Question 26 Chapter 7 of +2-A

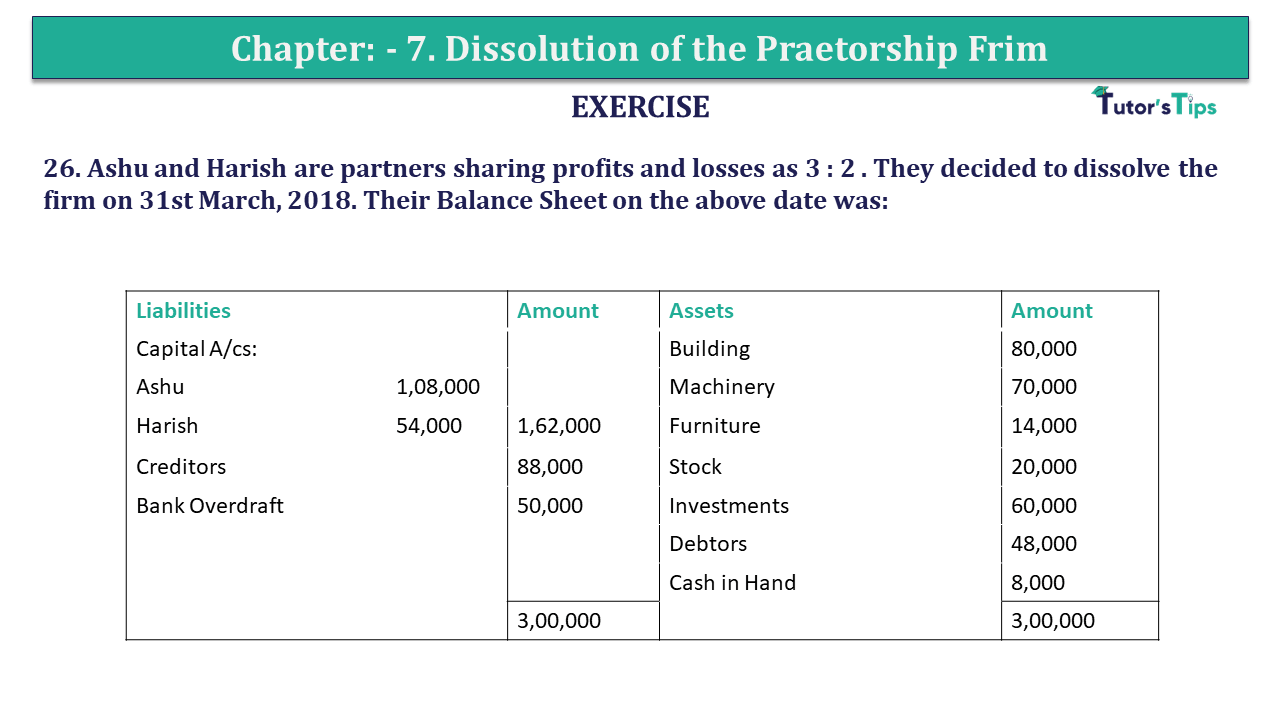

26. Ashu and Harish are partners sharing profits and losses as 3: 2. They decided to dissolve the firm on 31st March 2018. Their Balance Sheet on the above date was:

| Liabilities | Amount | Assets | Amount | |

| Capital A/cs: | Building | 80,000 | ||

| Ashu | 1,08,000 | Machinery | 70,000 | |

| Harish | 54,000 | 1,62,000 | Furniture | 14,000 |

| Creditors | 88,000 | Stock | 20,000 | |

| Bank Overdraft | 50,000 | Investments | 60,000 | |

| Debtors | 48,000 | |||

| Cash in Hand | 8,000 | |||

| 3,00,000 | 3,00,000 |

The firm was dissolved on 1st April 2018 and the Assets and Liabilities were settled as follows :

a Land and Building b realised 4,30,000.

b Debtors realized 2,25,000 with interest and 1,000 were recovered for Bad Debts written off last year.

c There was an Unrecorded Investment which was sold for 25,000.

d Vichal took over Machinery at 2,80,000 for cash.

e 50% of the Creditors were paid 4,000 less in full settlement and the remaining Creditors were paid the full amount.

Pass necessary journal entries for dissolution of the firm.

Ashu is to take over the building at 95,000 and Machinery and Furniture is taken over by Harish at a value of 80,000. Ashu agreed to pay Creditor and Harish agreed to meet Bank overdraft. Stock and Investments are taken by both partners in profit-sharing ratio. Debtors realised for 46,000, expenses of realisation amounted to 3,000. Prepare necessary Ledger Accounts

The solution of Question 26 Chapter 7 of +2-A: –

| Realization Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Building | 80,000 | Creditors | 88,000 | ||

| Machinery | 70,000 | Bank overdraft | 50,000 | ||

| Furniture | 14,000 | Ashu’s Capital A/c (see working note) | 1,43,000 | ||

| Stock | 20,000 | Harish’s Capital A/c (see working note) | 1,12,000 | ||

| Investments | 60,000 | Cash Debtors | 46,000 | ||

| Debtors | 48,000 | ||||

| Ashu’s Capital A/c Creditors | 88,000 | ||||

| Harish’s Capital A/c Bank Overdraft | 50,000 | ||||

| Cash Expenses | 3,000 | ||||

| Realization Profit | |||||

| Ashu’s Capital A/c | 3,600 | ||||

| Harish’s Capital A/c | 2,400 | 6,000 | |||

| 4,39,000 | 4,39,000 | ||||

| Partners’ Capital Account | |||||

| Part. | Ashu | Harish |

Part. |

Ashu | Harish |

| To Realization Assets taken | 1,43,000 | 1,12,000 | By Balance B/d | 1,08,000 | 8,000 |

| To Realization A/c | 56,600 | 1,965 | By Realization Liabilities A/c | 88,000 | 50,000 |

| To Realization A/c | By Realization profit A/c | 3,600 | 2,400 | ||

| To Cash A/c | 56,600 | By Cash A/c | 5,600 | ||

| 1,99,600 | 1,12,000 | 1,99,600 | 1,12,000 | ||

| Bank Account |

|||||

| Particular |

Amount | Particular | Amount | ||

| Balance b/d | 8,000 | Realization Expenses | 3,000 | ||

| Realization Debtors | 46,000 | Ashu’s Capital A/c | 56,600 | ||

| Harish’s Capital A/c | 5,600 | ||||

| 59,600 | 59,600 | ||||

Working Notes:

| Particular |

Ashu | Harish | |

| Building | 95,000 | – | |

| Machinery and Furniture | – | 80,000 | |

| Stock 3:2 | 12,000 | 8,000 | |

| Investment 3:2 | 36,000 | 24,000 | |

| 1,43,000 | 1,12,000 | ||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication