Question 55 Chapter 8 -Unimax

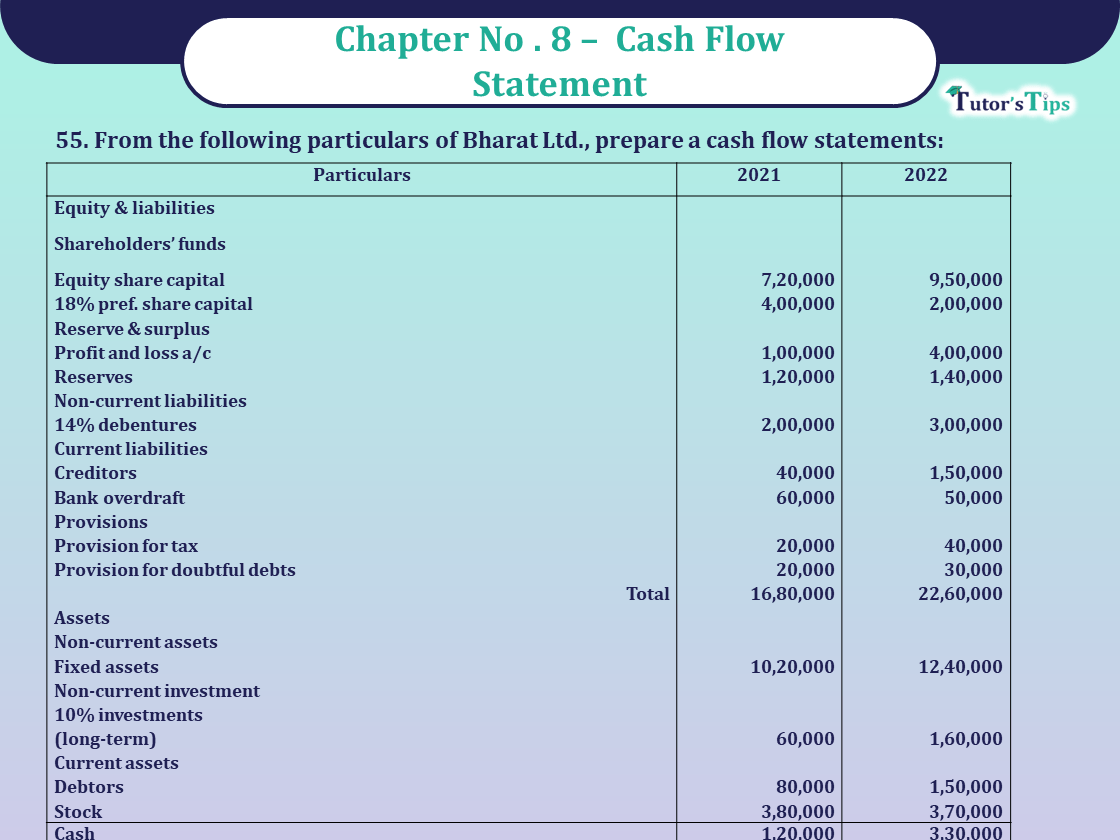

55. From the following particulars of Bharat Ltd., prepare a cash flow statement:

| Particulars | ₹ | ₹ | |

| Equity & liabilities | |||

| Shareholders’ funds | |||

| Equity share capital | 7,20,000 | 9,50,000 | |

| 18% pref. Share capital | 4,00,000 | 2,00,000 | |

| Reserve & surplus | |||

| Profit and loss a/c | 1,00,000 | 4,00,000 | |

| Reserves | 1,20,000 | 1,40,000 | |

| Non-current liabilities | |||

| 14% debentures | 2,00,000 | 3,00,000 | |

| Current liabilities | |||

| Creditors | 40,000 | 1,50,000 | |

| Bank Overdraft | 60,000 | 50,000 | |

| Provision for tax | 20,000 | 40,000 | |

| Provision for doubtful debts | 20,000 | 30,000 | |

| Total | 16,80,000 | 22,60,000 | |

| Assets | |||

| Non-current assets | |||

| Fixed assets | 10,20,000 | 12,40,000 | |

| Non-current investment | |||

| 10% investments (long-term) |

60,000 | 1,60,000 | |

| Current assets | |||

| Debtors | 80,000 | 1,50,000 | |

| Stock | 3,80,000 | 3,70,000 | |

| Cash | 1,20,000 | 3,30,000 | |

| Other current assets | |||

| Underwriting commission | 5,000 | 6000 | |

| Discount on issue | |||

| Debentures | 15,000 | 4000 | |

| Total | 16,80,000 | 22,60,000 | |

You are informed that during the year:

Proposed dividend 2021 1,20,000; 2022 1,50,000.

(a) A machine costing 1,40,000 (depreciation provided thereon 60,000) was sold for 50,000, depreciation charged during the year was 1,40,000.

