Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Today we are covering the topic of the Balance sheet. This is the last topic of final accounts. After this topic, we will cover all adjustments of the final account which is your next chapter. In this article, you will learn the meaning of the Balance Sheet, Feature, Needs, Format, and understand it in much better ways with examples.

It is the statement showing the position of the assets and liabilities of the business for a particular accounting period. It is a list of balances of the account of assets, capital, and liabilities. The value of assets shows which we can realize from the market and the value of Liabilities shows which we have to pay in the future. Capital shows the amount invested by the owner into the business entity. it is the basis of the following accounting equation.

"Assets = Capital + Liabilities"

You can check out the above equation's article from the below link which explained the concept behind it.

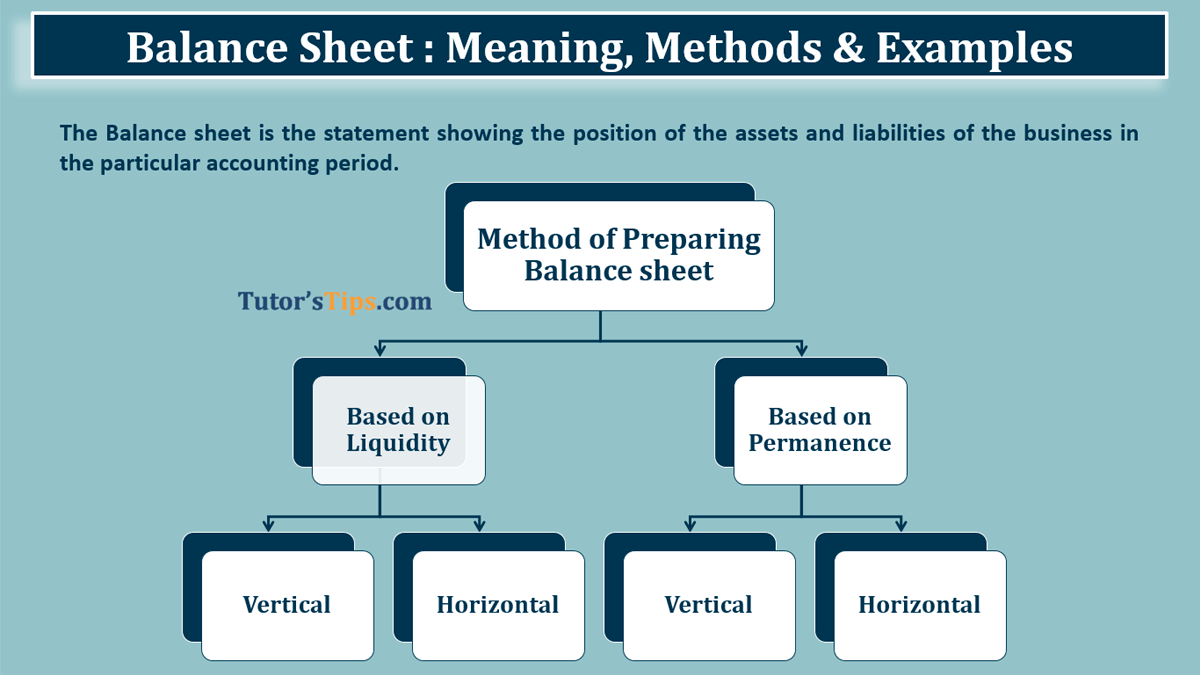

The preparation of a balance sheet is needed to:

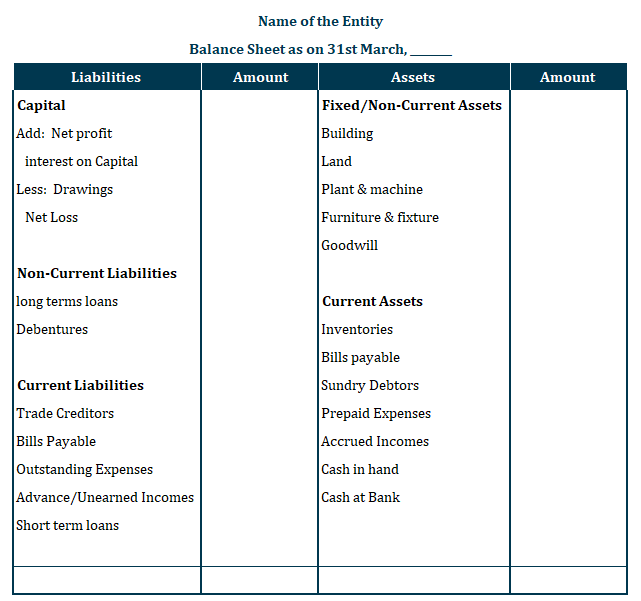

We have to prepare a balance sheet from the trial balance after preparing the trading and profit/loss account. The accounts left in the trial balance after preparing the trading and profit/loss account are posted in the balance sheet. The balance sheet is based on a simple equation i.e. Assets = capital + liabilities but there are different Balance sheet formats are available. Which we can differentiate only on the basis of the presentation of the balance of accounts. The balance sheet format are based on the following thing:-

In this format of balance sheets, Assets are arranged in such an order that most liquid asset is shown first, followed by the less liquid assets. Similarly, Liabilities are arranged in such an order that most urgent payments due shown first, followed by the less urgent and then shown capital(owner's equity).

The following is the Proforma of the balance sheet:-

Name of the Entity

| Balance Sheet as on 31st March, _______ |

|||

| Liabilities | Amount | Assets | Amount |

|---|---|---|---|

| Current Liabilities | Current Assets | ||

| Trade Creditors | Cash in hand | ||

| Bills Payable | Cash at Bank | ||

| Outstanding Expenses | Inventories | ||

| Advance/Unearned Incomes | Bills payable | ||

| Short term loans | Sundry Debtors | ||

| Non-Current Liabilities | Prepaid Expenses | ||

| long terms loans | Accrued Incomes | ||

| Debentures | Fixed/Non-Current Assets | ||

| Capital | Building | ||

| Add: Net profit | Land | ||

| interest on Capital | Plant & machine | ||

| Less: Drawings | Furniture & fixture | ||

| Net Loss | Goodwill | ||

In this format of balance sheets, Assets are arranged in such an order that the least liquid asset is shown first, followed by the more liquid assets. Similarly, Liabilities side capital shows first and followed by the long-term/non-current liabilities and then, short terms/current liabilities.

The following is the Proforma of the balance sheet:-

Name of the Entity

| Balance Sheet as on 31st March, _______ |

|||

| Liabilities | Amount | Assets | Amount |

|---|---|---|---|

| Capital | Fixed/Non-Current Assets | ||

| Add: Net profit | Building | ||

| interest on Capital |

Land | ||

| Less: Drawings | Plant & machine | ||

| Net Loss | Furniture & fixture | ||

| Goodwill | |||

| Non-Current Liabilities | Current Assets | ||

| long terms loans | Inventories | ||

| Debentures | Bills payable | ||

| Current Liabilities | Sundry Debtors | ||

| Trade Creditors | Prepaid Expenses | ||

| Bills Payable | Accrued Incomes | ||

| Outstanding Expenses | Cash in hand | ||

| Advance/Unearned Incomes | Cash at Bank | ||

| Short term loans | |||

Or if you want to download the Format please download the following image: -

The balance sheet can be presented in two forms.

The presentation of the Balance sheet discussed until now is called horizontal presentation. In this form of presentation, we had to present all account information across the page from left to right. All assets are shown on the corresponding side of all liabilities. All liabilities are shown on the left side of the balance sheet and all assets are shown on the right side of the balance sheet.

In the vertical form of presentation, we have to present all account information across the page from top to bottom. First, we show all liabilities and capital and then after all assets. It is also present in two way

Balance Sheet as on 31st March ____________

| Note No. | Current Year | Previous Year | |

|---|---|---|---|

| I. Liabilities | |||

| (1) Current Liabilities | |||

| (a) Trade Payable | |||

| (b) Other Current Liabilities | |||

| (c) Short-Term Provision | |||

| Total Current Liabilities | |||

| (2) Non-Current Liabilities | |||

| (a) long terms loans/Borrowing | |||

| (b) Other Long-Term Liabilities | |||

| Total Non-Current Liabilities | |||

| (3) Owner's Equity(Capital) | |||

| Add: Net profit | |||

| Interest on Capital | |||

| Less: Drawings | |||

| Net Loss | |||

| Total Owner's Equity | |||

| Total Liabilities | |||

| II. Assets | |||

| (1) Current Assets | |||

| (a) Cash in hand | |||

| (b) Cash at Bank | |||

| (c) Inventories | |||

| (d) Trade Receivables | |||

| (e) other current Assets | |||

| Total Current Assets | |||

| (2) Non-Current Assets | |||

| (a) Fixed Assets | |||

| (i) Tangible assets | |||

| (ii) Intangible assets | |||

| (iii) Capital work-in-progress | |||

| (iv) Intangible assets under development | |||

| (b) Non-current investments | |||

| (c) Deferred tax assets (net) | |||

| (d) Long-term loans and advances | |||

| (e) Other non-current assets | |||

| Total Non-Current Assets | |||

| Total Assets |

Balance Sheet as on 31st March ____________

| Balance Sheet as on 31st March ____________ | Note No. | Current Year | Previous Year |

|---|---|---|---|

| I. Liabilities | |||

| (1) Owner's Equity(Capital) | |||

| Add: Net profit | |||

| Interest on Capital | |||

| Less: Drawings | |||

| Net Loss | |||

| Total Owner's Equity | |||

| (2) Non-Current Liabilities | |||

| (a) long terms loans/Borrowing | |||

| (b) Other Long-Term Liabilities | |||

| Total Non-Current Liabilities | |||

| (3) Current Liabilities | |||

| (a) Trade Payable | |||

| (b) Other Current Liabilities | |||

| (c) Short-Term Provision | |||

| Total Current Liabilities | |||

| Total Liabilities | |||

| II. Assets | |||

| (1) Non-Current Assets | |||

| (a) Fixed Assets | |||

| (i) Tangible assets | |||

| (ii) Intangible assets | |||

| (iii) Capital work-in-progress | |||

| (iv) Intangible assets under development | |||

| (b) Non-current investments | |||

| (c) Deferred tax assets (net) | |||

| (d) Long-term loans and advances | |||

| (e) Other non-current assets | |||

| Total Non-Current Assets | |||

| (2) Current Assets | |||

| (a) Cash in hand | |||

| (b) Cash at Bank | |||

| (c) Inventories | |||

| (d) Trade Receivables | |||

| (e) other current Assets | |||

| Total Current Assets | |||

| Total Assets |

Or If you want to download the Format please download the following image: -

Note No.: - For every liabilities, capital and assets account a detailed note will be attached with the balance sheet. in this column, the note number will be shown in references.

Current Year: - Total of detailed note of each account is shown in this column.

Previous Year: - Total of the same account from the previous year's balance sheet will be shown in this column.

Prepare the balance sheet as of 31st March 2018

(Trial Balance only shows assets, liabilities, and capital account balances. )

| Particulars | Debit balance | Credit Balance |

|---|---|---|

| Capital | 10,00,000 | |

| Furniture & fixture | 1,00,000 | |

| Land & Building | 5,00,000 | |

| Sundry Creditors | 70,000 | |

| Bills Receivable | 15,000 | |

| Investment | 500,000 | |

| Inventories | 60,000 | |

| Bills payable | 25,000 | |

| Sundry Debtors | 50,000 | |

| Prepaid Insurance | 20,000 | |

| Accrued interest on Investment | 15,000 | |

| Outstanding Salary | 50,000 | |

| Rent received in advance | 25,000 | |

| Short term loans | 40,000 | |

| Cash in hand | 50,000 | |

| Cash at Bank | 170,000 | |

| the loan from Bank(repayable within 7 years) |

2,00,000 | |

Net Profit for the year ended is Rs 90,000/-

We will solve this example with both methods.

Balance Sheet as of 31st March 2018

| Liabilities | Amount | Assets | Amount | |

|---|---|---|---|---|

| Current Liabilities | Liquid Assets | |||

| Trade Creditors | 70,000 | Cash in hand | 50,000 | |

| Bills Payable | 25,000 | Cash at Bank | 1,70,000 | |

| Outstanding Expenses | 50,000 | Inventories | 60,000 | |

| Advance/Unearned Incomes | 25,000 | Bills Receivable | 15,000 | |

| Short term loans | 40,000 | Sundry Debtors | 50,000 | |

| Non-Current Liabilities | Prepaid Insurance | 20,000 | ||

| Bank Loan | 2,00,000 | Accrued interest on Investment | 15,000 | |

| Capital | 10,00,000 | Fixed/Non-Current Assets | ||

| Add: Net profit | 90,000 | Land & Building | 5,00,000 | |

| Less: Drawings | 20,000 | Furniture & fixture | 1,00,000 | |

| 10,70,000 | Investment | 5,00,000 | ||

| 14,80,000 | 14,80,000 | |||

Balance Sheet as of 31st March 2018

| Liabilities | Amount | Assets | Amount | |

|---|---|---|---|---|

| Capital | 10,00,000 | Fixed/Non-Current Assets | ||

| Add: Net profit | 90,000 | Land & Building | 5,00,000 | |

| Less: Drawings | 20,000 | Furniture & fixture | 1,00,000 | |

| 10,70,000 | Investment | 5,00,000 | ||

| Non-Current Liabilities | Current Assets | |||

| Bank loan | 2,00,000 | Inventories | 60,000 | |

| Bills Receivable | 15,000 | |||

| Current Liabilities | Sundry Debtors | 50,000 | ||

| Trade Creditors | 70,000 | Prepaid Insurance | 20,000 | |

| Bills Payable | 25,000 | Accrued interest on Investment | 15,000 | |

| Outstanding Expenses | 50,000 | Cash in hand | 50,000 | |

| Advance/Unearned Incomes | 25,000 | Cash at Bank | 1,70,000 | |

| Short term loans | 40,000 | |||

| 14,80,000 | 14,80,000 | |||

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

Today we are covering the topic of the Balance sheet. This is the last topic of final accounts. After this topic, we will cover all adjustments of the final…

Class 11 and Class 12 commerce students, and CA Foundation aspirants, studying Financial Accounting.

Yes — this page includes a short interactive quiz so you can check your understanding straight away.

22 February 2022

23 February 2022

2 December 2022

2 December 2022

8 January 2023