Question 47 Chapter 1 of +2-Part-1

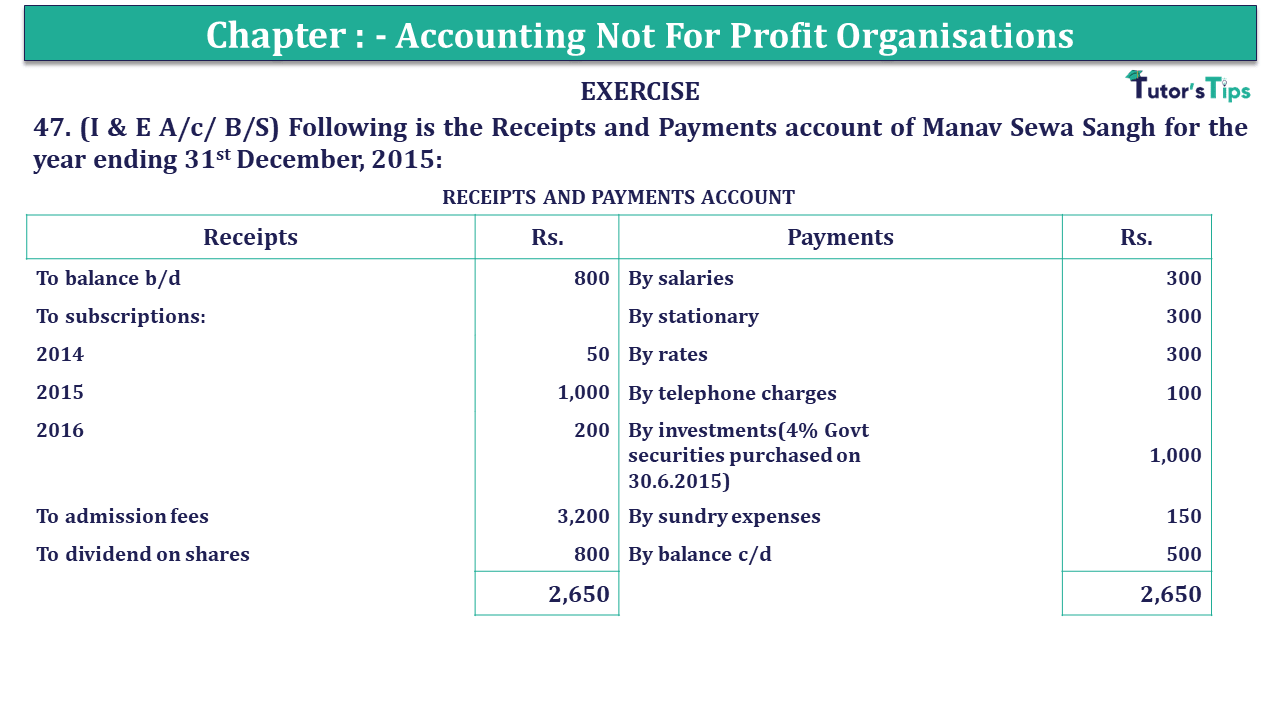

47. (I & E A/c/ B/S) Following is the Receipts and Payments account of Manav Sewa Sangh for the year ending 31st December 2015:

| RECEIPTS AND PAYMENTS ACCOUNT | |||

| Receipts | Rs. | Payments | Rs. |

| To balance b/d – Cash in hand | 800 | By salaries | 300 |

| To subscriptions: | By stationary | 300 | |

| 2014 (previous year) | 50 | By rates | 300 |

| 2015 | 1,000 | By telephone charges | 100 |

| 2016(new year) | 200 | By investments(4% Govt securities purchased on 30.6.2015) | 1,000 |

| To admission fees | 3,200 | By sundry expenses | 150 |

| To dividend on shares | 800 | By balance c/d | 500 |

| 2,650 | 2,650 | ||

Further information:

1) There are 600 members paying annual subscription Of Rs. 2 per head, Rs.90 being in arrear for 2014 at the beginning of 2015.

2) Stock of stationery on 31st December 2014 was Rs.200, on 31st December, 2015-Rs.100.

3) The rates were paid for 15 months up to 31st March 2016.

4) Sundry expenses outstanding on 31st December 2014 were Rs.50.

5) Telephone charges for 3 months outstanding, the amount due is Rs.40.

6) At 31st December 2014 – investments in shares were Rs.4,000.

7) At 31st December 2014 – the building stood in the books at Rs.10,000 and it is required to write off depreciation at 5% p.a.

You are required to prepare:

(a) the Income and Expenditure Account for the year ended 31st December 2015 and

(b) the balance sheet as on that date.

The solution of Question 47 Chapter 1 of +2 Part-1: –

| Income and Expenditure account of Manav Sewa Sangh For the year ending 31st December 2015 |

|||||

| Expenditure |

Amount | Income |

Amount | ||

| To salaries | 300 | By subscriptions | 1,000 | ||

| To stationary | 300 | Add: outstanding (600*2)-1,000 | 200 | 1,200 | |

| Add: opening stock | 200 | By dividend on shares | 200 | ||

| Less: closing stock | 100 | 400 | By interest on investments (1,000 x 4/100 x 6/12) |

20 | |

| To rates | 300 | By excess of expenditure over income (deficit) | 260 | ||

| Less: Prepaid 1/5 | 60 | 360 | |||

| To telephone charges | 100 | ||||

| Add: outstanding | 40 | 140 | |||

| To sundry expenses | 150 | ||||

| Less: paid for 2014 | 50 | 100 | |||

| To depreciation on building @5% | 500 | ||||

| 1,680 | 1,680 | ||||

| Balance Sheet As on 31st March 2015 |

|||||

| Liabilities |

Amount | Assets |

Amount | ||

| Capital Fund: | Cash in hand | 500 | |||

| -Opening Balance | 15,040 | Outstanding Subscriptions: | |||

| Add: Admission fees | 400 | -2014 (90 – 50) | 40 | ||

| Less: Deficiency | 260 | 15,180 | -2015 | 200 | 240 |

| Outstanding telephone charges | 40 | Stock of stationary | 100 | ||

| Subscriptions received in advance | 200 | Prepaid rates (300 x 3/15) | 60 | ||

| Investments in shares | 4,000 | ||||

| 4% Investments | 1,000 | ||||

| Accrued interest | 20 | ||||

| Building | 10,000 | ||||

| Less: Depreciation | 500 | 9,500 | |||

| 15,420 | 15,420 | ||||

Working Note:

1. Opening Capital Fund:

| Balance Sheet As on 1st January 2015 |

|||||

| Liabilities |

Amount | Assets |

Amount | ||

| Outstanding sundry expenses | 50 | Outstanding Subscriptions | 90 | ||

| Capital Fund (Balancing Figure) | 15,040 | Cash in hand | 800 | ||

| Stock of stationary | 200 | ||||

| Building | 10,000 | ||||

| Investments in shares | 4,000 | ||||

| 15,090 | 15,090 | ||||

Note: In the absence of any instructions, the legacy has been treated as revenue income as the amount was very small.

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication