Question 37 Chapter 7 of +2-A

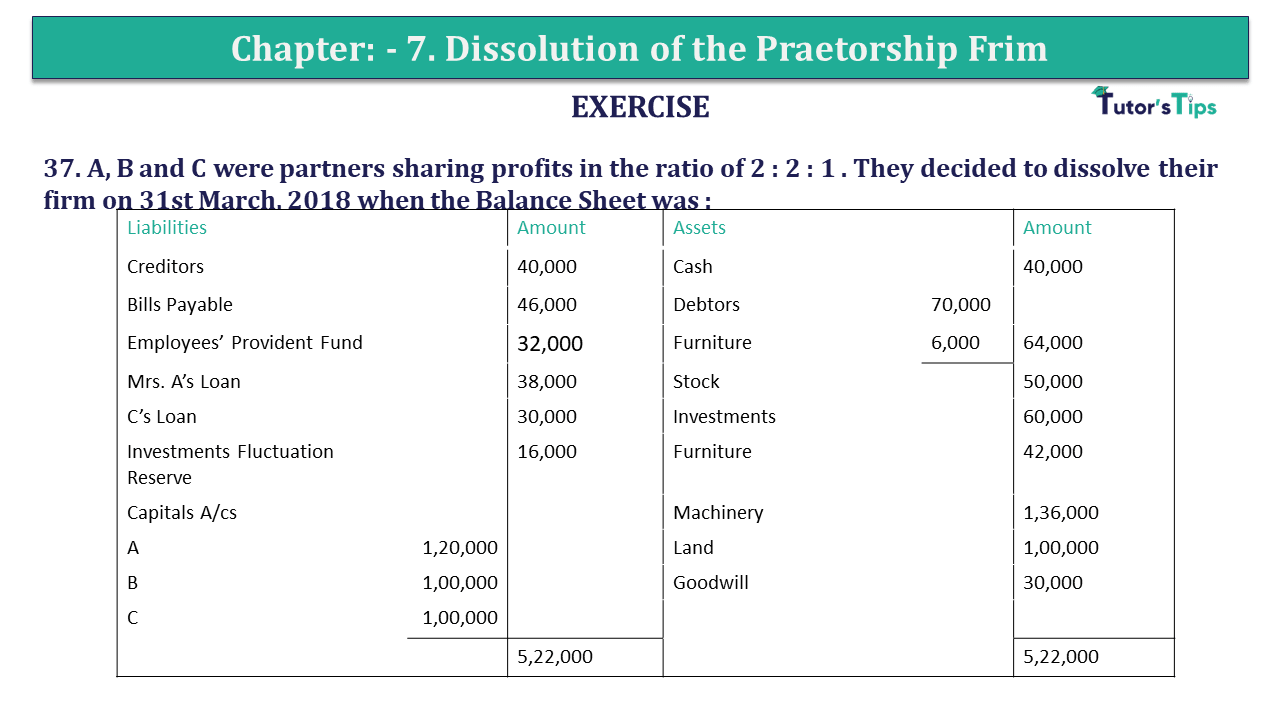

37. A B and C were partners sharing profits in the ratio of 2: 2: 1. They decided to dissolve their firm on 31st March 2018 when the Balance Sheet was :

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 40,000 | Cash | 40,000 | ||

| Bills Payable | 46,000 | Debtors | 70,000 | ||

| Employees’ Provident Fund | 32,000 | Furniture | 6,000 | 64,000 | |

| Mrs. A’s Loan | 38,000 | Stock | 50,000 | ||

| C’s Loan | 30,000 | Investments | 60,000 | ||

| Investments Fluctuation Reserve | 16,000 | Furniture | 42,000 | ||

| Capitals A/cs | Machinery | 1,36,000 | |||

| A | 1,20,000 | Land | 1,00,000 | ||

| B | 1,00,000 | Goodwill | 30,000 | ||

| C | 1,00,000 | ||||

| 5,22,000 | 5,22,000 |

Following transactions took place :

a A took over Stock at 36,000. He also took over his wife’s loan.

b B took over half of the Debtors at 28,000.

c C took over Investments at 54,000 and half of Creditors at their book value.

d Remaining Debtors realised 60% of their book value. Furniture sold for 30,000; Machinery 82,000 and Land 1,20,000.

e An unrecorded asset was sold for 22,000.

f Realisation expenses amounted to 4,000. Prepare necessary Ledger Accounts to close the books of the firm.

The solution of Question 37 Chapter 7 of +2-A: –

| Realization Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Debtors | 70,000 | Provision for Doubtful Debts | 6,000 | ||

| Stock | 50,000 | Creditors | 40,000 | ||

| Investments | 60,000 | Bills Payable | 46,000 | ||

| Furniture | 42,000 | Employee’s Provident Fund | 32,000 | ||

| Machinery | 1,36,000 | Investment Fluctuation Fund | 16,000 | ||

| Land | 1,00,000 | Mrs A’s Loan | 38,000 | ||

| Goodwill | 30,000 | A’s Capital A/c Stock | 36,000 | ||

| A’s Capital A/c Mrs.A’s Loan | 38,000 | B’s Capital A/c Debtors | 28,000 | ||

| C’s Capital A/c Creditors | 20,000 | C’s Capital A/c Investments | 54,000 | ||

| Cash A/c Expenses | 4,000 | Cash A/c | 2,54,000 | ||

| Cash A/c Creditors | 20,000 | ||||

| Cash A/c Bills Payable | 46,000 | ||||

| Cash A/c Employees’ Provident Fund | 32,000 | Loss on Revaluation | |||

| A’s Capital A/c | 30,800 | ||||

| B’s Capital A/c | 30,800 | ||||

| C’s Capital A/c | 15,400 | 77,000 | |||

| 6,48,000 | 6,48,000 | ||||

| Partners’ Capital Account |

|||||||

| Part. | A | B | C |

Part. |

A | B | C |

| To Realization A/c | 36,000 | – | – | By Balance B/d | 1,20,000 | 1,00,000 | 1,00,000 |

| To Realization A/c | – | 28,000 | – | By Realization A/c | 38,000 | – | – |

| To Realization A/c | – | – | 54,000 | By Realization A/c | – | – | 20,000 |

| To Realization Loss A/c | 30,800 | 30,800 | 15,400 | ||||

| To Cash A/c | 91,200 | 41,200 | 50,600 | ||||

| 1,58,000 | 1,00,000 | 1,20,000 | 1,58,000 | 1,00,000 | 1,20,000 | ||

| C’s LoanAccount |

|||||

| Particular |

Amount | Particular | Amount | ||

| Cash A/c | 30,000 | Balance b/d | 30,000 | ||

| 30,000 | 30,000 | ||||

| Bank Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Balance b/d | 40,000 | Realization A/c | 1,02,000 | ||

| Realization A/c | 2,75,000 | C’s Loan A/c | 30,000 | ||

| A’s Capital A/c | 91,200 | ||||

| B’s Capital A/c | 41,200 | ||||

| C’s Capital A/c | 50,600 | ||||

| 3,15,000 | 3,15,000 | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication