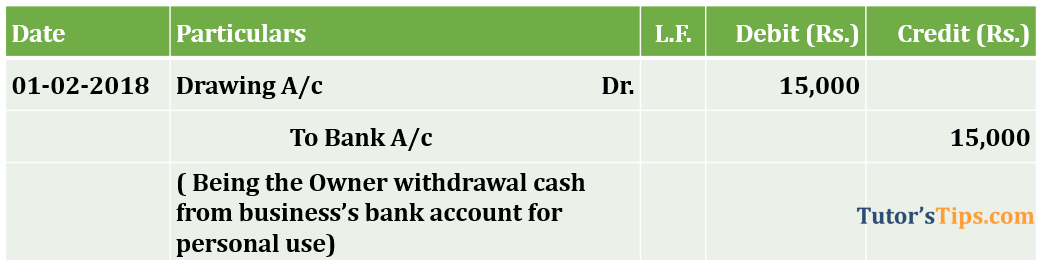

| Drawing-> *2 | Personal -> | Personal Account -> | Receiving cash from Business -> | The Receiver -> | Debit |

| Cash -> | Assets -> | Real Account -> | Goes out from business -> | What goes out -> | Credit |

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Drawing->*2 | Personal -> | Personal Account -> | Receiving cash from Business -> | The receiver -> | Debit |

| Bank->*3 | Personal -> | Personal Account -> | Paid Cash to Insurance Company -> | The giver -> | Credit |

Or

05/02/2018 Purchase of Goods for Rs 50,000/- for Cash Both transactions are cash transaction will be treated as below:| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Purchase ->*4 | Expense-> | Nominal Account -> | Spending money on goods -> | All Expenses and losses -> | Debit |

| Cash->*5 | Asset -> | Real Account -> | Paid Cash to Supplier -> | What goes out -> | Credit |

Or

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Cash-> | Asset -> | Real Account -> | Received Cash from Customer-> | What comes in -> | Debit |

| Sale-> *6 | Income -> | Nominal Account -> | Earned money from the selling of goods -> | All incomes and gains -> | Credit |

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Computer -> | Asset -> | Real Account -> | Purchased Computer -> | What comes in -> | Debit |

| Cash-> | Asset -> | Real Account -> | Paid Cash to Supplier -> | What goes out -> | Credit |

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Cash-> | Asset -> | Real Account -> | Cash Received form buyer-> | What comes in -> | Debit |

| Machine -> | Asset -> | Real Account -> | Sold old machine -> | What goes out -> | Credit |

| Profit on sale of Asset-> | Gain -> | Nominal Account -> | Business earn the gain on sale of Asset-> | All income and gains -> | Credit |

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Salary-> | Expense -> | Nominal Account -> | Spending money to pay salary-> | All expenses and losses -> | Debit |

| Cash->*5 | Asset -> | Real Account -> | Paid cash to Employees -> | What goes out -> | Credit |

| Name of Account | Type of Account | The rule will be Applied | Effect of a transaction on accounts | Condition of Rule applied | According to Rule, It will be Dr./Cr. |

|---|---|---|---|---|---|

| Cash-> | Asset -> | Real Account -> | Received Cash from Tenent -> | What comes in -> | Debit |

| Rent Received -> | Income -> | Nominal Account -> | Earned money from Building -> | All income and gains -> | Credit |

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

In this article, We will explain to you the Basic Journal Entries and after this chapter, You will know about all journal entries which are regularly used in…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

3 August 2021

3 August 2021