(b) An interim dividend @ 15% was paid on equity shares. A new share was issued on 31.12.2022.

(c) Tax paid during the year was 10,000.

(d) On 31.12.2022 some investments were purchased for 1,80,000 and some, investments were sold at a profit of 20% on sale.

(e) Preference shares were redeemed on 31.12.2022 at a premium of 5%

The solution of Question 55 Chapter 8 – Unimax Publication Class 12 Part 2-2021: –

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31st DEC,2022

| Particulars | ₹ | ₹ | |

| Cash from operating activities: | |||

| Net profit as per balance sheet | 3,00,000 | ||

| Add: non-cash, non-operating expenses: | |||

| Discount on issue of debentures w/o | 11,000 | ||

| Depreciation charged | 1,40,000 | ||

| Loss on sale of machinery | 30,000 | ||

| Interim dividend paid | 1,08,000 | ||

| Provision for taxation | 30,000 | ||

| Premium paid on redemption of pref. shares | 10,000 | ||

| Preference share dividend paid | 72,000 | ||

| Transfer to reserve | 20,000 | ||

| Interest on debentures | 28,000 | ||

| Proposed dividend | 1,20,000 | 5,69,000 | |

| Less: non-cash, non-operating incomes: | |||

| Interest received on investment | (6,000) | ||

| Profit on sale of investment | (16,000) | (22,000) | |

| Add: decrease in current assets & increase in current liability: | |||

| Decrease in stock | 10,000 | ||

| Increase in creditors | 1,10,000 | ||

| Increase in provision for doubtful debts | 10,000 | ||

| Decrease in current liabilities & | |||

| Increase in current assets: | |||

| Increase in debtors | (70,000) | 60,000 | |

| Less: income paid tax | (10,000) | (10,000) | |

| Cash flow from operating activities | 8,97,000 | ||

| Cash from investing activities: | |||

| Purchase of investment | (1,80,000) | ||

| Purchase of machinery | (4,40,000) | ||

| Sale of machinery | 50,000 | ||

| Sale of investment | 96,000 | ||

| Interest received from investment | 6,000 | ||

| Cash flow from investing activities | (4,68,000) | ||

| Cash from financing activities: | |||

| Issue of equity share capital | 2,30,000 | ||

| Redemption of pref. share capital (2,00,000+10,000) | (2,10,000) | ||

| Issue of debenture | (99,000) | ||

| Underwriting commission | (1,08,000) | ||

| Interim dividend paid | (72,000) | ||

| Bank Overdraft | (10,000) | ||

| Interest on debentures | (28,000) | ||

| Proposed dividend paid | (1,20,000) | ||

| Cash flow from financial activity | (2,19,000) | ||

| Net increase | 2,20,000 | ||

| Add: opening cash & bank overdraft (1,20,000) | 60,000 | ||

| Closing cash & bank overdraft (3,30,000) | 2,80,000 | ||

Working Notes:

MACHINERY A/C

| Particulars | ₹ | Particulars | ₹ |

| To Balance b/d | 10,20,000 | By Cash a/c (sale) | 50,000 |

| To Cash a/c (purchased) (B/F) | 4,40,000 | By Profit & loss a/c (loss) | 30,000 |

| By Profit & loss a/c (Depreciation charged) |

1,40,000 | ||

| By Balance c/d | 12,40,000 | ||

| 14,60,000 | 14,60,000 |

Provision for taxation A/C

| Particulars | ₹ | Particulars | ₹ |

| To Cash a/c (tax paid) | 10,000 | By Balance b/d | 20,000 |

| To Balance c/d | 40,000 | By Profit & loss a/c (B/F) | 30,000 |

| (New provision) | |||

| 50,000 | 50,000 |

Investment A/c

| Particulars | ₹ | Particulars | ₹ |

| To Balance b/d | 60,000 | By Cash a/c (sale) | 96,000 |

| To Profit & loss a/C | 16,000 | By Balance c/d | 1,60,000 |

| To Purchase | 1,80,000 | ||

| 2,56,000 | 2,56,000 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

What is the cash flow statement? why do we need to prepare?

Unimax Publication – Accountancy PSEB Class 12 – Volume I – Solution

- Chapter No. 1 – Accounting Not-for-Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Change in Profit sharing ratio among Existing Partners )

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Unimax Publication – Accountancy PSEB (Class 12) – Part – II – Solution

- Chapter No. 1 – Company Accounts (Share Capital)

- Chapter No. 2 – Company Accounts (Issue of Debentures)

- Chapter No. 3 – Company Accounts (Redemption of Debentures)

- Chapter No. 4 – Financial Statements of a Company

- Chapter No. 5 – Financial Statement Analysis

- Chapter No. 6 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 7 – Ratio Analysis

- Chapter No. 8 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication