Question No 6 Chapter No 8

Journalise the following transactions:

| (i) | Goods worth Rs 500 given as charity. |

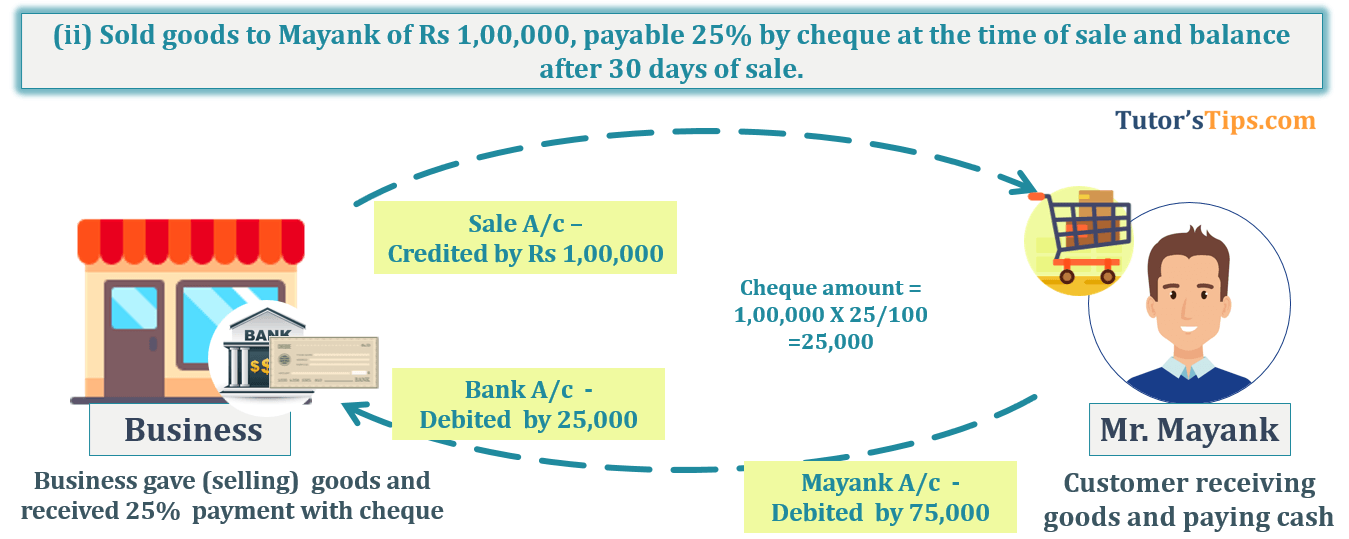

| (ii) | Sold goods to Mayank of Rs 1,00,000, payable 25% by cheque at the time of sale and balance after 30 days of sale. |

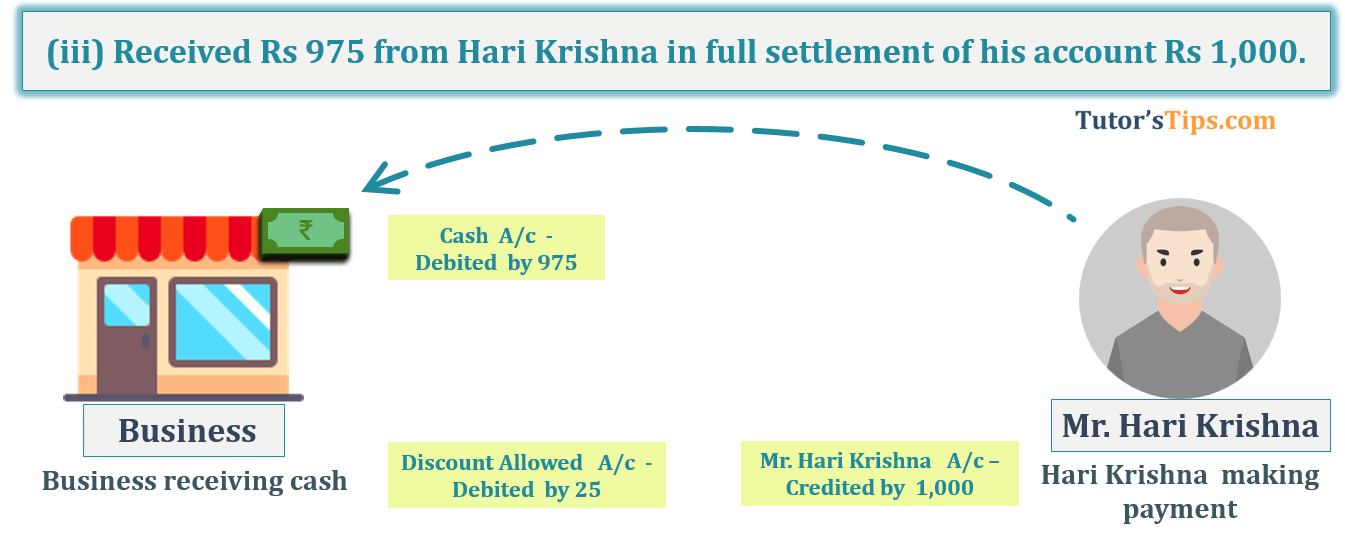

| (iii) | Received Rs 975 from Harikrishna in full settlement of his account Rs 1,000. |

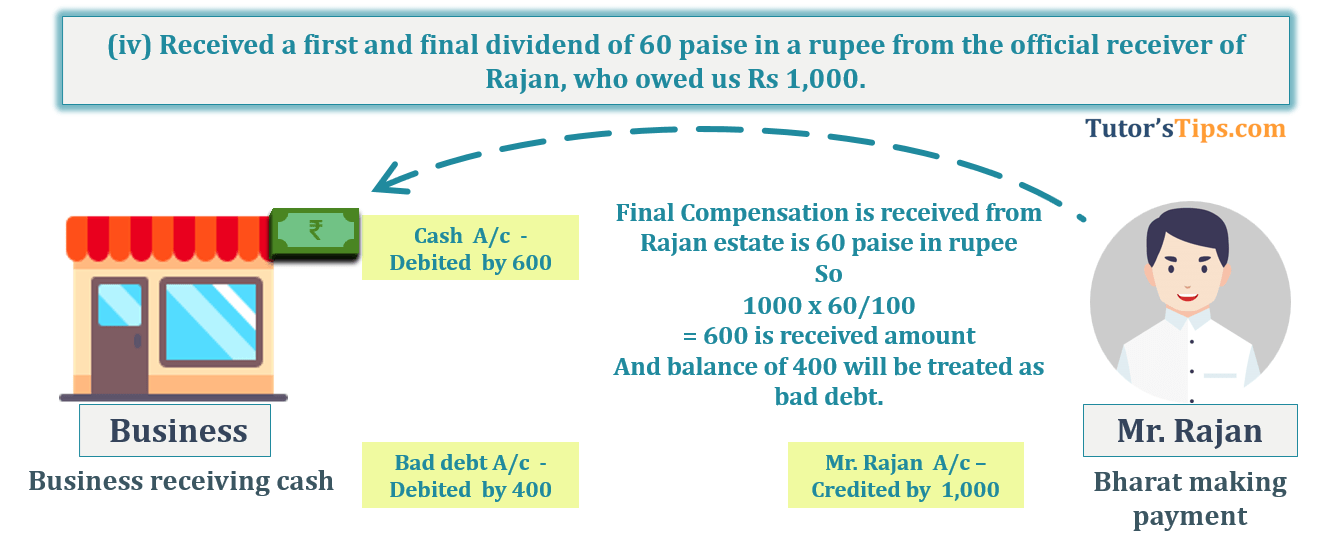

| (iv) | Received a first and final dividend of 60 paise in a rupee from the official receiver of Rajan, who owed us Rs 1,000. |

| (v) | Charged depreciation on plant Rs 1,000. |

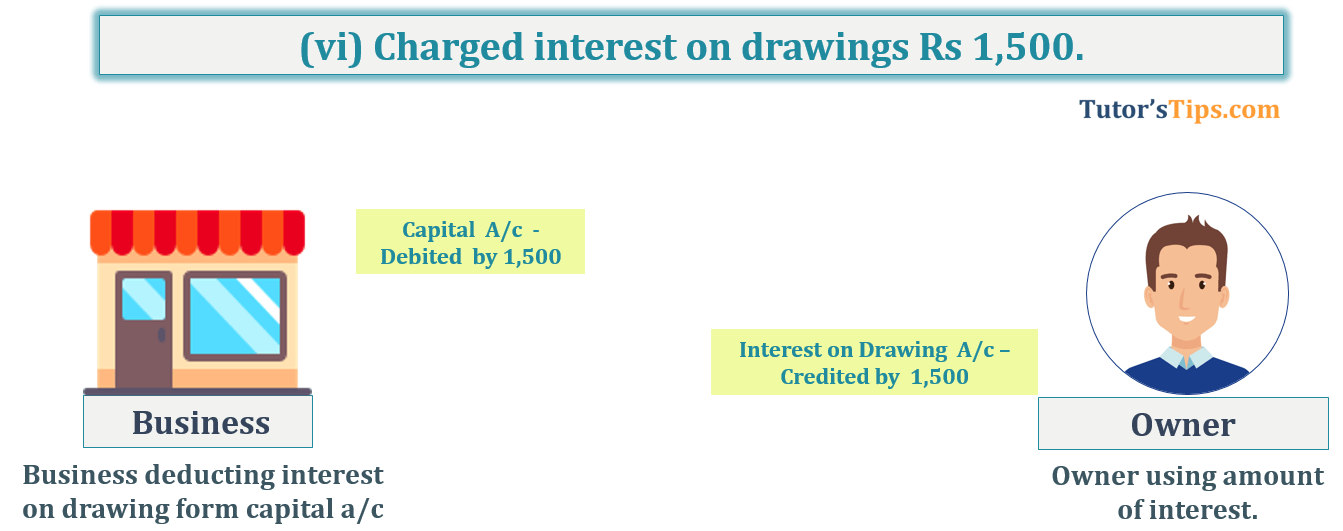

| (vi) | Charged interest on drawings Rs 1,500 |

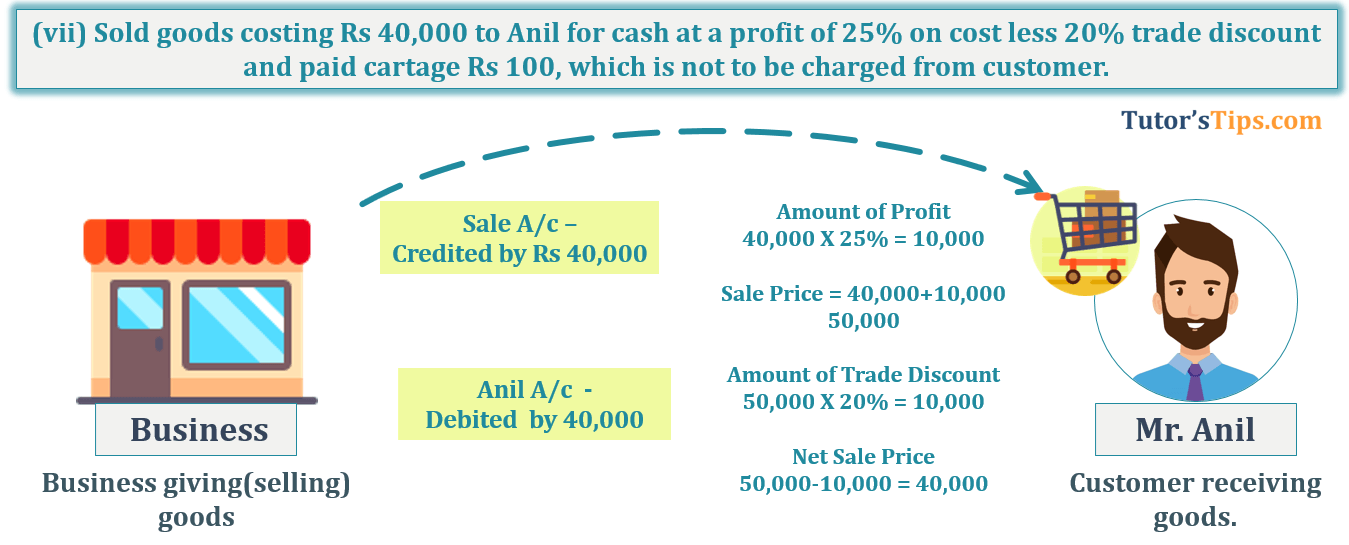

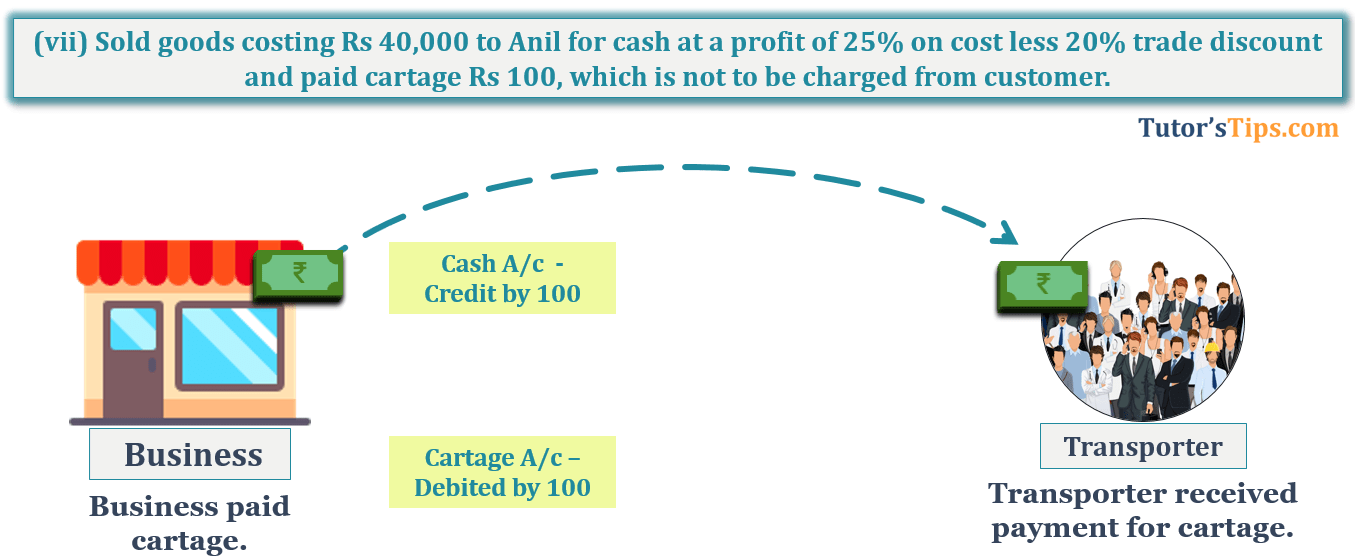

| (vii) | Sold goods costing Rs 40,000 to Anil for cash at a profit of 25% on cost less 20% trade discount and paid cartage Rs 100, which is not to be charged from customer. |

Solution of Question No 6 Chapter No 8: –

| Date | Particulars |

L.F. | Debit | Credit | |

| (i) | Charity A/c | Dr. | 500 | ||

| To Purchase A/c | 500 | ||||

| (Being goods given as charity.) | |||||

| (ii) | Mayank A/c | Dr. | 75,000 | ||

| Bank A/c | Dr. | 25,000 | |||

| To Sales A/c | 1,00,000 | ||||

| (Being goods sold to Mayank and 25% payment received with a cheque.) | |||||

| (iii) | Cash A/c | Dr. | 975 | ||

| Discount Allowed A/c | Dr. | 25 | |||

| To Hari Krishna A/c | 1,000 | ||||

| (Being cash received from Hari Krishna with the full settlement.) | |||||

| (iv) | Cash A/c | Dr. | 600 | ||

| Bad debts A/c | Dr. |

400 |

|||

| To Rajan A/c | 1,000 | ||||

| (Being rent due to landlord but not paid.) | |||||

| (v) | Depreciation A/c | Dr. | 1,000 | ||

| To Plant A/c | 1,000 | ||||

| (Being Depreciation charged on Plant.) | |||||

| (vi) | Capital A/c | Dr. | 1,500 | ||

| To Interest on Drawing A/c | 1,500 | ||||

| (Being interest charges on interest on drawing.) | |||||

| (vii) | Anil A/c | Dr. | 40,000 | ||

| To Sales A/c | 40,000 | ||||

| (Being goods sold to Anil at 20% trade discount) | |||||

| Cartage A/c | Dr. | 100 | |||

| To Cash A/c | 100 | ||||

| (Beingcartage paid in cash on above sale.) | |||||

Explanation of All Transactions with images: –

This is not a part of the solution, So you don’t have to write it in the exam. So, why we explained if it is not needed. Because This explanation will help you to understand all transactions with logic and you don’t need to remember all the transactions but just understand and remember the logic use behind it.

Transaction No. 1

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Charity |

Expenses |

Nominal Account |

50% Payment received in cash |

Cash comes in |

Debit |

|

Purchase (goods) |

Assets |

Real Account |

Goods given as charity |

Goods goes out |

Credit |

Transaction No. 2

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Sales a/c (Goods) |

Assets |

Real |

Goods giving by Business |

Goods Goes out |

Credit |

|

Bank |

Artificial Person |

Personal |

Payment received by cheque |

Bank is receiver |

Debit |

|

Mayank |

Person |

Personal |

Goods received |

Mayank is receiver |

Debit |

Transaction No. 3

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Cash |

Assets |

Real Account |

Payment received in cash |

Cash comes in |

Debit |

|

Discount allowed |

Loss |

Nominal Account |

Loss for receiving payment early |

All Expenses and Losses |

Debit |

|

Mr. Hari Krishna |

Person |

Personal Account |

Making payment |

Giver |

Credit |

Transaction No. 4

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Cash |

Assets |

Real Account |

Payment received in cash |

Cash comes in |

Debit |

|

Bad debt |

Loss |

Nominal Account |

Loss for not receiving due amount |

All Expenses and Losses |

Debit |

|

Mr. Rajan |

Person |

Personal Account |

Making payment |

Giver |

Credit |

Transaction No. 5

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Depreciation |

Loss |

Nominal |

Value of assets diminished |

All Expenses and Losses |

Debit |

|

Plant |

Assets |

Real |

Assets decreasing |

Goes out |

Credit |

Transaction No. 6

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Owner |

Person |

Personal A/c |

The owner is using an amount of Interest for his own purpose not paying it to the business. |

Owner is indirectly receiving cash |

Debit |

|

Interest on Drawing |

Income |

Nominal A/c |

Interest earned by Business |

All Income and gains |

Credit |

Transaction No. 7

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Sales a/c (Goods) |

Assets |

Real Account |

Goods giving by Business |

Goods Go out |

Credit |

|

Anil a/c |

Person |

Personal Account |

Goods received |

Pawan is receiver |

Debit |

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|

Cartage |

Expenses |

Nominal Account |

Expenses Incurred |

All Exp. or Loss |

Debit |

|

Cash |

Assets |

Real Account |

Cash paid by a business |

Cash goes out |

Credit |

Thanks Please share with your friends

Comment if you have any questions.

T.S. Grewal’s Double Entry Book Keeping (Class +1) – Solution

Chapter No. 1 – Introduction to Accounting

Chapter No. 2 – Basic Accounting Terms

Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

Chapter No. 4 – Bases of Accounting

Chapter No. 5 – Accounting Equation

Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

Chapter No. 10 – Special Purpose Books I – Cash Book

Chapter No. 11 – Special Purpose Books II – Other Books

Chapter No. 12 – Bank Reconciliation Statement

Chapter No. 13 – Trial Balance

Chapter No. 15 – Provisions and Reserves

Chapter No. 16 – Accounting for Bills of Exchange

Chapter No. 17 – Rectification of Errors

Chapter No. 18 – Financial Statements of Sole Proprietorship

Chapter No. 19 – Adjustments in preparation of Financial Statements

Chapter No. 20 – Accounts from incomplete Records – Single Entry System

Chapter No. 21 – Computers in Accounting

Chapter No. 22 – Accounting Software – Tally

Check out T.S. Grewal’s +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal’s Double Entry Book Keeping