Question 53 Chapter 5 – Unimax Class 12 Part 1 – 2021

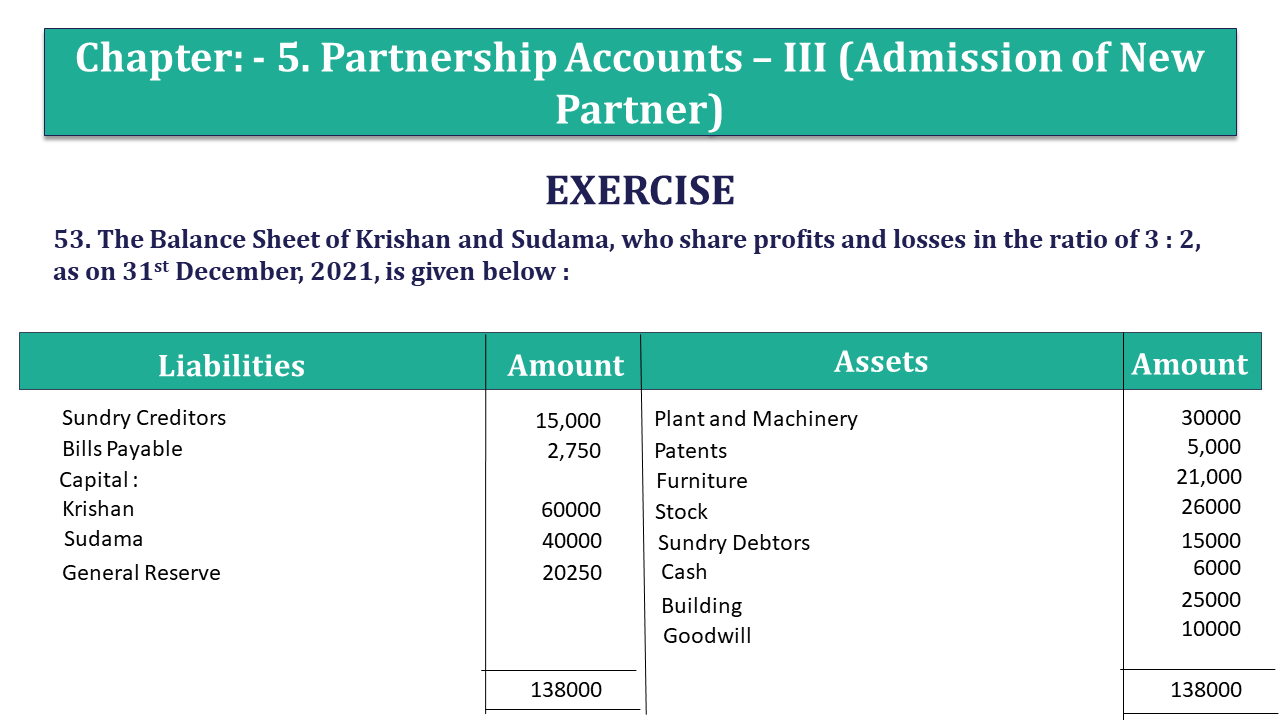

53. The Balance Sheet of Krishan and Sudama, who share profits and losses in the ratio of 3 : 2, as on 31st December, 2021, is given below :

| Liabilities | Amount | Assets | Amount |

| Sundry Creditors | 15,000 | Plant and Machinery | 30000 |

| Bills Payable | 2,750 | Patents | 5,000 |

| Capital : | Furniture | 21,000 | |

| Krishan | 60000 | Stock | 26000 |

| Sudama | 40000 | Sundry Debtors | 15000 |

| General Reserve | 20250 | Cash | 6000 |

| Building | 25000 | ||

| Goodwill | 10000 | ||

| 138000 | 138000 |

On the date of the Balance Sheet, Balram is admitted as a partner with 1/4th share in profits upon the following conditions :

(a) He is to contribute proportionate capital and his share of goodwill in cash.

(b) Goodwill is to be valued at 2 years’ purchase of 4 years’ average profits, which were Rs. 10000; Rs. 9000 ; Rs. 8000 and Rs. 13000 respectively.

(c) Plant and Machinery is to be written down to Rs. 25000 and Patents written up to Rs. 9000.

A provision of 5% on debtors is required. A liability of Rs. 500 included in sundry creditors is not likely to arise.

Pass Journal entries on Balram’s admission and give the Balance Sheet after admission.

The solution of Question 53 Chapter 5 – Unimax Class 12 Part 1

Journal

| Date | Particulars | L.F. | Debit | Credit | |

| Revaluation a/c | Dr. | 5750 | |||

| To Plant and Machinery A/c | 5000 | ||||

| To Provision for bad debts A/c | 750 | ||||

| (Being value of assets decreases) | |||||

| Patents a/c | Dr. | 4000 | |||

| Sundry Creditors A/c | Dr. | 500 | |||

| To Revaluation a/c | 4500 | ||||

| (Being value of asset decreased) | |||||

| Krishan’s Capital a/c | Dr. | 750 | |||

| Sudama’s Capital a/c | Dr. | 500 | |||

| To revaluation a/c | 1250 | ||||

| General Reserve a/c | Dr. | 20250 | |||

| To Krishns’s Capital a/c | 12150 | ||||

| To Sudama’s Capital a/c | 8100 | ||||

| (Being reserve transferred to old partners’ capital) |

| Date | Particulars | L.F. | Debit | Credit | |

| Krishna’s Capital a/c | Dr. | 6000 | |||

| Sudama’s Capital A/c | 4000 | ||||

| To Goodwill a/c | 10000 | ||||

| (Being old goodwill w/o) | |||||

| Cash a/c | Dr. | 43000 | |||

| To Balrama’s Capital A/c | 38000 | ||||

| To Premium A/c | 5000 | ||||

| (Being Capital and goodwill brought by new partner) | |||||

| Premium a/c | Dr. | 5000 | |||

| To Krishna’s Capital A/c | 3000 | ||||

| To Sudama’s Capital A/c | 2000 | ||||

| (Being goodwill transferred to old partner’s a/c) |

Revaluation A/c

| Particulars |

Rs. | Particulars |

Rs. | |

| To Plant and Machinery A/c | 5000 | By Patents a/c | 4000 | |

| To Provision for doubtful debts a/c (5% on 15000) | 750 | By Creditors a/c | ||

| By Loss on revaluation | ||||

| Krishna (3 : 2) | 750 | |||

| Sudama | 500 | 1250 | ||

| 5750 | 5750 |

Capital Accounts

| Particulars | A | B | C | Particulars | A | B | C |

| To Goodwill a/c | 6000 | 4000 | _ | By Balance b/d | 60000 | 40000 | _ |

| To Loss on revaluation a/c | 750 | 500 | By Cash A/c | _ | _ | 38000 | |

| To Balance c/d | 68400 | 45600 | 38000 | By Premium A/c | 3000 | 2000 | _ |

| By General Reserve A/c | 12150 | 8100 | _ | ||||

| 75150 | 50100 | 38000 | 75150 | 50100 | 38000 |

Balance Sheet

| Liabilities |

Rs. | Assets |

Rs. | ||

| Sundry Creditors | 14500 | Plant and Machinery | 25000 | ||

| Capital Accounts | Patents | 9000 | |||

| Krishna | 68400 | Furniture | 21000 | ||

| Sudama | 45600 | Debtors | 15000 | ||

| Balram | 38000 | 152000 | Less Provision for bad debts | 750 | 14250 |

| Bills Payable | 2750 | Stock | 26000 | ||

| Cash (6000 + 5000 + 38000) | 49000 | ||||

| Building | 25000 | ||||

| 169250 | 169250 |

Working Note

(A) Calculation of value of Balrama’s G.W. share :

4 years average profit =10000 + 9000 + 8000 + 13000/4

Total G.W. = 10000 X 2 = Rs. 20000

Balram’s Share = 1/4 X 20000 = Rs. 5000

(B) Calculation Balram’s Capital :

For 3/4 share capital contributed = Rs. 114000

For 1 share capital contributed = Rs. 114000 X 4/3

For 1/4 share capital contributed = Rs. 114000 X 4/3 X 1/4

= Rs. 38000

What is Partnership – Meaning and Its 4 Types

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication