Question 70 Chapter 5 – Unimax Class 12 Part 1 – 2021

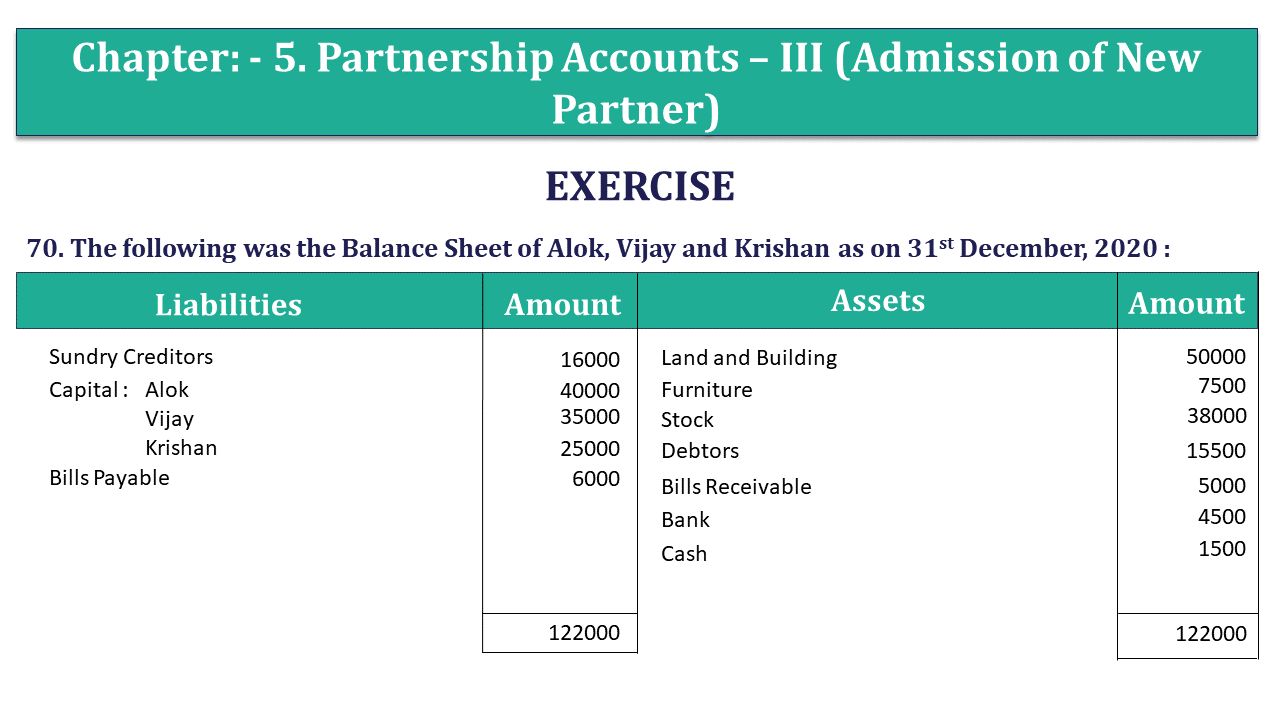

70. The following was the Balance Sheet of Alok, Vijay and Krishan as on 31st December, 2020 :

| Liabilities | Amount | Assets | Amount | |

| Sundry Creditors | 16,000 | Land and Building | 50,000 | |

| Capital : | Furniture | 7,500 | ||

| Alok | 40,000 | Stock | 38,000 | |

| Vijay | 35,000 | Debtors | 15,500 | |

| Krishan | 25,000 | Bills Receivable | 5,000 | |

| Bills Payable | 6,000 | Bank | 4,500 | |

| Cash | 1500 | |||

| 1,22,000 | 1,22,000 |

They share Profits and Losses in the ratio of 6 : 5 : 3. They agreed on 1st January, 2021 to admit Suresh in the partnership and give him 1/10th share in profits on the following terms :

- Suresh would bring in Rs. 28400 as his share of capital.

- Stock would be depreciated by Rs. 3000 and furniture by Rs. 900.

- A provision of Rs. 1300 be made for outstanding rapairs bill.

- The value of land and building be appreciated upto Rs. 65000.

- Goodwill of the firm is valued at Rs. 84000 before the admission of Suresh and he is unable to bring his share of assets in cash.

Pass necessary Journal Entries to record the above arrangements and prepare Revaluation account, Capital a/cs and the new Balance Sheet of the firm after Suresh’s admission.

The solution of Question 70 Chapter 5 – Unimax Class 12 Part 1: –

Journal

| Date | Particulars | L.F. | Debit | Credit | |

| Building a/c | Dr. | 15,000 | |||

| To Revaluation A/c | 15,000 | ||||

| (Being value of assets increased) | |||||

| Revaluation a/c | Dr. | 5,200 | |||

| To Stock a/c | 3,000 | ||||

| To Furniture a/c | 900 | ||||

| To Outstanding repairs bill a/c | 1,300 | ||||

| (Being value of asset decreased) | |||||

| Revaulation a/c | Dr. | 9,800 | |||

| To Alok’s Capital A/c | 4,200 | ||||

| To Vijay’s Capital a/c | 3,500 | ||||

| To Krishan’s Capital a/c | 2,100 | ||||

| (Being profit distributed among old partners’ in old ratio) | |||||

| Cash a/c | Dr. | 28,400 | |||

| To Suresh’s Capital A/c | 28,400 | ||||

| (Being goodwill brought by new partner) | |||||

| Suresh’s Capital a/c | Dr. | 8,400 | |||

| To Alok’s Capital A/c | 3,600 | ||||

| To Vijay’s Capital a/c | 3,000 | ||||

| To Krishan’s Capital a/c | 1,800 | ||||

| (Being compensation paid to old partner’s as Suresh’s share of goodwill) |

Revaluation A/c

| Particulars | Rs. | Particulars | Rs. | |

| To Stock a/c | 3,000 | By Building a/c | 15,000 | |

| To Furniture a/c | 900 | |||

| To Provision for outstanding repairs bill | 1,300 | |||

| To Profit on revaluation | ||||

| Alok ( 6 : 5 : 3 ) | 4,200 | |||

| Vijay | 3,500 | |||

| Krishan | 2,100 | 9,800 | ||

| 15,000 | 15,000 |

Capital Accounts

| Particulars | Alok | Vijay | Krishan | Suresh | Particulars | Alok | Vijay | Krishan | Suresh |

| To Alok’s Cap. | – | – | – | 3,600 | By Balance b/d | 40,000 | 35,000 | 25,000 | – |

| To Vijay Cap. | – | – | – | 3,000 | By Cash a/c | – | – | – | 28,400 |

| To Vijay Cap. | – | – | – | 1,800 | By Suresh’s Cap. | 3,600 | 3,000 | 1,800 | – |

| To Balance c/d | 47,800 | 41,500 | 28,900 | 20,000 | By Profit on rev. | 4,200 | 3,500 | 2,100 | – |

| 47,800 | 41,500 | 28,900 | 28,400 | 47,800 | 41,500 | 28,900 | 28,400 |

Balance Sheet

| Liabilities | Rs. | Assets | Rs. | ||

| Bills Payable | 6,000 | Land and Building | 65,000 | ||

| Capital Accounts | Furniture | 6,600 | |||

| Alok | 47,800 | Stock | 35,000 | ||

| Vijay | 41,500 | Debtors | 15,500 | ||

| Krishan | 28,900 | Bills Receivable | 5,000 | ||

| Suresh | 20,000 | 1,38,200 | Bank | 4,500 | |

| Creditors | 16,000 | Cash (1500 + 28400) | 29,900 | ||

| Outstanding repairs bill | 1,300 | ||||

| 1,61,500 | 1,61,500 |

Working Note:

Suresh’s share of goodwill = 1/10 X 84000 = Rs. 8400

What is Partnership – Meaning and Its 4 Types

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication